text new page (beta)

text new page (beta) English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Similars in

SciELO

Similars in

SciELO

Permalink

PermalinkIntroduction

The availability of financial sources plays a very important role in a company because the presence of sufficient financial capital can have an effect on innovation opportunities and better business processes (Farkas, 2016). Conversely, a poor financial system causes innovation stagnation which results in many MSMEs being unable to compete (Ullah, 2020) . Previous studies that tested the relationships between financial aspects like financing and the business performance had inconclusive results. For financing that originated from debt, there is evidence that it has a positive influence (Jadoua & Mostapha, 2020; Ortiz-Walters & Gius, 2012), negative influence (Comeig, Brio, & Fernandez-Blanco, 2014; Mallick & Yang, 2011; Yazdanfar & Öhman, 2015), and even no influence towards the business performance (Belwal, Tamiru, & Singh, 2012). Then previous research showed that financial sources from their own financial capital have a positive influence (Adina-Simona, 2013; Kölling, 2015; Raude, Wesonga, & Wawire, 2015), a negative influence (Balboa, Martí, & Zieling, 2011); Lehner, Grabmann, and Ennsgraber (2015), and even no influence towards the business performance (McMahon, 2007; Ortiz-Walters & Gius, 2012). From these research results, it is seen that there are inconsistencies between the influence of debt financing or its own financial capital towards business performance. Nevertheless, it seems that the financial aspect is not necessarily able to directly improve the business performance.

This condition signifies that there is another variable that mediates and influences the relationship between the financial aspect and business performance. This mediating variable is entrepreneurship oriented finance, which reveals a finance activity with an entrepreneurial characteristic. In this research, entrepreneurship oriented finance is considered as a financial activity which is a synthesis of risky financing, innovative investments, and proactive profit policies which are done by entrepreneurs to improve their business performance. This research also adds antecedent variables that are expected to influence MSME performance, which are financial and non-financial aspects. The financial aspect is financing access, while the non-financial aspects consist of the company’s condition (Abdullahi, Abubakar, Aliyu, & Umar, 2015; Dobrovic, Lambovska, Gallo, & Timkova, 2018; Kutllovci, Shala, & Troni, 2012), the entrepreneur’s condition (Abdullahi et al., 2015; N. U. Khan, Shuangjie, Khan, & Anwar, 2019), and the government’s condition (Nakku, Agbola, Miles, & Mahmood, 2020; Ntiamoah, Li, & Kwamega, 2016).

As far as the knowledge of researchers, only a limited number of studies have examined the financial (access to funding) and non-financial aspects (business prospects, entrepreneurial orientation, and government policy support) simultaneously on MSME performance through the mediation of entrepreneurship-oriented finance. This mediating variable reflects the financial activities from the entrepreneurial side done by entrepreneurs. This research is conducted while keeping in mind there is still a lack of research that discusses entrepreneurial finance from the side of MSME entrepreneurs, especially in Indonesia. This research was conducted in 2019 in three batik centers located in Central Java Province, Indonesia. Previous research looked at entrepreneurial finance from the supply side, which discussed the fund provider as the study center (Maria Rio Rita & Muharam, 2018; Romaní, Atienza, Campos, Bahamondes, & Hernández, 2018). In contrast, in this research entrepreneurial finance will be discussed from the demand side perspective, which explains financing decisions, investments, and utilizing business profit from the side of the entrepreneur. This study strives to examine the direct and indirect effects of financial and non-financial aspects towards the MSME performance through entrepreneurship oriented finance.

These research findings provide a holistic perspective on finance from an entrepreneurial perspective for MSME entrepreneurs and the government, especially in an effort to improve the business performance. The existence of MSMEs in improving people’s welfare and aggregately supporting the economy of a country necessitates support from various related parties in formulating a policy model in favor of MSMEs.

Literature review and hypothesis development

The special characteristics of MSME financing are being fast, small, and frequent (Duan, Han, & Yang, 2009). When financial access increases in the amount, process, or frequency of obtaining funds, then it will support the creation of opportunities, which have been previously identified through value creation. This availability of cheaper internal funds can be used to add to the raw materials, support the materials, and improve the production system so that the products produced can compete with the competitors, and the company performance can increase. Meanwhile, this internal financing strength can also support the growth and sustainability of a company (Jiang, Li, & Lin, 2014; S. Khan, 2015), improve customer satisfaction (Fresard, 2010), as well as develop entrepreneurial performance (Bellavitis, Filatotchev, Kamuriwo, & Vanacker, 2017). Hisrich, Petković, Ramadani, and Dana (2016) stated that venture capital has become a financing choice because the various kinds of venture capital financing are more flexible to be used and adjusted with the production process, so that the company performance target can be reached compared with the bank debt that has a fixed cost. Venture financier expertise is needed for MSMEs to assist in developing their businesses. Performance can be improved because the entrepreneur receives additional knowledge from the financier, which can become guidance and a solution to running the business.

Hypothesis 1: Financial access has a positive influence on MSME performance.

