Services on Demand

Journal

Article

text in

text in  English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Similars in

SciELO

Similars in

SciELO

Share

Permalink

PermalinkContaduría y administración

Print version ISSN 0186-1042

Contad. Adm vol.63 n.2 Ciudad de México Apr./Jun. 2018

https://doi.org/10.22201/fca.24488410e.2018.1236

Articles

Management strategy and intellectual capital disclosure: Influence of corporate governance

1Universidad de Castilla-La Mancha, España

2Universidade do Minho, Portugal

Knowledge has become a key strategic resource for business success and has led companies to be concerned about managing their knowledge assets (intellectual capital). However, accounting as an information system has suffered a loss of reliability of the information provided, by showing that the market value of companies is higher than the book value shown in the balance sheets. This discrepancy has been one of the main reasons why companies voluntarily manage and disclose their intellectual capital. Relying on the agency theory and the resources and capabilities theory, this paper analyses the influence of corporate governance in the management of information intellectual capital. The methodology used was based on content analysis of annual reports using a analysis multivariate linear regression.

Keywords : Knowledge; Intellectual Capital; Corporate Governance; Information Disclosure

JEL Classification: M19; M49

El conocimiento se ha convertido en un recurso estratégico clave para el éxito de los negocios y ha llevado a las empresas a preocuparse por la gestión de sus activos de conocimiento capital intelectual). No obstante, la contabilidad, como sistema de información, ha sufrido una pérdida de fiabilidad de la información suministrada, al poner en evidencia que el valor de mercado de las empresas es superior al valor contable que figura en los balances. Esta discrepancia ha sido uno de los principales motivos por los que las empresas gestionan y divulgan voluntariamente su capital intelectual. Apoyándonos en la teoría de la agencia y en la de recursos y capacidades, se analiza la influencia que ejerce el Gobierno Corporativo en la gestión de información del capital intelectual. Se utiliza como metodología el análisis de contenido de los informes anuales y se realiza un análisis multivariante de regresión lineal.

Palabras clave: Conocimiento; Capital intelectual; Gobierno Corporativo; Divulgación de Información

Clasificación JEL: M19; M49

Introduction

In recent decades, particular attention has been paid to corporate governance, most notably, following the financial scandals starring certain companies, due to the fraudulent practices carried out in the management of the same. One of these practices could be traced to the lack of diligence in the implementation of accounting standards (Babío & Muíño, 2005; Rodríguez-Ariza, Frías & García, 2014; Sánchez Fernández de Valderrama, 2004), which has caused a distortion in the published financial information, giving rise to distrust in the current economic system. Furthermore, these actions have contributed to a crisis of values and of basic attitudes to maintain stable relations (Bueno Campos, 2002) between owners and directors, and other groups of interest of the companies. The key to rectify this lies in the “board of directors” of the companies that have acted without an adequate good governance and without ethical standards; offering to the market information that has been distorted from the true situation of the same and of their management (Briozzo, Albanese, & Santolíquido, 2017; Hidalgo, García-Meca & Martínez, 2011; Sánchez Fernández de Valderrama, 2004).

In this context, the lack of theoretical consensus of generally accepted principles or of general measurement models, validated in their implementation by the scientific and professional community, has caused certain interpretative deviations concerning the evaluation of companies (Bueno Campos, 2002, p. 159; Tejedo-Romero & Araujo, 2015); this has caused, in some cases, differences between the market value and the value that appears in the annual accounts. Some authors (Alcaniz, Gomez-Bezares & Ugarte, 2015; Brooking, 1997; Edvinsson & Malone, 1999) justify said differences, among other things, with the lack of recognition of the Intellectual Capital (henceforth IC) in the evaluation of the companies, despite having become a key economic resource (Hidalgo & Garcíaj-Meca, 2009; Spagnol, Moraes & Piqueira, 2015; Villegas, Hernández & Salazar, 2017; Zerenler, Hasiloglu & Sezgin, 2008), originating in: the people (Human Capital, henceforth HC), the socioeconomic environment (Relational Capital, henceforth RC), and the organization (Structural Capital, henceforth SC), taking a critical role in the creation of value (de Cássia Fucci-Amato & Amato-Neto, 2010; Herrera & Macagnan, 2006; Villegas et al., 2017). Although the accounting information system plays a fundamental role as a generator and provider of information, in reality, it is not entirely useful for IC-Knowledge intensive companies (An, Davey, Eggleton & Wang, 2015; Brooking, 1997; Edvinsson & Malone, 1999). The balance sheet is no longer entirely explanatory of the business reality on which it intends to report, since the identification, measurement, and evaluation criteria no longer answer to the characteristics of the knowledge-based economy (Brennan, 2001; Herrera & Macagnan, 2016; Hidalgo & García-Meca, 2009; Tejedo-Romero & Araujo, 2015).

For this reason, a series of companies and institutions have leaned towards adopting a perspective that is not strictly financial for the evaluation of IC, complementing the annual financial statements with voluntary information. This requires better and more transparent visibility of the information disclosed by the companies, as it is a key element of good corporate governance. Thus, a good corporate governance would not be possible without an efficient accounting system, and the quality offered by accounting would not be reliable without an efficient corporate governance system (Briano & Saavedra, 2015; Briozzo et al., 2017; Rodríguez-Ariza et al., 2014; Sánchez Fernández de Valderrama, 2004). Therefore, in order to implement good corporate governance practices, promoting efficiency and transparency, equity in the treatment of the shareholders and information disclosure, as well as establishing effective internal control mechanisms, a significant wave of good governance codes (CNMV, 1998, 2003, 2006, 2013 and 2015) has occurred, for the promotion of ethical behaviors in the administrative and management bodies of the companies.

In this context, the objective of this work focuses on the study of the influence of the ownership structure and of particular characteristics of the board of directors of the companies on greater information transparency with regard to IC, seeking to contribute with greater knowledge to previous works in this field, regarding the changes experienced on company disclosure policy. The justification to consider the government of the company as a determinant factor, as indicated by Li, Pike and Haniffa (2008), is that the board of directors promotes the disclosure of information in the annual reports, therefore, its characteristics could be important to influence the IC disclosure policy.

