Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Similars in

SciELO

Similars in

SciELO

Share

Permalink

PermalinkContaduría y administración

Print version ISSN 0186-1042

Contad. Adm n.230 Ciudad de México Jan./Apr. 2010

Artículos de investigación

Optimal portfolio and consumption decisions under exchange rate and interest rate risks. A jump–diffusion approach*

Decisiones de portafolio óptimo y consumo bajo riesgos de tipo de cambio y tasa de interés. Un enfoque de difusión con saltos

Francisco Venegas Martínez* y Abigail Rodríguez Nava**

* Profesor investigador, Escuela Superior de Economía, Instituto Politécnico Nacional. E– mail: fvenegas1111@yahoo.com.mx

** Profesora investigadora, Departamento de Producción Económica, Universidad Autónoma Metropolitana – Azcapotzalco. E–mail: arnava@correo.xoc.uam.mx

Fecha de recepción: 14.04.2009

Fecha de aceptación: 11.11.2009

Abstract

This research develops a stochastic model of the consumer's decision making under an environment of risk and uncertainty. In the proposed model agents perceive that a mixed diffusion–jump process drives the exchange rate depreciation and a diffusion process governs the real interest rate, these processes are supposed to be correlated. We generalize the proposals from Giuliano and Turnovsky (2003), Grinols and Turnovsky (1993) and Merton (1969 and 1971) by including sudden and unexpected jumps in the stochastic dynamics of relevant variables in the intended model. We examine portfolio, consumption and wealth equilibrium dynamics under the optimal decisions. We also assess the effects on portfolio, consumption and welfare of sudden and permanent changes in the parameters determining the expectations of the exchange rate depreciation.

Keywords: portfolio choice, intertemporal consumer choice, consumer behavior.

Resumen

Esta investigación desarrolla un modelo estocástico sobre las decisiones de los consumidores en un ambiente de riesgo e incertidumbre. En el modelo propuesto, los agentes perciben que la tasa de depreciación del tipo de cambio es conducida por un proceso de difusión con saltos y que la tasa de interés real es guiada por un proceso de difusión; se supone que estos procesos están correlacionados entre sí. Este trabajo generaliza las propuestas de Giuliano y Turnovsky (2003), Grinols y Turnovsky (1993) y Merton (1969 y 1971) a través de la inclusión de saltos repentinos e inesperados en la dinámica estocástica de las variables relevantes del modelo propuesto. Asimismo, se examina la dinámica de equilibrio del portafolio elegido, la demanda de consumo y la riqueza, en el equilibrio, asociados a las decisiones óptimas. Además, se evalúan los impactos que sobre el portafolio, el consumo y el bienestar tienen los cambios repentinos y permanentes en los parámetros que determinan las expectativas de la depreciación del tipo de cambio.

Palabras clave: selección de portafolio, selección intertemporal de consumo, conducta del consumidor.

Introduction

This paper develops a stochastic model of consumer's decision making in an environment of risk, emphasizing the role of uncertainty in the dynamics of both the depreciation rate and the real interest rate. It is assumed that 1) the exchange rate depreciation follows a mixed diffusion–jump process, and 2) the expected dynamics of the real interest rate is driven by a Brownian motion. These processes are supposed to be correlated; as stylized fact shows. This framework generalizes the proposals in Giuliano and Turnovsky (2003), Grinols and Turnovsky (1993), and Merton (1969) and (1971) by including sudden and unexpected jumps in the stochastic dynamics of relevant variables. By assuming logarithmic utility, we examine the equilibrium dynamics of portfolio, consumption and wealth in an environment of risk and uncertainty. We also study the effects on portfolio, consumption and economic welfare of once–and–for–all changes in the key parameters that determine the expected depreciation rate.

The financial literature has by now exhausted a class of deterministic models aimed at explaining the consumer's decision making under risk and uncertainty.

Most of the existing models ignore uncertainty, providing a very elaborate economic interpretation of why uncertainty does not need to be considered. Until fairly recently, no many attempts had been made to study consumers' portfolio decisions under exchange rate and interest rate risks; see for instance: Penati and Pennacchi (1989) and Svensson (1992).

The analytical framework is based on Venegas–Martínez (2001), (2005), (2006a), (2006b), (2006c), (2008) and (2009) and Merton (1969) y (1971). The proposed model, in which the exchange rate depreciation is driven by a mixed diffusion–jump process and the expected dynamics of the real exchange rate is modeled by a diffusion process (useful approximations to reality), is by itself capable of dealing with a range of interesting issues. Moreover, we analyze consumption and wealth equilibrium dynamics, and examine the effects on consumption and welfare of sudden changes in the expected depreciation of the exchange rate.