A business prospect has various dimensions. One of these is growth opportunity, which is proxied with an increase in company physical assets and expenditure ratio for R&D (Titman & Wessels, 1988). An increase in growth opportunity will improve the SME performance (Guo, Tang, Su, & Katz, 2017; Semrau, Ambos, & Kraus, 2016), as well as stimulate further investments (Levy & Powell, 2002; Srimuk & Choibamroong, 2015). According to the neoclassic theory, if a company has a high level of productivity and an increasing trend, the company will have business prospects (Kendrick, 1973). A business that possesses a growth in productivity will have a higher probability to increase financial performance because it will have a stronger competitive edge than its competitors. Related to this, productivity involves its own financial contributions towards the total asset growth, the total asset contributions in producing sales, as well as the sales effect towards the company profit (Chalos & Chen, 2002; Pares, 1980). A company that applies technology is proxied as a company that has business prospects that can produce company growth (Bianchi & Sugden, 2008; Chege & Wang, 2020). Having superior, compatible, and easily applied technology, a firm will be able to stimulate sustainable financial performance, market performance, and investments (Škerlavaj, Štemberger, & Dimovski, 2007), because of efficient and productive production.

Hypothesis 2: The business prospect has a positive influence on MSME performance.

Large-scale or small-scale companies are expected to have innovation or creativity capabilities in a competitive business environment. These capabilities are attached to the entrepreneurs in the form of social capital (Zheng, Zhu, Liu, & Chen, 2019). The effort to actualize business opportunities is reinforced by the inner characteristics of the entrepreneur. According to McClelland (2019), an entrepreneur is an individual who has high achievement needs, and that characteristic makes the individual a good fit to create a business. The entrepreneurial orientation will influence managerial practices, which ultimately will affect business performance (Frank, Kessler, & Fink, 2010; Kraus, Rigtering, Hughes, & Hosman, 2012). In other words, someone who has a high entrepreneurial spirit that is marked by extensive knowledge; a strong personality; as well as technical, financial, and marketing competence will be proficient and capable in making strategic decisions.

Hypothesis 3: Entrepreneurial orientation has a positive influence on MSME performance.

MSMEs which are not strong enough need much assistance. Institutional support is related to developing entrepreneurship through emphasizing triple helix interactions from the government, industry, and academicians in creating a workable framework for MSMEs, especially at a company’s early risky stage (Chandra & Silva, 2012). The government supports MSMEs through conducive policies in making a creative environment and facilitating new businesses (Hadiyati, 2015; Singh, Khamba, & Nanda, 2018). Government policies are designed so that they produce business innovations through fund provisions and other resources which are able to stimulate economic growth. Having an efficient capital market, competitive venture capital, cheap funds, entrepreneurship education, and other regulations which are oriented to produce trust and support for entrepreneurs can have a positive influence in developing new companies in the economy.

Hypothesis 4: Government policy support has a positive influence on MSME performance.

When financial access increases, entrepreneurs’ ability to obtain external funds to develop their companies will also increase (Maria Rio Rita & Utomo, 2019). Meanwhile, based on the free cash flow theory, when MSMEs have a sufficient cash flow, it can help them to convince investors to invest in their companies. Having sufficient internal funds can reduce the problem of asymmetric information with fund providers (Trinh, Kakinaka, Kim, & Jung, 2017). According to the opportunity based entrepreneurship theory, the main components which need to be given attention in business activities - including in accessing financial resources - are the locus of changes, sources of opportunity, and initiator of changes (Jonathan T Eckhardt & Shane, 2010; Jonathan T. Eckhardt & Shane, 2003). Locus of changes can be found in the new product creation stage, new market discoveries, new resource creations/discoveries, the appearance of new production methods, as well as changes that are produced within an organization (Schumpeter, 1934). Opportunity sources can be various, such as due to asymmetric information between market actors, imbalances between requests and offers, as well as new shocks in the market. In the interim, the actors initiate changes that are able to produce entrepreneurship opportunities. This type of initiator can influence the value creation process and the duration of the business opportunities.

Hypothesis 5: Financial access has a positive influence on entrepreneurship oriented finance.

When a firm develops, its business activities will also escalate. When a company grows, its business activities will also increase (Blackburn, Hart, & Wainwright, 2013). A surge in these business activities can occur in investment activities or routine operational activities. This has an effect on the need for additional capital to accommodate an increase in business activities through innovative and proactive investment activities. When business prospects are better, MSME entrepreneurial oriented finance will also be better. When there is an uptick in growth opportunity, productivity, research funding, and development (Ortega‐argilés, Piva, Potters, & Vivarelli, 2010), as a sign of an improvement in business prospects, so investment needs will rise. Entrepreneurs will strive to finance these investment needs from internal or external capital (Balaban, Župljanin, & Ivanović, 2016). When these business prospects rise, it will allow entrepreneurs to capture opportunities by increasing their capital needs in order to actualize their investment activities in an innovative and proactive way.

Hypothesis 6: The business prospect has a positive influence on entrepreneurship oriented finance.

In an MSME financing context, entrepreneurs who have an entrepreneurship orientation will strive to increase their financial access by having connections with fund providers or other entrepreneurs, which will result in an increase in their firm performance (Mohammed, Umar, & Nzelibe, 2016). Having a cognition bias in making financial decisions is demonstrated to be able to influence investors to invest in their firms (Adomdza, Åstebro, & Yong, 2016). This means that entrepreneurs who are willing to take risks, be innovative, and be proactive will be able to look for business funds and add to their capital, in order to produce new materials, methods, products, markets, and organizations through a creative and innovative process. Furthermore, entrepreneurs can utilize their efforts to develop their firms and beat the competition.