To this end, and using the “content analysis” methodology, disclosure indices have been created, building four statistical models using the linear regression technique. These models allow determining the influence that the variables representative of the ownership structure and of the characteristics of the board of directors of the company exercise on the disclosure of information regarding IC, generally and particularly, of the HC, RC and SC. Furthermore, certain control variables such as size, indebtedness, and sector have been considered. For this purpose, and considering the entry into force of law 26/2003 of July 17th on information transparency, the annual reports of a sample of 23 listed companies included in the IBEX 35 stock index, for the years of 2004 to 2008, were selected; a total of 115 annual reports were analyzed. The 2009 to 2015 period was not included, left to future works, following the approval of law 16/2007 of July 4th on the reform and adaptation of commercial accounting legislation for its international harmonization based on EU standards, as well as coinciding, following its entry into force, with a series of mergers of companies listed in the IBEX 35 throughout the years 2009 and 2010, which would have distorted the historical series of the selected companies.

Furthermore, this empirical study has required significant research and data collection that, being highly specific, are scattered in various reports and whose disclosure depends, largely, on the corporate governance (board of directors). The results show that the percentage of shares held by significant shareholders, the size of the board, the separation of functions (as president and chief executive officer), the percentage of independent directors, size, level of indebtedness, and business sector influence the level of disclosure of IC information. Additionally, it is worth noting that the mean of the analyzed companies complies with the recommendations established by the 2006 Unified Code of Good Governance (henceforth CUBG, for its acronym in Spanish)

Approach of the investigation and development of hypothesis. Corporate Governance

With the globalization of the economy and the liberalization of the markets, such as the deregulation, privatization and sale of public companies, capital flows have increased, producing a greater dispersal of ownership of large companies due to the existence of a multitude of small and large (institutional) investors, who do not participate in their management, but who have gained the right to exercise a greater role in the supervision and control of the companies, which carries the associated risk of conflicts of interest (Berle & Means, 1932) between the parties. This conflict, according to the Agency Theory, is a network of relationships (agency relations) between shareholders and directors (Jensen & Meckling, 1976), which is considered central to the Governance problem of the listed companies. This theory is based on the fact that the directors (agents) cannot always act in benefit of the shareholders (principals), because their objectives are different. The solution to this agency problem requires the design of governance mechanisms that allow the efficient control of the management of the company (Briano & Saavedra, 2015; Briozzo et al., 2017; Hidalgo et al., 2011).

Therefore, with the purpose of improving the Good Governance of the listed companies, Good Governance Codes (CNMV, 1998, 2003, 2006, 2013 and 2015) have been redacted, including a series of recommendations and rules addressing the governments of the same, in order for them to voluntarily implement them (Babío & Muíño, 2005); thus, making the Board of Directors fulfill their function as an internal mechanism of supervision and control (Rodríguez-Ariza et al., 2014).

Consequently, and underpinned by ethics and transparency, Good Governance is an efficient means to avoid conflicts of interest and the existing imbalances between majority and minority shareholders, and between shareholders and directors. This has led companies to improve and increase transparency through a greater level of disclosed information, as well as greater accessibility and publicity, trying to restore, both to the markets and to society as a whole, the lost confidence.

Information on Intellectual Capital

In order to overcome the limitations of the current accounting regulations with regard to the identification, measurement and evaluation of IC, and to improve the usefulness of the information provided to the shareholders, it has been suggested that the companies voluntarily reveal it in sections; either as part of the annual report, since it is the main means of corporate communication for the future activities and intentions of the companies, or through so-called IC reports and Sustainability reports (An et al., 2015; Meritum, 2002; Rodrigues, Tejedo-Romero & Craig, 2016).

Thus, most works on IC disclosure have been based on the conceptual framework by Sveiby (1997) to define, classify, and record the information on said subject, being subsequently developed by Guthrie and Petty (2000), and applied to their studies carried out in Australia, and replicated by: Brennan (2001) in Ireland; Bozzolan et al. (2003)) in Italy; April, Bosma and Deglon (2003 and Wagiciengo and Belal (2012) in South Africa; Goh and Lim (2004) and Ahmed Haji and Mohd Ghazali (2013) in Malaysia; An et al. (2015) in China; Abeysekera and Guthrie (2005) in Sri Lanka; Vandemaele et al. (2005) in the Netherlands, Sweden and the United Kingdom; Oliveras and Kasperskaya (2005) and Alcaniz et al. (2015) in Spain; Rodrigues, Tejedo-Romero & Craig (2016) in Portugal; Hidalgo & García-Meca (2009) and Hidalgo et al. (2011) in Mexico; Herrera & Macagnan (2016) in Brazil and Spain; De Silva, Stratford and Clark (2014) in New Zealand, among others. These works show that, despite the lack of regulatory accounting standards on the recording of IC facts, companies are voluntarily providing related information. In this sense, our work is based on the theory of resources and capabilities, given that IC is the most important resource that a company possesses due to its strategic potential to generate competitive advantages (Hall, 1992; Wagiciengo & Belal, 2012). Many companies are interested on voluntarily providing information to highlight their competitive advantage (Ahmed Haji & Mohd Ghazali, 2013; Sonnier, 2008) and thus, obtain the support of investors in the capital market (Alcaniz et al., 2015; Tabares, Alvarez & Urbano, 2015).

Hypothesis development

The presence of various problems in the Good Governance of companies can, in some cases, be due to shortcomings in their reporting and disclosure policy (Whittington, 1993), with the quantity and quality of the information being fundamental to reduce information asymmetries and managerial discretion, since they limit the free action of the administration and management, and encourage manipulative practices (Babío & Muiño, 2005; Prado, García & Gallego-Álvarez, 2009; Rodríguez-Ariza et al., 2014; Rodrigues, Tejedo-Romero & Craig, 2016). To this end, and with the Agency Theory as its basis, the ownership structure and characteristics of the Board of directors are studied as influential factors in the disclosure of IC information.

Ownership structure takes on particular importance due to both the degree of concentration or dispersion of the ownership, and the shareholding of executives and directors. It is defined as the degree of participation in the ownership of the company, which determines the distribution of power and control (Briano & Saavedra, 2015). Thus, a high dispersion of share ownership (a large number of small shareholders) assumes a greater separation between ownership and management, resulting in high agency costs due to these being far removed from the power structure, and the decline in their exercise and participation in the management and control of the company, deriving towards the existence of information asymmetries. According to Eng and Mak (2003), greater supervision and control on behalf of the minority shareholders is necessary, which requires greater disclosure of information and, consequently, of IC. In view of this approach, the first hypothesis is proposed:

H1: There is a negative association between the shareholder concentration and the level of disclosure of IC information.