This research is organized as follows. In the next section, we work out a Ramsey–type, one–good, cash–in–advance, stochastic model where agents have expectations of devaluation driven by a mixed diffusion–jump process and the expected dynamics of the real interest rate is guided by a diffusion process. In section 3, we solve for the equilibrium dynamics, undertake the policy experiment, and examine the welfare implications. We also examine the dynamic behavior of portfolio, consumption and wealth, and address a number of exchange–rate policy issues. In section 4, we present conclusions, acknowledge limitations, and make suggestions for further research. Three appendices contain some technical details on the consumer's choice problem.

Structure of the economy

In order to derive solutions which are analytically tractable, the structure of the economy will be kept as simple as possible. Let us consider a small open stochastic economy with a representative infinitely lived investor in a world with a single perishable consumption good. The good is freely traded at a domestic price Pt, determined by the purchasing power parity condition, Pt = Pt*Et, where Pt* is the dollar price of the good in the rest of world, and Et is the nominal exchange rate. It will be assumed, from now on, that P* is fixed and for simplicity equal to 1, which readily implies that the price level, Pt, is equal to the exchange rate, Ef The initial value E0 is supposed to be known.

The ongoing uncertainty about the dynamics of the expected rate of depreciation is driven by a mixed diffusion–jump process. In such a case, we suppose that the representative investor perceives that the expected inflation rate, dPt /Pt, and thus the expected rate of depreciation, dEt /Et, is driven by a geometric Brownian motion with Poisson jumps:

where the drift ε is the mean expected rate of depreciation conditional on no jumps, σ is the instantaneous volatility of the expected rate of depreciation, v is the mean expected size of upward jumps in the exchange rate, and zt is a standard Wiener process, that is, dzt is a temporally independent normally distributed random variable with E[dzt ] = 0 and Var[dzt ]= dt. The number of devaluations per unit of time occurs according to a Poisson process qt with intensity λ , so

whereas

We initially set q0 = 0. Moreover, processes dzt and dqt are assumed to be correlated. Because of the specific interest of this paper in once–and–for–all changes in the rate of depreciation and in the intensity parameter, we assume that ε, σ, v and λ are all positive constants. Investors will hold two real assets: real cash balances, mt = Mt/Pt, where Mt is the nominal stock of money, and an international bond, bt. Thus, the investor's real wealth, Wt is defined by

where the initial wealth, W0 , is exogenously determined. Furthermore, we suppose that the rest of the world does not hold domestic currency (i.e., the peso is not an asset for foreigners). The stochastic dynamics of the real rate of return on bonds evolves in accordance with

where the drift, r0, is the mean rate of return, σ0 is the instantaneous volatility of the expected rate of return, and xt is a standard Wiener process; i.e., dxt is a temporally independent normally distributed random variable with E[dxt] = 0 and Var[dxt] = di. Moreover, we suppose that dzt and dxt are correlated

where Cov(dxt,dzt) is the covariance between dxt and dzt. We will assume that disturbances in the return rate and the exchange rate are positively correlated, that is, Cov(dxt ,dzt) > 0.

If capital is perfectly mobile, the real domestic interest rate, defined as (dRt /Rt) – (dEt /Et), must be equal to drt /rt over any instant. Consequently, the expected nominal interest rate is given by

where i = r0 + ε, is the mean expected nominal interest rate conditional on no jumps.

Consider now a Clower–type constraint of the form, mt > α ct, where ct is consumption and α > 0 is the time that money must be held to finance consumption. Given that i > 0, the investor has incentive to hold only

The stochastic rate of return of holding real cash balances, dRM, is simply the percentage change in the inverse of the price level. By applying the generalized Itô's lemma for diffusion–jump processes to the inverse of the price level with (1) as the underlying process (see Appendix III, formula (III.1), see also Lamberton and Lapeyre (1996)), we obtain:

Investor's Portfolio Problem

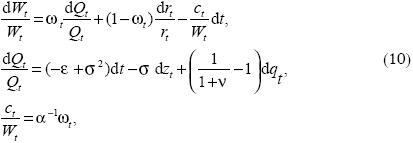

The stochastic investor's wealth accumulation in terms of the portfolio shares,  t = mt /Wt, and 1 – ωt = bt /Wt,

t = mt /Wt, and 1 – ωt = bt /Wt,

and consumption, ct (the numeraire good), is determined by the following system of stochastic differential equations:

where Qt = 1/Pt is the price of money in terms of goods. Observe that the portfolio optimal decision  , which is associated with monetary real balances, is, in virtue of the cash–in–advance constraint, linked with consumption. Of course, the optimal complementary proportion 1 – is intended for holding bonds. To avoid unnecessary technical complications, we exclude the investor real wage from the analysis. By solving system (10) in terms of dWt /Wt, we get