Hypothesis 7: Entrepreneurial orientation has a positive influence on entrepreneurship oriented finance.

This asymmetric condition can increase fundraising costs for small firms (Vandenberg, Chantapacdepong, & Yoshino, 2016). When creditors do not receive enough information from debtors about the business conditions and activities, the credit market will be reluctant to release funds, so that they will incur high interest and credit rationing. Caner and Karan (2012) stated that the government needs to play a role in providing financial incentives (subsidized credit) or non-financial incentives to evaluate credit risks, so that it boosts the creditworthiness for MSMEs. This statement is in line with H Kent Baker, Kumar, and Rao (2020) as well as Altman, Esentato, and Sabato (2020), in that policymaking needs to design appropriate and innovative policies for MSMEs which have underutilized funding sources. This soft credit assistance facilitates entrepreneurs to improve their innovative investments, which can produce a profit that can be used for proactive investments. Government support can also be actualized in the form of training and mentoring (such as business incubators), which teach about how to create, search for, and utilize funds and other resources to boost business performance.

Hypothesis 8: Government policy support has a positive influence on entrepreneurship oriented finance.

A firm that lacks entrepreneurial characteristics will have few innovations, avoid risks, and imitate competitors’ actions rather than lead (Balaban et al., 2016). An entrepreneur who is able to calculate time and the number of funds which should be collected will be able to increase financial access to obtain funds, efficiently allocate the resources to actualize business opportunities, and make decisions to get out of financial difficulties to make the firm successful (Mitter & Kraus, 2011). An entrepreneur who has financial entrepreneurship capabilities will be able to develop one’s ideas and business by using funds aggressively, doing innovative investments, and utilizing profit for proactive programs to create high performance.

Hypothesis 9: Entrepreneurship oriented finance has a positive influence on MSME performance.

According to the resource-based view theory, when financial access increases, the availability of financial resources that are reflected from the internal and external capital will increase (Ferreira, Garrido Azevedo, & Fernández Ortiz, 2011). In spite of this, the resource-based entrepreneurship theory emphasizes that an increase in these resources does not automatically boost the performance, as it depends on the entrepreneur’s unique ability to recognize opportunities, obtain resources, and possess an organizational ability to combine input to become business performance (Alvarez & Busenitz, 2001; Maria Rio Rita & Huruta, 2020). When adding business capital is also followed by increasing the entrepreneurship and management capacity, then the firm performance will improve. Variations in obtaining and utilizing the funds will determine the firm’s success. Klonowski (2016) stated that an increase in funds will be meaningful when an entrepreneur is able to allocate the funds for productive and efficient activities, so that the business performance can be made better.

Hypothesis 10: Entrepreneurship oriented finance mediates the influence of financial access on MSME performance.

According to the resource-based entrepreneurship theory, a prospective company is not necessarily able to produce high performance; it depends on how the prospects can be viewed by the entrepreneur as opportunities to be developed (Jonathan T. Eckhardt & Shane, 2003). This is an entrepreneurship ability that can see opportunities, develop ideas, and assemble resources (including financial ones) in business actualizations (Hock-Doepgen, Clauss, Kraus, & Cheng, 2021). This means that an entrepreneur is able to aggressively bring in funds and develop innovative investments and abilities to attract business prospect which can be proactively utilized to capture business opportunities to improve the firm performance. Performance differences with the same business prospects are caused by diversity in available funds and how the resources are allocated in productive and efficient business activities . This means that entrepreneurial-oriented finance management will be able to change a firm that lacks prospects to become one that has high performance.

Hypothesis 11: Entrepreneurial oriented finance mediates the influence of the business prospect on MSME performance.

Tangible and intangible unique resources, including human resources in the form of knowledge, experience, and entrepreneurship orientation, cannot have a direct positive impact on the performance, but they must be mediated by an entrepreneur’s ability to see opportunities, assemble resources like capital, develop the resources in the form of innovation, and produce profit which will be used again for investments (Alvarez & Busenitz, 2001). Entrepreneurs who have an entrepreneurship orientation will be able to easily work with other people, including investors. If the entrepreneurship orientation increases, then an entrepreneur’s ability to obtain funds to operate the firm will increase also. In the entrepreneurial finance theory, having sufficient funding availability will facilitate entrepreneurs in developing their companies, whether for start-ups or expansion.

Hypothesis 12: Entrepreneurship oriented finance mediates the influence of entrepreneurial orientation on MSME performance.

Government assistance, which is financial (soft loans) or non-financial, such as training and assistance to MSME entrepreneurs, does not automatically boost business performance. Inappropriate use of assistance and unwise management by entrepreneurs have made government intervention meaningless (Sandra & Purwanto, 2017). Not all entrepreneurs are able to see opportunities resulting from changes in the initiator (government) aspect. When there are initiation and intervention from the government related to cheap credit policies, some entrepreneurs will be able to respond to these opportunities to develop their enterprises, while others will not. Z. Serrasqueiro, Nunes, and Leitão (2011) discovered that government subsidies have a positive influence on the amount of research and the development of MSMEs, which can produce technology and innovation to improve business performance. When government financial and non-financial support is responded positively by the owners of MSMEs, then entrepreneurship oriented finance capacity will strengthen. These different responses are due to differences in entrepreneurship capacity of ownership and management. Entrepreneurs are more confident and have the courage to access external capital sources, carry out innovative investments and profit allocation is prioritized for business expansion. Whenever financial assistance, training, and mentoring are considered beneficial, then entrepreneurs will strive to run their firms better to boost their business performance (Jahanshahi, Nawaser, Sadeq Khaksar, & Kamalian, 2011; Kitching, 2006). This infers that government intervention can stimulate risky financing, innovative investments, and proactive profit policies from the entrepreneur, which in turn can improve the firm performance.