Furthermore, certain characteristics of the Board of Directors encourage the articulation of rules and behaviors that can help improve the tasks of supervision and control and, consequently, lead to an increase in information transparency and in the confidence of future investors, thus reducing the possible conflict of interest between insiders (agent) and outsiders (principal).

The existence of independent directors can promote the making of decisions directed towards voluntarily revealing IC information (Babío & Muíño, 2005; Barako, Hancock & Izan, 2006; Briano & Saavedra, 2015; Cerbioni & Parbonetti, 2007; Chen & Jaggi, 2000; Gisbert & Navallas, 2013; Hidalgo et al., 2011; Ho & Wong, 2001; Li et al., 2008; Lim, Matolcsy & Chow, 2007) in the annual reports, reducing the information asymmetries between the directors and shareholders (Hidalgo et al., 2011; Lim et al., 2007); since more objectivity and independence is expected in the analysis of the management and behavior of the company on behalf of the independents (Rodríguez-Ariza et al., 2014). Therefore, this characteristic of the Board tends to improve its decision-making capacity for supervision and control to alleviate agency conflicts between owners-shareholders and directors, and increase the level of disclosure of IC information. Thus, the following hypothesis is proposed:

H2: There is a positive association between the independence of the Board of Directors and the level of disclosure of IC information.

When the positions of chairman of the board and chief executive officer are held by the same person, it could give rise to inefficient and opportunistic behaviors (Jensen & Meckling, 1976), caused by the excessive concentration of power; although in theory, it ought to encourage the disclosure of information in order to reduce coordination costs (Coles, Daniel & Naveen, 2008; Hidalgo et al., 2011; Jensen, 1993). Li et al. (2008) argue that the duality in the position can limit the independence of the Board, thus placing the control and supervision functions that affect the information disclosure policy of the company at risk. The concentration of too much power in the hands of a single person can give rise to inefficient and opportunistic behaviors (Jensen & Meckling, 1976), favoring personal interests to the detriment of the company (Prado et al., 2009). The third hypothesis to corroborate is:

H3: The disclosure of IC information is positively correlated to the separation of the functions of the chief executive and chairman of the board.

A unanimous position is not detected in previous literature in relation to the size of the Board of Directors when guaranteeing the efficiency in its supervision and control role (Rodrigues, Tejedo-Romero & Craig, 2016). Some authors, such as Pearce and Zahra (1992), believe that a large Board size favors the diversity of opinions and the level of voluntary disclosure of information. In this same line, Briano and Saavedra (2015), Gisbert and Navallas (2013), and Hidalgo et al. (2011) find a positive association between the size of the Board and the level of voluntary disclosure of information. However, Jensen (1993) considers that this becomes a reduction in speed and efficiency in decision-making due to a lack of coordination and information. Although a large number of members in the Board could assume a greater capacity of supervision, this can be diminished by a lengthening of the decision-making process and of the communication procedure (Jensen, 1993) and, therefore, would be negatively correlated to the information transparency of the IC. In this sense, Cerbioni and Parbonetti (2007) and Lim et al. (2007) find a negative association between the size of the Board and the level of voluntary information. Thus, the following hypothesis is proposed:

H4: The disclosure of IC information is negatively correlated to the size of the Board of Directors.

Methodological design and data collection

This empirical study (for the contrast of hypotheses) utilized the content analysis methodology (April et al., 2003; Beattie & Thomson, 2007; Bozzolan et al., 2003;Guthrie, Petty, Yongvanich & Ricceri, 2004; Tejedo-Romero & Araujo, 2015), the techniques of which have served as the basis for the elaboration of a disclosure index and three sub-indices (Rodrigues, Tejedo-Romero & Craig, 2016) in order to quantify the IC information, generally and particularly, of the HC, RC and SC of the companies being studied.

To guarantee the reliability of the content analysis, we took into account the indications of Guthrie et al. (2004), which consider that for the case of a single encoder, if it has been subject to a sufficient formation period and the codification decisions have achieved an acceptable level in the pilot sample carried out, the reliability can be proven in the depuration process of the data. Nevertheless, to address the lack of transparency in the codification of the same (Beattie & Thomson, 2007), the following stages have been carried out.

Period of study

The chosen period covers 5 years, from 2004 to 2008 (including both years completely). As previously stated, this choice is reasoned by the approval in Spain of law 26/2003 of July 17th on information transparency, which regulates all issuers of securities and financial instruments admitted to listing, where it is stated, in section 2 of article 117, that said issuing companies must have a website to disclose information; facilitating, from 2004 onward, access to the analyzed documents.

Definition of the population and choice of sample

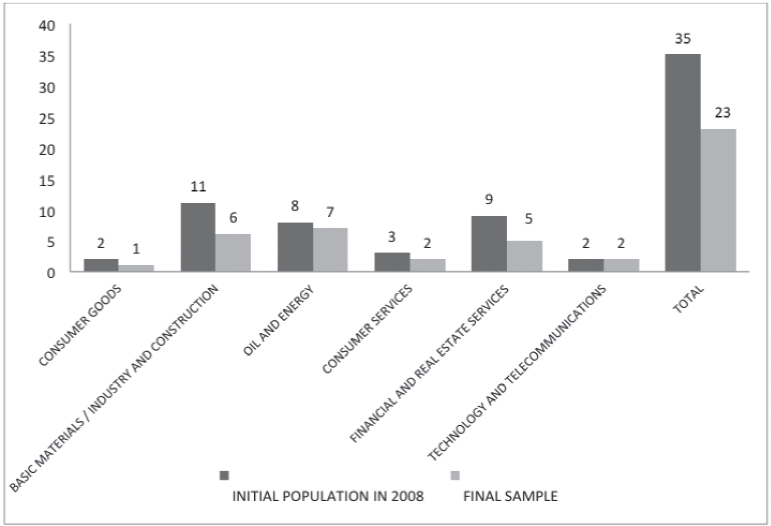

Companies listed in the Spanish continuous market that were included in the IBEX 35 stock index during the 2004-2008 period comprise the starting population, due to these being more susceptible to greater information transparency (Hernández, Aibar & Aibar, 2015). IBEX 35 is the main reference stock index of the Spanish stock exchange. It is comprised of the 35 companies with most liquidity listed in the stock exchange; these being the ones that possess a greater trading volume and market capitalization. In the selection process of the sample, we opted for a targeted or non-probabilistic design (Hernández, Fernández & Baptista, 2006), parting from the companies included in the 2008 index and maintaining them fixed throughout the rest of the analyzed years, up to 2004. The year 2008 was selected in order to obtain a significant sample of the companies in the IBEX 35, given that mergers have taken place in subsequent years and some companies have dropped out of the index. Thus, the sample was comprised of 23 business groups, having information at the group level, 65.7% consolidated of the starting population. Similarly, all industrial sectors are characterized (see Figure 1).