, which is associated with monetary real balances, is, in virtue of the cash–in–advance constraint, linked with consumption. Of course, the optimal complementary proportion 1 – is intended for holding bonds. To avoid unnecessary technical complications, we exclude the investor real wage from the analysis. By solving system (10) in terms of dWt /Wt, we get

where ρ depends only on exogenous parameters. Our analysis will be only concerned with small values of the total volatility compared with the mean expected rate of depreciation in such a way that

The competitive, risk–averse investor derives utility from consumption, ct, and wishes to maximize her/his overall discounted, Von Neumann–Morgenstern utility, at time t = 0, given by

where F0 is all available information at t = 0. In order to generate closed–form solutions, we have chosen the logarithmic utility function.

Comparative Statics

In maximizing (13) subject to the wealth constraint as given in (11), the first–order condition for an interior solution is (see Appendix I)

where A and B depend on parameters and on Cov(dxt,dzt) > 0. We have not imposed any positivity constraint of the form ![]() t > 0 , so unrestricted short sales are permitted. In what follows, without loss of generality, we will suppose that Cov(dxt,dzt) is bounded from above so that

t > 0 , so unrestricted short sales are permitted. In what follows, without loss of generality, we will suppose that Cov(dxt,dzt) is bounded from above so that

From (15), we immediately find that A > 0. Observe that (14) is a cubic equation with one negative and two positive roots, and only one root satisfying 0< ω *<1.

We have now the first important results: a once–and–for–all increase in the rate of depreciation, which results in an increase in the future opportunity cost of purchasing goods, leads to a permanent decrease in the proportion of wealth devoted to future consumption. It is enough to differentiate (14) to obtain

Another relevant result is the response of the equilibrium share of real monetary balances, ω *, to once–and–for–all changes in the intensity parameter, λ. A once–and–for–all increase in the expected number of devaluations per unit of time causes an increase in the future opportunity cost of purchasing goods. This, in turn, permanently decreases the proportion of wealth set aside for future consumption. By differentiating (14), we get

Thus, the elasticity of the depreciation rate satisfies:

In other words, portfolio shares are more responsive to changes in the mean expected depreciation rate than to changes in the expected number of devaluations.

Welfare implications

We assess now the magnitudes of the impacts on welfare of once–and–for–all changes in the mean expected rate of depreciation and in the probability of devaluation. As usual, the welfare criterion, W, of the representative investor is the maximized utility starting from the initial real wealth, W0. Therefore, economic welfare is given by (see Appendix I, formula (I.3))

A routine exercise of comparative statics leads to:

and

As it might be expected, welfare behaves as a decreasing function of both the mean expected rate of depreciation.

Money in utility index

The cash–in–advance assumption is somewhat restrictive in the sense that money is only seen as medium of exchange. We ease this assumption by including currency directly in the utility function because of its liquidity services. In such a case, the stochastic wealth accumulation in terms of the portfolio shares and consumption becomes

where  depends on exogenous parameters. The expected utility at time t = 0, V0, now takes the form:

depends on exogenous parameters. The expected utility at time t = 0, V0, now takes the form:

We have chosen again the logarithmic utility function to generate closed–form solutions.

The first order conditions for an interior solution to the problem of maximizing

where D and B are taken as in section 2. The second equation above is similar to

that of (14), except for the factor 1/(1 + θ) ) that now appears in the first term of the left–hand side of (22).

Concluding remarks

We have presented a stochastic model of exchange rate and interest rate risks. Specifically, it was assumed that agents have expectations of the exchange rate depreciation driven by a mixed diffusion–jump process and a diffusion process guides the real interest rate. By using a logarithmic utility, we have derived explicit solutions and examined the dynamic implications of uncertainty. Our analytical framework, in which the expectations of devaluation are driven by a combination of Brownian motion with a Poisson process and the real interest rate is guided by a Brownian motion, provides new elements to understand the consumer behavior.