Hypothesis 13: Entrepreneurship oriented finance mediates the influence of government policy support on MSME performance.

Research method

The population of this research was MSMEs involved in the batik business and located in Central Java Province, Indonesia, in Rembang, Pekalongan, and Surakarta. The three locations were chosen because they have their own unique aspects (Maria Rio Rita, Priyanto, Andadari, & Haryanto, 2018), in which the geographic regional differences can also influence the business activities (Priyanto, Haryanto, Andadari, & Rita, 2016). The total number of MSMEs under the MSME and Cooperative Agency are listed in Table 1 below:

Table 1 Number of MSMEs in Pekalongan Regency, Rembang Regency, and Surakarta Municipality

| No. | Location | Total Population | Percentage |

|---|---|---|---|

| 1 | Pekalongan Regency | 878 | 70% |

| 2 | Rembang Regency | 120 | 10% |

| 3 | Surakarta Municipality | 232 | 20% |

| Total | 1,230 | 100% |

Source: MSME and Cooperative Agency (2018-2019)

The analysis unit of this research was batik MSME entrepreneurs who did the production, were responsible for the finances, and controlled the business management. The sample retrieval stage began by first determining the regency/city locations. This study selected three regencies/cities which had batik characteristics in Central Java, comprising Pekalongan Regency, Rembang Regency, and Surakarta Municipality. Then, after deciding on the regencies, the sub-districts were chosen that had the largest concentrations of batik MSMEs. The next stage was to set the villages that had the batik MSMEs. After the village locations were fixed, then with the assistance of the Cooperative and MSME Agency, village leaders, the heads of batik handicraft groups in the three regencies, and other key informants, the sample names were selected to become the respondents (sampling frame). The number of samples was determined based on the minimum number of samples needed to process the data by using SEM.

The sample design was chosen using a probability sampling approach. The probability sampling design applied a restricted/ complex probability sampling with a sampling area (Sekaran & Bougie, 2013) based on culture. The number of batik MSMEs in Pekalongan comprised 70 percent of the total population. Then in Rembang they made up 10 percent and in Surakarta 20 percent. These percentages were within the guidelines in choosing the number of samples in each location (Table 2).

Table 2 Planned regions and number of respondents retrieved

| No. | Region | Proportion | Number of Respondents |

|---|---|---|---|

| 1 | Pekalongan Regency | 70% | 210 |

| 2 | Rembang Regency | 10% | 30 |

| 3 | Surakarta Municipality | 20% | 60 |

| Total | 100% | 300 |

Source: MSME and Cooperative Agency (2018-2019), processed.

Research variables and their measurements

The variable details and the measurement indicators of this model are explained below:

Financial access (FA) was measured from the indicators: the number of funds, processes, and frequency of obtaining the funds (Duan et al., 2009).

Business prospect (BP) was measured from the indicators: growth opportunity (Anderson & Reeb, 2003; Titman & Wessels, 1988), productivity growth (Chalos & Chen, 2002; Pares, 1980), and technological resources (Ramdani, Kawalek, & Lorenzo, 2009).

Entrepreneurial Orientation (EO) was measured from the indicators: risk-taking, innovative, and proactive (Kreiser & Davis, 2010).

Government policy support (GPS) was measured from the indicators: a soft credit program (soft loans), training, and mentoring (Lean & Tucker, 2001).

Entrepreneurship-oriented finance (EOF) was measured from the indicators: risky financing, innovative investments, and proactive profit policies.

MSME performance (MP) in this research used three performance measurements: financial performance (Torugsa, O’Donohue, & Hecker, 2012), market performance (Brouthers & Nakos, 2004), and entrepreneurship performance (Maria Rio Rita & Thren, 2019).

Data analysis technique

This multilevel model was estimated by using structural equation modeling (SEM) (Jr, Black, Babin, & Anderson, 2010). This research model consisted of exogenous and endogenous constructs. There are two stages in doing this estimation: a confirmatory factor analysis (CFA) technique and a full structural equation technique model. The structural equations applied in this research model are as follows:

Explanation:

β |

= Path coefficient which explains the influence of the exogenous variable on the endogenous variable. |

γ |

= Path coefficient which explains the influence of the endogenous variable on other endogenous variables. |

ζ |

= Error term. |

In principle, SEM is a multivariate analysis that describes the application of several models in a compact manner, namely the factor analysis, path analysis, and regression analysis models. The advantage of SEM compared to another data analysis is that it can be used to determine the indicators forming a variable, test the validity and reliability of an instrument, confirm the accuracy of the model, and examine the effects of a variable on other variables. The maximum likelihood approach allows the researcher to test the hypothesis when there are a number of factors that can explain the intercorrelation between variables (Ghozali, 2011). When minimizing the maximum likelihood function, the chi-square likelihood ratio is obtained, which indicates that the hypothesized model fits the data. This approach assumes that the number of samples must be large (asymptotic), the distribution of the observed normal variables is multivariate, the hypothesized model must be valid, and the measurement scale has continuous (interval) variables.