Measurement of the variables and data collection

In order to corroborate the previously presented hypotheses, the dependent variables considered for the four statistic models (which are specified below) are: the level of disclosure of IC information, generally and particularly, of HC, RC and SC, provided by the companies in their annual reports or accounts. These variables have been measured using unweighted disclosure indices and sub-indices based on the results obtained from the content analysis of the annual reports. Thus, the sampling units are the annual reports, the recording units are the presence or absence of IC information, and the context units have been the data analyzed at the phrase level. For data coding, the initial framework by Sveiby (1997) was followed. Thus, a tripartite IC model is used, in which each category (HC, RC and SC) is comprised of a series of subcategories and specific elements based on previous literature (see Table 1).

Table 1 Categories, subcategories, and intangible elements

| IC | ||

|---|---|---|

| HC | RC | SC |

| EMPLOYEES: Employee profile Economic Data Employee health and safety Work relations and union activity Employee involvement with the community Employee recognition Outstanding employees Issues of equal opportunities and diversity Employee behavior Employee commitments Employee motivation EDUCATION: Formal education Professional qualifications TRAINING AND DEVELOPMENT: Employee training Employee development WORK-RELATED KNOWLEDGE: Know-how Professional experience Seniority of experts Achievement and performance of senior management ENTREPRENEURIAL SPIRIT | FINANCIAL RELATIONS BRANDS CUSTOMERS: Names of relevant customers Customer loyalty Customer satisfaction Customer services and support COMPANY REPUTATION/IMAGE: Company name Favorable contracts Environmental protection measures Sponsorship and patronage Social responsibility/social action Corporate governance BUSINESS PARTNERS: Collaboration with companies Franchise agreements License agreements OTHER COMPANY RELATIONS: Supplier relations Relations with public administrations Relations with research centers Relations with media outlets Relations with other interest groups DISTRIBUTION CHANNELS | INTELLECTUAL PROPERTY: Patents Copyrights Trademarks Trade secrets MANAGEMENT PHILOSOPHY CORPORATE CULTURE TECHNOLOGICAL AND MANAGEMENT PRO- CESSES: Management processes Technological Processes R+D+i: Research and Development Innovation INFORMATION AND NETWORKING SYSTEMS: Information systems Networking systems |

Based on the previous framework, the general IC index (ICI), three sub-indices corresponding to the HC (HCI), RC (RCI) and SC (SCI) were elaborated, configuring each of these as follows:

Where I j are the absolute index and indices of unweighted disclosure of company j; i are the items or lines; j is the company; and Xji is the score for item i in company j. So that, Xij takes the value of 1 if company j has disclosed item i, and takes the value of 0 otherwise.

Regarding the independent variables, the necessary data are obtained from the annual reports on Corporate Governance. The measurement of these variables is described below:

Table 2 Independent variables

| VARIABLE | MEASURE |

| Shareholder concentration | - Numeric variable that represents the holding of shares by a natural person or legal entity ≥ 5% of the capital. |

| Independence of the Board of Directors | - Numeric variable that represents the percentage of independent directors in the Board of Directors. |

| Separation of the functions of the Chief Executive and the Chairman of the Board | - Dummy variable that takes the value of 1 when there is a separation of functions, and the value of 0 otherwise. |

| Size of the Board of Directors | - Numeric variable that represents the total number of members that comprise the Board of Directors. |

Moreover, certain business characteristics have been considered, such as the control variables (Alcaniz et al., 2015; Chen & Jaggi, 2000; Rodrigues, Tejedo-Romero & Craig, 2016), given that they are necessary to isolate the effect of the characteristics of the Board of Directors on the level of disclosure of IC information. The data collection was carried out using the Iberian Balance Sheet Analysis System (SABI for its acronym in Spanish) database.

Size: Has been measured as the Nepali logarithm of the number of employees (Alcaniz et al., 2015; Bozzolan et al., 2003).

Sector: Dichotomous variables have been considered for each of the sectors, that is, it takes a value of 1 if the company belongs to the sector in question and a value of 0 otherwise (Hidalgo & García-Meca, 2009; Rodrigues, Tejedo-Romero & Craig, 2016).

Indebtedness: Is measured as the quotient between the total amount of debt and the net equity (Cerbioni & Parbonetti, 2007). Furthermore, the year has been included as a control variable.

Research model

In line with the above, to obtain the variables that contribute in explaining the variability of the information index (IC) and sub-indices (HC, RC and SC) to a greater extent, four multiple linear regression statistical models were used, which allow, given a dependent variable to explain and a set of independent variables, to obtain a linear function of such variables with which it is possible to explain or predict the value of the dependent variable. To this end, the following four statistical models are created:

Model 1:

Model 2:

Model 3:

Model 4:

Results and discussion

First of all, a descriptive analysis was carried out to make an approximation to the behavior of the variables of the models through their main statistics.

Table 3 Descriptive statistics of the corporate governance dependent and independent variables

| N | Minimum | Maximum | Mean | Stan. Dev. | Median | ||

|---|---|---|---|---|---|---|---|

| Dependent variables | |||||||

| ICI | 115 | 0 | 0.698 | 0.417 | 0.198 | 0.491 | |

| ICH | 115 | 0 | 0.800 | 0.386 | 0.219 | 0.450 | |

| ICR | 115 | 0 | 0.762 | 0.407 | 0.203 | 0.476 | |

| ICE | 115 | 0 | 0.917 | 0.487 | 0.234 | 0.583 | |

| Independent variables | |||||||

| % of Significant Shareholders | 115 | 0% | 92.06% | 30.92% | 23.88% | 27.46% | |

| % of Independent Directors in the Board of Directors | 115 | 9.09% | 80% | 40.66% | 17.03% | 41.18% | |

| Size of the Board | 115 | 8 | 24 | 14.99 | 3.84 | 15 | |

| Independent variables | |||||||

| % of Significant Shareholders | 115 | 0% | 92.06% | 30.92% | 23.88% | 27.46% | |