Several of the obtained results throughout this research deserve further attention and discussion. For example, it is observed from Equation (9) that the returns of real money balances for low levels of volatility in prices may lead to a negative trend due to inflation. Nonetheless, this trend can be reversed for higher levels of volatility, since fluctuations in prices, although large, can be upward (inflation) or down (deflation); and in the last case the trend can be positively modified. With respect to equation (10), after replacing the optimal proportion of wealth allocated for holding real balances (which, on the basis of equation (14), is maintained constant by the agent to manage future uncertainty), it is concluded that consumption should be always proportional to wealth. When the level of volatility remains constant, the above result is similar to that found in Modigliani (1971) in the following sense: a risk–averse agent (with logarithmic utility) to deal with future uncertainty should continue the strategy of maintaining its consumption proportional to his/her wealth. On the other hand, if a consumer–investor makes decisions on portfolio and consumption in a deterministic environment and has access to both bonds (free of default risk) and real balances, then the agent can determine his/her optimal consumption path. Whereas in the stochastic case, the consumption path cannot be determined because consumption becomes a random variable; a situation closer to reality. Finally, we have that an increase in the probability of a jump in the exchange rate and a rise in the average expected rate of depreciation may lead to a reduction in the economic welfare of the agents, that is, their levels of satisfaction will be lessened; the same arguments and considerations apply when money is included in the utility function (according to equation (22)).

It is worthwhile mentioning that the results obtained strongly depend on the assumption of logarithmic utility, which is a limit case of the family of constant relative risk aversion utility function. The extension of our stochastic analysis to such a family does not provide closed–form solutions, and result might be only obtained via numerical methods. More work is needed in the above aspect.

Finally, we believe that more research should be undertaken in this stochastic framework to include government transfers and a stochastic budget constraint for the government (in a full general equilibrium), and to extend the analysis to include both non–tradable and durable goods. Needless to say, further work is required in this regard.

References

Giuliano, P., and S. J. Turnovsky (2003). Intertemporal substitution, risk aversion, and economic performance in a stochastically growing open economy. Journal of International Money and Finance, Vol.22, No. 4, pp. 529–556. [ Links ]

Grinols, E. A. and S. J. Turnovsky (1993). Risk, the financial market, and ma–croeconomic equilibrium. Journal of Economic Dynamics and Control, Vol. 17, No. 1–2, pp. 1–36. [ Links ]

Lamberton, D. and B. Lapeyre (1996). Introduction to Stochastic Calculus Applied to Finance. Chapman & Hall. [ Links ]

Merton, R. C. (1969). "Lifetime Portfolio Selection under Uncertainty: The Continuous–Time Case". Review of Economics and Statistics, Vol. 51, No. 3, pp. 247–257. [ Links ]

––––––––––(1971), Optimum Consumption and Portfolio Rules in a Continuous–Time Model, Journal of Economic Theory, Vol. 3, No. 4, pp. 373–413. [ Links ]

Modigliani, F. (1971), "Monetary Policy and Consumption", in Consumer Spending and Monetary Policy: the linkages, Federal Reserve Bank of Boston, Conference Series No. 5, pp. 9–84. [ Links ]

Penati, A. and G. Pennacchi (1989). "Optimal Portfolio Choice and the Collapse of a Fixed–Exchange Rate Regime". Journal of International Economics, Vol. 27, No. 1–2, pp. 1–24. [ Links ]

Svensson, L. E. O. (1992). The Foreign Exchange Risk Premium in a Target Zone with Devaluation Risk. Journal of International Economics, Vol. 33, No. 1–2, pp. 21–40. [ Links ]

Venegas–Martínez, F. (2001). "Temporary Stabilization: A Stochastic Analysis". Journal of Economics Dynamics and Control, Vol. 25, No. 9, pp. 1429–1449. [ Links ]

––––––––––(2005). "Bayesian Inference, Prior Information on Volatility, and Option Pricing: A Maximum Entropy Approach". International Journal of Theoretical and Applied Finance, Vol. 8, No.1, pp.1–12. [ Links ]

––––––––––(2006a). "Stochastic Temporary Stabilization: Undiversifiable Devaluationand Income Risks". Economic Modelling, Vol. 23, No. 1, pp. 157–173. [ Links ]

––––––––––(2006b). "Fiscal Policy in a Stochastic Temporary Stabilization Model: Undiversifiable Devaluation Risk". Journal of World Economic Review, Vol. 1. No. 1, pp. 87–106. [ Links ]

––––––––––(2006c). Riesgos financieros y económicos (productos derivados y decisiones económicas bajo incertidumbre, International Thomson Editors. [ Links ]

––––––––––(2008). Riesgos financieros y económicos (productos derivados y decisiones económicas bajo incertidumbre, 2a. edición. Cengage Learning (anteriormente International Thomson Editors). [ Links ]

––––––––––(2009). "Temporary Stabilization in Developing Countries and the Real Option of Waiting, when Consumption Can Be Delayed". International Journal of Economic Research, Vol. 6, No. 2, 229–249. [ Links ]

* The authors are very gratefully for many valuable comments and suggestions made for two anonymous referees.