There are seven steps in a data analysis using the SEM technique (Ghozali, 2011), namely: (1) developing a model based on a theory, (2) compiling a path diagram that states a causal relationship, (3) translating the path diagram into structural equations and research model specifications, (4) selecting input matrices and estimation techniques, (5) assessing problem identification, (6) evaluating the goodness of fit model, and (7) doing model interpretations and modifications.

Results

Respondent profile

The respondents had an average age of 42 years old, even though there was a variation in ages in the three locations. The respondents had various reasons for choosing to work in the batik industry, including continuing the family business, their familiarity with the batik business environment in their daily lives, and an interest to become entrepreneurs in the batik industry after finishing their studies. In general, the respondents were males (63%) with the remainder being females. Based on the findings in the field, it was discovered that the batik businesses in Surakarta Municipality and Pekalongan Regency were managed more by the heads of households. Although women also assisted in the businesses, they were not too actively involved in managing the businesses. A different condition was seen in batik companies in Rembang Regency, where women were more active in managing the enterprises. Meanwhile, the men were employed more outside of the batik sector. In Surakarta Municipality and Pekalongan Regency, the respondents averaged 12 years of business experience, while in Rembang Regency they averaged 7 years of batik business experience. The MSMEs which were able to exceed a five-year period were evaluated in terms of their growth and ability to survive the turbulence in the beginning of their establishment, where many small companies are in an oscillation cycle of quick environmental change that results in threats and opportunities from one year to the next.

Table 3 Respondent profile

| Surakarta Municipality | Rembang Regency | Pekalongan Regency | Total | |

|---|---|---|---|---|

| Age | ||||

| Min | 24 | 22 | 19 | 19 |

| Max | 69 | 60 | 72 | 72 |

| Average | 46 | 41 | 40 | 42 |

| Gender | ||||

| Male | 43 (72%) | 10 (33%) | 139 (64%) | 192 (63%) |

| Female | 17 (28%) | 20 (67%) | 78 (36%) | 115 (37%) |

| Total | 60 (100%) | 30 (100%) | 217 (100%) | 307 (100%) |

| Experience | ||||

| Min | 5 | 5 | 5 | 5 |

| Max | 43 | 15 | 48 | 48 |

| Average | 16 | 7 | 13 | 12 |

Source: Primary data, processed (2019)

An SEM estimation method with bootstrapping was carried out because the multivariate normality assumption in the initial full model was not fulfilled, even though the outlier data was already eliminated. Therefore, there were differences in evaluating the full model feasibility which was used in estimating the parameter values with the SEM method based on the maximum likelihood estimation (MLE). A model fit test was done by using the Bollen-Stine bootstrap method. If there are no significant differences between the data with the model, then the model is considered as a fit to do an estimation (Ghozali, 2011).

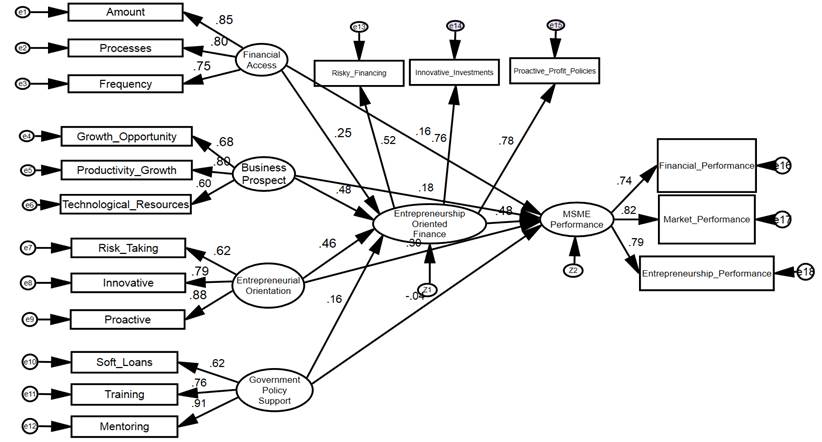

The testing of the bootstrapping full model produced the following results, as depicted in Figure 1 below:

Table 4 below presents the output of the full model with the bootstrapping procedures. The bootstrap output was evaluated through a bias-corrected confidence interval analysis.

Table 4 Bias-corrected confidence interval (standardized regression weights: group number 1 - default model)

| Parameter | Estimate | Lower | Upper | P | ||

|---|---|---|---|---|---|---|

| EOF | <--- | FA | .251 | .092 | .405 | ** |

| EOF | <--- | EO | .251 | .092 | .405 | *** |

| EOF | <--- | BP | .482 | .318 | .648 | *** |

| EOF | <--- | GPS | .158 | .066 | .241 | ** |

| MP | <--- | EOF | .482 | .279 | .656 | *** |

| MP | <--- | FA | .162 | .012 | .299 | ** |

| MP | <--- | BP | .177 | -.035 | .359 | .171 |

| MP | <--- | EOF | .297 | .161 | .446 | ** |

| MP | <--- | GPS | -.039 | -.143 | .064 | .554 |

Explanation: *, **, *** coefficients are significant at the 10%, 5%, and 1% levels

Source: Primary Data, Processed (2019)

The loading factor values of each latent variable towards the other latent variables as well as the indicators towards the latent variables can be seen from the bias-corrected confidence interval. For instance, the EO variable towards EOF is 0.251 with a confident interval of 0.092 until 0.405. Since the zero value is not included in the low range and high range, the hypothesis which states that the regression weight EO EOF is the same as zero, is rejected. This assumption can also be seen more easily through the p-value = 0.009, which is significant at α 1%. In observing the output above, it was discovered that from the 13 hypotheses proposed, 11 of them are accepted (H1, H3, H5, until H13), while 2 of them are rejected (H2 and H4) because they have a significant value higher than 5% of the low range or the high range has a zero value.