| % of Independent Directors in the Board of Directors | 115 | 9.09% | 80% | 40.66% | 17.03% | 41.18% | |

| Size of the Board | 115 | 8 | 24 | 14.99 | 3.84 | 15 | |

| N | Frequency | Percentage | Accumulated percentage | Mean | Stand. Dev. | ||

| Separation of Functions | No Separation | 86 | 74.8 | 74.8 | 0.252 | 0.436 | |

| Separation | 29 | 25.2 | 100 | ||||

The results show that, despite being immersed in the Knowledge Society, little IC information is disclosed, with a mean of 39%, 41% and 49%, at the information level of HC, RC and SC, respectively. These results are similar to those obtained in previous works of other countries: in Australia (Guthrie & Petty, 2000), Ireland (Brennan, 2001), South Africa (April et al., 2003), Sweden, the Netherlands and the United Kingdom (Vandemaele et al., 2005), with 30%, 40% and 30%, respectively; in Italy (Bozzolan et al., 2003) with 21%, 49% and 30%, respectively; in Sri Lanka (Abeysekera & Guthrie, 2005) with 36%, 44% and 20%, respectively; in Malaysia (Goh and Lim, 2004) with 22%, 41% and 37%, respectively; and in Spain (Oliveras & Kasperskaya, 2005) with 21%, 51% and 28%, respectively. Thus, under the assumptions of the theory of resources and capabilities, the companies are afraid of losing their competitive advantage that has its origin in the most important strategic resource they possess, their IC, and can perhaps be the reason for the limited disclosure.

Finally, the estimation of the linear regression statistical model is carried out using the “forward” staged regression method, in which the input and output of the independent variables in the regression equation is done based on the values of the t-Student statistic. The standardized coefficient for each variable is calculated at every step if it were to be entered into the model in the following step, as well as the value of the t statistic and the level of significance. A level of significance below 0.05 and an output greater than 0.1 are used in this work as an entry criterion in the equation. In this sense, the results (see Table 4) obtained from the four statistical models are presented after having complied with the assumptions of linearity, independence, homoscedasticity, normalcy, and non-multicollinearity for their correct implementation.

Table 4 Results of the linear regression models

| Variables | Model 1 IC | Model 2 HC | Model 3 RC | Model 4 SC | ||||

|---|---|---|---|---|---|---|---|---|

| β | t | β | t | β | t | β | t | |

| (Constant) | 9.975*** | 1.868* | 7.715*** | 2.000** | ||||

| % Acc. of significant minutes | 0.227 | 2.509** | ||||||

| % of independent directors | -0.225 | -2.675*** | ||||||

| Separation of functions | 0.365 | 3.983*** | 0.417 | 4.584*** | 0.281 | 3.070*** | ||

| Size of the Board of Directors | -0.475 | -4.989*** | 0.361 | -4.352*** | -0.378 | -4.144*** | -0.314 | -3.444*** |

| No. of employees | 0.454 | 5.190*** | 0.573 | 6.148*** | 0.367 | 4.073*** | ||

| % of indebtedness | .593 | 5.674*** | 0.392 | 3.450*** | ||||

| Consumer services | -0.257 | -3.199*** | -0.397 | -5.070*** | -0.236 | -2.915*** | -0.216 | -2.683*** |

| Consumer goods | -0.208 | -2.484** | ||||||

| Financial and real estate services | -0.481 | -4.571*** | -0.424 | -3.778 | ||||

| R 2 | 0.329 | 0.390 | 0.340 | 0.355 | ||||

| Adjusted R 2 | 0.298 | 0.362 | 0.310 | 0.320 | ||||

| F | 10.689*** | 13.943*** | 11.237*** | 9.922*** |

*** = Significant for p<0.01; ** = Significant for p<0.05; * = Significant for p< 0.1

Regarding the provision of IC information, it is observed that there are four variables that help explain the levels of information: 1) The size of the Board is decisive for the level of IC information ( β =-0.475, sig.=0.000), the larger the size the less information is disclosed, and is recognized at both the theoretical (Agency Theory) and empirical (Babío & Muíño, 2005; Cerbioni & Parbonetti, 2007; Lim et al., 2007) levels, corroborating the fourth hypothesis; 2) The separation of functions, of the Chief Executive and the Chairman of the Board, is statistically significant ( β =0.365, sig.=0.000), which implies a greater level of disclosure of IC information (Barako & Brown, 2008; Cerbioni & Parbonetti, 2007; Li et al., 2008), thus confirming the third hypothesis; 3) The size of the company is decisive ( β =0.454, sig.=0.000) for the justification of greater levels of disclosure of IC information (Barako et al., 2006; Bozzolan et al., 2003; Haniffa & Cooke, 2005; Ho & Wong, 2001). At a sectoral level, it is observed that the consumer goods and services maintain differential behaviors ( β =-0.257, sig.=0.002; β =- 0.208, sig.=0.015, respectively) with regard to the other sectors, with these being the ones that disclose the least amount of IC information, given that these are not very intensive sectors in this type of capital (OECD, 2001).

The fit of the IC statistical model measured by the adjusted R 2 increases to 0.298, implying that the independent variables explain 29.8% of the variance of the level of disclosure of the IC information. This value is very similar to that obtained in the studies by Chen and Jaggi (2000) with 30%, Ho and Wong (2001) with 31.4%, Lim et al. (2007) with 18.79%.

Regarding the provision of HC information, the variables that help explain the levels of information are: the size of the Board which is decisive for the level of information, the larger the size the less information is disclosed ( β =-0.361, sig.=0.000). Additionally, as is the case in previous works (Eng & Mak, 2003; Haniffa & Cooke, 2005), a greater % of independent directors in the Board involves a lower level of information supplied ( β =-0.225, sig.=0.009) since, as Li et al. (2008) argue, non-executive directors may not necessarily be as independent. Furthermore, the level of indebtedness ( β =0.593, sig.=0.000) and the consumer service and the financial and real estate sectors are also significant ( β =-0.397, sig.=0.000; β =-0.481, sig.=0.000, respectively). In this model, the adjusted R 2 increases to 0.362, which implies that the independent variables explain 36.2% of the variance of the level of disclosure of the HC information, corroborating hypotheses H2 and H4.