The size of the direct effect, indirect effect, and total effect between the constructs tested in the model at the 5% error level are shown in Table 5 below:

Table 5 Direct effect, indirect effect, total effect

| No | Path | Direct Effect | Indirect Effect | Total Effect | |

|---|---|---|---|---|---|

| 1 | FA → EOF → MP | .195 | .084 | .279 | |

| 2 | BP → EOF → MP | .098 | .201 | .299 | |

| 3 | EO → EOF → MP | .268 | .143 | .411 | |

| 4 | GPS → EOF → MP | -0.056 | .063 | .055 |

Source: Primary Data, Processed (2019)

Based on Table 5, the size of the total effect coefficient in path 1, path 2, and path 3 is bigger than the direct effect coefficient. Besides that, in path 2 and path 4, the indirect effect coefficient is bigger than the direct effect coefficient. This shows that EOF acts as a mediating variable that connects the exogenous and endogenous constructs.

Table 6 Sobel test results

| No. | Explanation | Input | Std. Error | P-Value | Mediation Types | |

|---|---|---|---|---|---|---|

| 1 | Entrepreneurship oriented finance mediates the influence between financial access and business performance. | a: | .182 | .02 | .001 | Partial mediation |

| b: | .390 | |||||

| sa: | .010 | |||||

| sb: | .109 | |||||

| 2 | Entrepreneurship oriented finance mediates the influence between business prospect and MSME performance. | a: | .600 | .10 | .04 | Full mediation |

| b: | .390 | |||||

| sa: | .225 | |||||

| sb: | .126 | |||||

| 3 | Entrepreneurship oriented finance mediates the influence between entrepreneurial orientation and MSME performance. | a: | .342 | .06 | .04 | Partial mediation |

| b: | .390 | |||||

| sa: | .129 | |||||

| sb: | .126 | |||||

| 4 | Entrepreneurship oriented finance mediates the influence between government policy support and MSME performance. | a: | .111 | .02 | .07 | Full mediation |

| b: | .390 | |||||

| sa: | .040 | |||||

| sb: | .126 | |||||

Source: Primary Data, Processed (2019)

Discussion

Determinants of MSME performance

Increasing the financial access, whether in the total, process, or frequency of funds obtained, will support the actualization of opportunities that have been previously identified along with other productive resource collaborations through business activities. As a result, the firm can serve the market needs, increase its profit, and enjoy prosperity from its business success. About 86% of the respondents stated that financing from debt makes them more motivated to work, as well as can increase the production, innovations, product promotions, production equipment, business location expansion, raw material purchases, experiments, networks, and market targets so that it ultimately increases the business profit. Entrepreneurs who have that perception can see that an increase in debt will improve their debt structure, which eventually will boost their business performance.

The neoclassic theory states that the growth of business supporting physical assets and an increase in the expenditure ratio for R&D will affect firm performance. Besides that, a company which has a growth in productivity will have greater chances to increase its performance, because it will have a greater competitive ability than its competitors. The application of the newest technology that matches the firm needs and is applied effectively in the business operations, which will have greater opportunities to improve its performance (Shikher, 2011; Škerlavaj et al., 2007).

If observed from the empirical data, it seems that micro and small scale batik firms dominate the sample total (96%), while the rest are medium-scale firms. It cannot be proven that the majority of the samples, which are micro and small scale batik firms, have a positive effect on the business prospect towards the performance. There are budget limitations for routine experiments in producing products, processes, and new markets, which are the main obstacles for micro and small scale firms. Besides that, the low level of interest to respond and adapt to technological developments also disrupt the business performance. Batik is known as a business which is passed down from one’s ancestors, so that it is rather challenging to change the entrepreneurs’ mindsets to switch to utilizing new technology, which will actually reduce the quality of batik produced. The experiment expenditures done by micro and small firms for the last three years are considered as small/low. The lack of fund allocations for research and product development causes the businesses to become stagnant so that the sales growth is low and the market needs are not fulfilled. Besides that, micro and small scale firms do not respond very positively to the current technological developments, because marketing is still done in a conventional way. They do not apply a modern production process and are not interested in utilizing information technology advancements to assist their firms. This finding indicates that the firm scale category can determine the high or low level of the business prospect. Low growth opportunities, productivity growth, and technology applications will not positively affect business performance.

Sidik (2012) stated that entrepreneurs who have an entrepreneurial spirit will boost their business performance. Entrepreneurs who have cultural or superior values will provide great contributions to their business performance. Entrepreneurs who have a high desire for success and do not want to be demeaned by society will engage in various innovative efforts so that their businesses can succeed. This success will be its own happiness (well-being) and create competitive superiority (a champion), as well as have a culture with a high power distance so that it will influence the business performance. Entrepreneurs who have a desire to show their abilities and successes in their businesses will make the entrepreneurs succeed in their firms. The need to reach a social status and gain respect from the environment is a trigger to change the entrepreneur’s personality (Hagen, 1960).

It is suspected that there are several reasons for the government policies having a lack of a significant influence towards MSME performance. The samples, which are mostly micro and small enterprises, reported that they rarely or never received training programs from the government. The entrepreneurs view the government as tending to pay more attention to large scale businesses. There is a lack of training programs accompanied with the low level of mentoring from the government in batik firm management. Small entrepreneurs also complain about the cheap funding incentives from the government, because the incentives are not evenly allocated. The phenomenon of low government support is considered as being unable to improve batik MSMEs’ performance. The majority (59%) of the respondents stated that they did not receive any training from the government in the last three years. Only 41% of the respondents received training in the form of the batik making process, holding exhibitions, dyeing, financial management, and business with various kinds of intensity in the three regions. A similar sentiment was also felt by the respondents towards the government mentoring program which was received by MSMEs, in which 74% of the respondents revealed that they never received any such mentoring. For the last three years, the mentoring that was received was a work program that involved the local MSME cooperative agency, especially in arranging business proposals and utilizing business credit. In referring to the survey results, the respondents considered that the government did not play much of a role in the batik MSMEs (71%). The reason found by the respondents was the presence of soft loan allocations that were not distributed evenly and the total was considered too small to fulfill the business needs; the training was not given equally to all MSMEs (the government was considered as siding more with large scale firms); the lack of attention from the municipal government of each region towards the batik firms; the lack of intensive mentoring that was conducted; as well as the lack of flow of cheap funding or rolling financing from the local municipal government.

Determinants of entrepreneurship oriented finance

When the number of internal funds, external funds, and debt is increased, an entrepreneur’s ability to aggressively search for funds and allocate them for innovative and proactive investment activities will also increase (Chemmanur & Fulghieri, 2014; Xiao, 2011). An entrepreneur who has high financial access will enable the entrepreneur to acquire external funds to develop the firm through increasing the expertise, innovations, competition, and investments. There are differences in information mastery between one party and another party, which actually can work together. MSME entrepreneurs who do not have sufficient information about the financial resources which can be obtained will find it challenging to acquire financial access. In contrast, if an entrepreneur has sufficient information and the fund provider understands the conditions and risks of the MSME business, the entrepreneur will have high financial access.

When there is an opportunity for a firm to grow, there will be an increase in productivity and available technological resources to solve business problems. The entrepreneur will respond by increasing the funds through internal and external capital in the form of debt or increasing the capital structure, even though the entrepreneur will have to pay higher interest (Huang & Liu, 2014). This effort is done to encourage innovative investment activities that are expected to be able to boost the company profit so that it can proactively develop the firm. So when a business prospect increases, the entrepreneur will respond by increasing the capital structure to increase investment activities and firm profit.

According to the resource-based entrepreneurship theory, entrepreneurs who possess an entrepreneurship orientation will be able to assemble natural resources, human resources, technology, and funds to develop their firms (Alvarez & Busenitz, 2001; Brown, Davidsson, & Wiklund, 2001). Resources will not be valuable if they are not managed by entrepreneurs who have an entrepreneurial spirit. This reality can also be explained by applying the behavioral finance theory, where an entrepreneur who has psychological behavior like planning fallacy, overconfidence, and optimism - will influence the business behavior and financial decisions, whether funding decisions or investment decisions (H. Kent Baker & Ricciardi, 2015; Fatma & Ezzeddine, 2019). According to (Van Der Wijst, 2012) and Thomas (2018), entrepreneurs who have high entrepreneurship tend to have a behavior bias, whether related with their cognition or emotions, so that the entrepreneurs will be brave to take risks, including in obtaining internal and external funds to finance their firms, be able to develop innovative investments due to their bravery in analyzing problems and looking for innovative solutions (Tan, 2001), as well as be able to use the profit to develop their firms to be proactive and competitive.

The opportunity-based entrepreneurship theory explains that occasionally there are special treatments from the government by providing soft loans, training, and mentoring, which means that there are changes in the sources of opportunity and initiator of changes (Jonathan T. Eckhardt & Shane, 2003). If the government does not offer support for MSMEs by providing soft loans, training, and mentoring, it will hinder entrepreneurs from obtaining company funding. Consequently, their firms will find it difficult to advance, be inefficient, and be non-productive due to operating in a non-economical business scale and having high capital costs.

MSME entrepreneurs who have high entrepreneurship-oriented financial ability will be able to acquire funds, use the funds for investments, and receive profit to create more competitive businesses. When based on the entrepreneurship theory and the resource theory, if entrepreneurs have resources, including financing, they will be capable of seeing opportunities, developing ideas, and executing ideas by assembling the available resources, developing the organizations, creating markets, and developing the products (Jonathan T Eckhardt & Shane, 2010). When beginning a company, an entrepreneur must mobilize one’s internal resources like norms, attitudes, and values which can influence new business creations. When MSMEs possess superior values in their firms, their performance will be high (Aldrich & Cliff, 2003).