Concerning the provision of RC information, and as is the case of model 1 relative to the IC information, the significant variables that help explain the levels of information are: the size of the Board, the separation of functions, the size of the company, and the consumer services sector ( β =-0.378, sig.=0.000; β =0.417, sig.=0.000; β =0.573, sig.=0.000; β =-0.236, sig.=0.004, respectively). The variable % of shares held by significant shareholders ( β =-0.227, sig.=0.014) also resulted significant, implying a greater level of information supplied (Eng & Mak, 2003). Regarding the adjustment, this statistical model presents an adjusted R 2 that increases to 0.310, which implies that the independent variables explain 31% of the variance of the level of disclosure of the RC information. Thus, hypotheses H1, H3, and H4 are confirmed. The variables that help explain the supplied SC information are: the size of the Board, the separation of functions, the size of the company, and the consumer services sector ( β =-0.314, sig.=0.001; β =0.281, sig.=0.003; β=0.367, sig.=0.000; β =-0.216, sig.=0.008, respectively), as was the case of the information relative to the IC and RC. Similarly, and as is the case of HC, the level of indebtedness ( β =0.392, sig.=0.001) resulted statistically significant, with a positive relation (Barako et al., 2006; Eng & Mak, 2003), and the financial and real estate sector ( β =- 0.424, sig.=0.000), which is not very intensive in intangibles (OECD, 2001). The adjusted R 2 increases to 0.320, which implies that the independent variables explain 32% of the variance of the level of disclosure of the SC information, corroborating hypotheses H3 and H4.

Conclusions

This empirical study evidences how the existence of particular characteristics of Corporate Governance, relative to the ownership structure and the Board of Directors, affect the voluntary disclosure of information regarding IC. The results confirm that the existence of particular recommendations established in Spain in the CUBG (CNMV, 2006, 2013, 2015) provide the control mechanisms necessary to increase the degree of information transparency, in the interest of a Good Corporate Governance as a means to avoid possible conflicts of interest from the point of view of the Agency Theory.

Therefore, Corporate Governance plays a fundamental role as a mechanism to reduce the information asymmetries and the agency costs, when voluntarily disclosing IC information. Concretely, it has been evidenced that the percentage of shares held by significant shareholders, the size of the Board of Directors, the separation of functions (of the chief executive and the chairman of the board), and the percentage of independent directors -members of the Board of Directors-, influence the level of disclosure of information. Similarly, it has been evidenced how certain business characteristics such as size, sector and indebtedness influence the provision of more voluntary information.

In this sense, it has been confirmed that a greater number of members of the Board prejudices the levels of disclosure of IC, HC, RC and SC information provided by the company. That is to say, a larger size of the Board has a negative impact on the effectiveness of the same, as the directors could be less motivated to participate in strategic decision-making and reveal less information. Additionally, the separation of functions is a useful mechanism to safeguard the interest of all the parties involved, improving supervision and the amount of information disclosed relative to IC, RC and SC. Similarly, a greater number of independent directors negatively influence the provision of HC information; this could be due to the fact that these directors are not as independent as initially thought, or because their presence in the Board of Directors (which guarantees the interest of the minority shareholders and of the other stakeholders) could be the reason why the minority shareholders demand less information, having placed great trust in the independents and, consequently, the company discloses less. Finally, a high degree of concentration of property held by the main shareholders benefits the disclosure of RC information. This could be due to them being interested in disclosing RC information in order to increase the liquidity and value of the company shares.

With these results, and within the framework of the Agency Theory, the intention of this work has been to contribute to the study of Corporate Governance mechanisms and their influence on the disclosure of IC information, clarifying the situation in Spain due to the lack of previous works. Moreover, this contribution is of great strategic use for the reduction of the agency problem, which may be referred to in future recommendations and modifications in the existing codes, being of interest to regulators, financial analysts, investors, and capital market participants, etc.

In this sense, our work has tried to provide evidence on the advisability of promoting Good Corporate Governance, the codes of conduct, and ethical behaviors in the management and administrative bodies of companies, in order to increase information transparency. Furthermore, it is also our intention to evidence the benefit that entails for the rest of the Spanish companies, knowing the performance of the senior management and the importance of voluntarily disclosing IC information, as well as the decisive factors for this major level of information.

Finally, we indicate that a future work will focus on completing the methodology of the content analysis using a methodological triangulation, elaborating a questionnaire directed to those in charge of creating the annual reports or accounts. We would additionally like to broaden the sample under study in an international context, studying the possible differences concerning the corporate governance mechanisms in each of the analyzed countries, and expand the period of study by incorporating more current data corresponding to the 2009-2017 period.

Referencias

Abeysekera, I., & Guthrie, J. (2005). An empirical investigation of annual reporting trends of intellectual capital in Sri Lanka. Critical Perspectives on Accounting, 16(3), 151-163. http://dx.doi.org/10.1016/s1045-2354(03)00059-5. [ Links ]

Ahmed Haji, A., & Mohd Ghazali, N. A. (2013). A longitudinal examination of intellectual capital disclosures and corporate governance attributes in Malaysia. Asian Review of Accounting, 21(1), 27-52. https://doi.org/10.1108/13217341311316931 [ Links ]

Alcaniz, L., Gomez-Bezares, F., & Ugarte, J. V. (2015). Firm characteristics and intellectual capital disclosure in IPO prospectuses. Academia Revista Latinoamericana de Administración, 28(4), 461-483. https://doi.org/10.1108/arla-09-2014-0134 [ Links ]

An, Y., Davey, H., Eggleton, I. R., & Wang, Z. (2015). Intellectual capital disclosure and the information gap: Evidence from China. Advances in Accounting, 31(2), 179-187. https://doi.org/10.1016/j.adiac.2015.09.001 [ Links ]

April, K. A., Bosma, P., & Deglon, D. A. (2003). IC measurement and reporting: Establishing a practice in SA mining. Journal of Intellectual Capital, 4(2), 165-180. https://doi.org/10.1108/14691930310472794 [ Links ]

Babío, M. R., & Muíño, M. F. (2005). Corporate Characteristics, Governance Rules and the Extent of Voluntary Disclosure in Spain. Advances in Accounting, 21, 299-331. https://doi.org/10.1016/s0882-6110(05)21013-1 [ Links ]

Barako, D. G., & Brown, A. M. (2008). Corporate social reporting and board representation: evidence from the Kenyan banking sector. Journal of Management and Governance, 12(4), 309-324. https://doi.org/10.1007/s10997-008-9053-x [ Links ]

Barako, D. G., Hancock, P., & Izan, H. Y. (2006). Relationship between corporate governance attributes and voluntary disclosures in annual reports: the Kenyan experience. Financial Reporting Regulation and Governance, 5(1), 1-27. [ Links ]

Beattie, V., & Thomson, S. J. (2007). Lifting the lid on the use of content analysis to investigate intellectual capital disclosures. Accounting Forum, 31(2), 129-163. https://doi.org/10.1016/j.accfor.2007.02.001 [ Links ]

Berle, A. A., & Means, G. C. (1932). The Modern Corporation and Private Property. New York: Macmillan. [ Links ]

Bozzolan, S., Favotto, F., & Ricceri, F. (2003). Italian annual intellectual capital disclosure: An empirical analysis. Journal of Intellectual Capital, 4(4), 543-558. https://doi.org/10.1108/14691930310504554 [ Links ]

Brennan, N. (2001). Reporting intellectual capital in annual reports: Evidence from Ireland. Accounting, Auditing & Accountability Journal, 14(4), 423-436. https://doi.org/10.1108/09513570110403443 [ Links ]

Briano, G.C., & Saavedra, M. L. (2015). The composition of the board and ownership structure as explanatory factors of transparency in corporate governance in Latin America: Evidence from listed companies in Argentina, Brazil, Chile and Mexico. Estudios Gerenciales, 31(136), 275-286. https://doi.org/10.1016/j.estger.2015.02.001 [ Links ]

Briozzo, A., Albanese, D., & Santolíquido, D. (2017). Gobierno corporativo, financiamiento y género: un estudio de las pymes emisoras de títulos en los mercados de valores argentinos. Contaduría y Administración, 62(2), 339-357. https://doi.org/10.1016/j.cya.2017.01.005 [ Links ]

Brooking, A. (1997). El capital intelectual: el principal activo de las empresas del tercer milenio. Barcelona: Paidós Empresa. [ Links ]

Bueno Campos, E. (2002). El Capital Social en el nuevo enfoque del Capital intelectual de las organizaciones. Revista de Psicología del Trabajo y las Organizaciones, 18(2-3), 157-176. [ Links ]

Cerbioni, F., & Parbonetti, A. (2007). Exploring the Effects of Corporate Governance on Intellectual Capital Disclosure: An Analysis of European Biotechnology Companies. European Accounting Review, 16(4), 791 - 826. https://doi.org/10.1080/09638180701707011 [ Links ]

Chen, C. J. P., & Jaggi, B. (2000). Association between independent non-executive directors, family control and financial disclosures in Hong Kong. Journal of Accounting and Public Policy, 19(4-5), 285-310. https://doi.org/10.1016/s0278-4254(00)00015-6 [ Links ]

CNMV (1998). Informe del Comité Olivencia sobre el Gobierno de las Sociedades. Madrid: Consejo de Ministros [ Links ]

CNMV. (2003). Informe de la Comisión Especial para el fomento de la transparencia y seguridad en los mercados y en las sociedades cotizadas. Madrid: Consejo de Ministros. [ Links ]

CNMV (2006): Informe del grupo especial de trabajo sobre buen gobierno de las sociedades cotizadas. Madrid: Ministerio de Economía y Hacienda. [ Links ]

CNMV (2013): Código Unificado de Buen Gobierno de las empresas cotizadas. Madrid: Ministerio de Economía y Hacienda. [ Links ]

CNMV (2015): Unified code of corporate governance. Informe del grupo especial de trabajo sobre buen gobierno de las sociedades cotizadas. Madrid: Ministerio de Economía y Hacienda. [ Links ]

Coles, J. L., Daniel, N. D., & Naveen, L. (2008). Boards: Does one size fit all? Journal of Financial Economics, 87(2), 329-356. https://doi.org/10.1016/j.jfineco.2006.08.008 [ Links ]

de Cássia Fucci-Amato, R., & Amato-Neto, J. (2010). A influência do capital humano e do capital intelectual no desenvolvimento de aglomerações de empresas e redes de cooperação produtiva. Journal of Technology Management & Innovation, 3(2), 56-66. [ Links ]

De Silva, T. A., Stratford, M., & Clark, M. (2014). Intellectual capital reporting: a longitudinal study of New Zealand companies. Journal of Intellectual Capital, 15(1), 157-172. https://doi.org/10.1108/jic-03-2013-0034 [ Links ]

Edvinsson, L., & Malone, M. S. (1999). El capital intelectual: Cómo identificar y calcular el valor de los recursos intangibles de su empresa. Barcelona: Gestión 2000. [ Links ]

Eng, L. L., & Mak, Y. T. (2003). Corporate governance and voluntary disclosure. Journal of Accounting and Public Policy, 22(4), 325-345. https://doi.org/10.1016/S0278-4254(03)00037-1 [ Links ]

Gisbert, A., & Navallas, B. (2013). The association between voluntary disclosure and corporate governance in the presence of severe agency conflicts. Advances in Accounting, 29(2), 286-298. https://doi.org/10.1016/j. adiac.2013.07.001 [ Links ]

Goh, P. C., & Lim, K. P. (2004). Disclosing intellectual capital in company annual reports: Evidence from Malaysia. Journal of Intellectual Capital, 5(3), 500-510. https://doi.org/10.1108/14691930410550426 [ Links ]

Guthrie, J., & Petty, R. (2000). Intellectual capital: Australian annual reporting practices. Journal of Intellectual Capital, 1(3), 241-251. https://doi.org/10.1108/14691930010350800 [ Links ]

Guthrie, J., Petty, R., Yongvanich, K., & Ricceri, F. (2004). Using content analysis as a research method to inquire into intellectual capital reporting. Journal of Intellectual Capital, 5(2), 282-293. https://doi.org/10.1108/14691930410533704 [ Links ]

Hall, R. (1992). The strategic analysis of intangible resources. Strategic Management Journal, 13(2), pp. 135-144. https://doi.org/10.1002/smj.4250130205 [ Links ]

Haniffa, R. M., & Cooke, T. E. (2005). The impact of culture and governance on corporate social reporting. Journal of Accounting and Public Policy, 24(5), 391-430. https://doi.org/10.1016/j.jaccpubpol.2005.06.001 [ Links ]

Hernández, M., Aibar, B., & Aibar, C. (2015). Determinants of corporate risk disclosure in large Spanish companies: a snapshot. Contaduría y Administración, 60(4), 757-775. https://doi.org/10.1016/j.cya.2015.05.014 [ Links ]