Role of entrepreneurship oriented finance as a mediating variable

Based on the premises found in the resource-based view theory, when capital increases, the financial resources available for entrepreneurs will also intensify (Ferreira et al., 2011) so that it is able to improve the business performance. Despite this, there is still another instrument that is able to accelerate financing to improve business performance, which is the entrepreneurial competence owned by an entrepreneur. According to the resource-based entrepreneurship theory, an upsurge in financial resources will make the business perform better when the entrepreneur has a unique ability to recognize opportunities, the capability to obtain resources that are needed to utilize opportunities, and organizational know-how to combine input to become business performance (Alvarez & Busenitz, 2001). The availability of heterogeneous resources that are owned by a company does not necessarily ensure a firm’s success. In contrast, a firm needs to manage and collaborate the resources in an innovative way, be brave to take risks, and be proactive to achieve top performance.

Prospective companies do not always produce high performance; it depends on how the prospects are seen by entrepreneurs as opportunities that can be developed. When there is innovation adoption, the amount of debt will increase and the financial structure will change, which will be used to purchase raw materials and assistance, employ a workforce, and do other production factors, which will eventually be able to increase the production, productivity, and business performance. Technological changes will give rise to opportunities. An entrepreneur who has an entrepreneurial-oriented financial ability will be able to recognize opportunities and assemble resources in the form of funds, markets, and organizations, which will advance the business performance (Alvarez & Busenitz, 2001). An empirical fact reveals that technological availability, an increase in productivity, and the presence of the same growth opportunities can produce different business performance, depending on how the availability of external or internal funds can take advantage of the opportunities.

The resource-based entrepreneurship theory explains that unique resources, whether they are tangible or intangible, including human resources like knowledge, experience, and entrepreneurship orientation, do not necessarily increase performance. It must be mediated by an entrepreneur’s ability to see opportunities, assemble resources and financial capital, develop the resources in the form of innovation, and produce the profit that will be used again to invest. An entrepreneur who lacks or does not have an entrepreneurship orientation will have difficulties in obtaining business capital, because the entrepreneur is not very creative, does not innovate, and is afraid to try something new due to having asymmetric information and cognition bias (Kon & Storey, 2003). This cognition bias can cause bravery on one side and fear on another side. This condition is what causes entrepreneurship orientation to improve business performance when it is supported by an entrepreneur’s ability to obtain funds, investment activities, and the capability to produce a profit to develop the company. The capacity of entrepreneurs to mobilize financial sources, including financial assistance from the government, is in how they allocate the resources in their business activities, manage risks, and optimize the financial contracts that have been made, in order to create and improve their company value to have an effect on the business performance (Smolarski & Kut, 2011).

Besides that, the MSME performance variation is not only caused by whether or not there is government policy support, but it also depends on the entrepreneur’s capability to see opportunities as a result of a change in an initiator’s aspect, such as the government acts as an initiator of change to give rise to business opportunities. This condition also applies in some countries with a huge number of SMEs, such as Indonesia and China. Especially in China, the government support for SMEs is proven successful because entrepreneurs also have high entrepreneurship oriented finance, and they can expand their businesses to the global scope nowadays.

Variations in government initiations and interventions related to cheap credit policies and variations in entrepreneurs’ abilities in responding to the particular opportunities in actualizing their business ideas are factors in shaping successful companies. When entrepreneurs feel that they receive policy support in the form of financial assistance, training, and mentoring, then the entrepreneurs will strive to run their businesses better, so that their company performance will increase (Kitching, 2006).

Conclusions

The study was carried out in Surakarta Municipality, Rembang Regency, and Pekalongan Regency in 2019, and had the following conclusions. In referring to the research results, a strategy can be devised for MSME entrepreneurs to improve their business performance by focusing on financial and non-financial aspects through the role of mediation of entrepreneurship oriented finance. When MSMEs have strong funding access, as measured from the high frequency of obtaining funds, the amount of internal or external funds included, as well as a quicker and easier process in obtaining funds, it will stimulate entrepreneurship oriented financial activities (a high level of innovative investment activities for experiments, intensive proactive profit allocation policies for company development, as well as risky financing by utilizing debt for the enterprise). MSME entrepreneurs also need to take advantage of their business opportunities and be synergized with government incentives, whether in financing or training-mentoring that is provided for company development. An increase in entrepreneurship oriented financial activities will create superior business performance through customer satisfaction, an increase in entrepreneurial skills, as well as a better company financial condition.

This research used an SEM method with bootstrapping because there was an issue in fulfilling the multivariate normality assumption. This has an implication in using resampling data to do estimations, in order that the probability (p) is stable. Therefore, future research can use an alternative method (non-resampling method), so that an analysis can be done by using an original sample. As for the insignificant findings between business prospect and government policy support, more in-depth studies are needed, such as by classifying firms into micro, small, and medium scale enterprises. The business scale which is the moderation variable has the potential to cause different effects towards the business performance (Blackburn et al., 2013; Z. S. Serrasqueiro & Nunes, 2008). The variation in the business scale is suspected to be related to the efforts and strategies of entrepreneurs in making their business decisions, where larger business scales face more complex problems and require solutions from smarter entrepreneurs. In addition, the larger the scale of the business, the greater the availability of resources that can be utilized to support business activities. This presumption can be tested in further studies. Then when testing was done simultaneously for all business scale categories, no unique effects were found towards the business performance.