Hernández, R., Fernández, C., & Baptista, P. (2006). Metodología de la Investigación. México: McGraw-Hill Interamericana. [ Links ]

Herrera, E. E., & Macagnan, C. B. (2016). Revelación de informaciones sobre capital estructural organizativo de los bancos en Brasil y España. Contaduría y administración, 61(1), 4-25. https://doi.org/10.1016/j.cya.2015.09.007 [ Links ]

Hidalgo, R. L., & García-Meca, E. (2009). Divulgación de información sobre el capital intelectual de empresas nacionales que cotizan en la Bolsa Mexicana de Valores. Contaduría y administración, (229), 105-131. http://dx.doi.org/10.22201/fca.24488410e.2009.658 [ Links ]

Hidalgo, R. L., García-Meca, E., & Martínez, I. (2011). Corporate governance and intellectual capital disclosure. Journal of Business Ethics, 100(3), 483-495. https://doi.org/10.1007/s10551-010-0692-x [ Links ]

Ho, S. S. M., & Wong, K. S. (2001). A study of the relationship between corporate governance structures and the extent of voluntary disclosure. International Journal of Accounting, Auditing and Taxation, 10(2), 139-156. https://doi.org/10.1016/s1061-9518(01)00041-6 [ Links ]

Jensen, M. C. (1993). The modern industrial revolution, exit, and the failure of internal control systems. Journal of Finance, 48(3), 831-880. http://dx.doi.org/10.1111/j.1540-6261.1993.tb04022.x [ Links ]

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X [ Links ]

Li, J., Pike, R., & Haniffa, R. (2008). Intellectual capital disclosure and corporate governance structure in UK firms. Accounting and Business Research, 38(2), 137-159. https://doi.org/10.1080/00014788.2008.9663326 [ Links ]

Lim, S., Matolcsy, Z., & Chow, D. (2007). The Association between Board Composition and Different Types of Voluntary Disclosure. European Accounting Review, 16(3), 555 - 583. https://doi.org/10.1080/09638180701507155 [ Links ]

Meritum (2002). Guidelines for managing and reporting on intangibles. Fundación Airtel-Vodafone. [ Links ]

OECD, Organisation for Economic Co-operation and Development. (2001). OECD Science, Technology and Industry Scoreboard 2001: Towards a Knowledge-based Economy. Paris: OECD Publishing. [ Links ]

Oliveras, E., & Kasperskaya, Y. (2005). Reporting Intellectual Capital in Spain Economics and Business Working Papers Series 781. Barcelona: Universidad Pompeu Fabra. [ Links ]

Pearce, J. A., & Zahra, S. A. (1992). Board compensation from a strategic contingency perspective. Journal of Management Studies (29), 411-438. [ Links ]

Prado, J. M., García, I. M. & Gallego-Álvarez, I. (2009). Características del consejo de administración e información en materia de responsabilidad social corporativa. Revista Española de Financiación y Contabilidad, 38(141), 107-135. https://doi.org/10.1080/02102412.2009.10779664 [ Links ]

Rodrigues, L. L., Tejedo-Romero, F., & Craig, R. (2016). Corporate governance and intellectual capital reporting in a period of financial crisis: Evidence from Portugal. International Journal of Disclosure and Governance. https://doi.org/10.1057/jdg.2015.20 [ Links ]

Rodríguez-Ariza, L., Frías, J. V. & García, R. (2014). El consejo de administración y las memorias de sostenibilidad. Revista de Contabilidad, 17(1), 5-16. https://doi.org/10.1016/j.rcsar.2013.02.002 [ Links ]

Sánchez Fernández de Valderrama, J. L. (2004). Información corporativa, opciones contables y análisis financiero: Publicaciones de la Real Academia de las Ciencias Económicas y Financieras. [ Links ]

Sonnier, B.M. (2008). Intellectual capital disclosure: high-tech versus traditional sector companies. Journal of Intellectual Capital, 9(4), 705-722. https://doi.org/10.1108/14691930810913230 [ Links ]

Spagnol, R., Moraes, R. D. O., & Piqueira, J. R. C. (2015). Knowledge Management as a Competitive Advantage to the Brazilian MVAS Ecosystem. Journal of Technology Management & Innovation, 10(2), 1-8. http://dx.doi.org/10.4067/S0718-27242015000200001 [ Links ]

Sveiby, K. E. (1997). The intangible assets monitor. Journal of Human Resource Costing and Accounting, 2(1), 73-97. https://doi.org/10.1108/eb029036 [ Links ]

Tabares, A., Alvarez, C., & Urbano, D. (2015). Born Globals From the Resource-Based Theory: a Case Study in Colombia. Journal of Technology Management & Innovation, 10(2), 155-165. https://doi.org/10.4067/s0718- 27242015000200011 [ Links ]

Tejedo-Romero, F. & Araujo, J. F. (2015). A gestão da informação do conhecimento organizacional das empresas. Observatorio (OBS*), 9(2), 189-205. [ Links ]

Vandemaele, S. N., Vergauwen, P. G. M. C., & Smits, A. J. (2005). Intellectual capital disclosure in The Netherlands, Sweden and the UK: A longitudinal and comparative study. Journal of Intellectual Capital, 6(3), 417-426. https://doi.org/10.1108/14691930510611148 [ Links ]

Villegas González, E., Hernández Calzada, M. A., & Salazar Hernández, B. C. (2017). La medición del capital intelectual y su impacto en el rendimiento financiero en empresas del sector industrial en México. Contaduría y Administración, 62(1), 184-206. https://doi.org/10.1016/j.cya.2016.10.002 [ Links ]

Wagiciengo, M. M., & Belal, A. R. (2012). Intellectual capital disclosures by South African companies: A longitudinal investigation. Advances in Accounting, 28(1), 111-119. https://doi.org/10.1016/j.adiac.2012.03.004 [ Links ]

Whittington, G. (1993). Corporate Governance and the Regulation of Financial Reporting Accounting and Business Research, 23(91A), 311-319. https://doi.org/10.1080/00014788.1993.9729899 [ Links ]

Zerenler, M., Hasiloglu, S. B., & Sezgin, M. (2008). Intellectual capital and innovation performance: empirical evidence in the Turkish automotive supplier. Journal of Technology Management & Innovation, 3(4), 31-40. https://doi.org/10.4067/s0718-27242008000200003 [ Links ]

Received: September 22, 2016; Accepted: June 06, 2017

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons