Services on Demand

Journal

Article

text in

text in  English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

-

Cited by SciELO

Cited by SciELO -

Access statistics

Access statistics

Related links

-

Similars in

SciELO

Similars in

SciELO

Share

Permalink

PermalinkContaduría y administración

Print version ISSN 0186-1042

Contad. Adm vol.67 n.3 Ciudad de México Jul./Sep. 2022 Epub June 06, 2023

https://doi.org/10.22201/fca.24488410e.2022.3324

Articles

Unconventional monetary policy of the ECB and unemployment

1 Universidad Nacional Autónoma de México, México

In this paper both the main characteristics of the European Central Bank's (ECB) unconventional monetary policy and its effectiveness on the labour market between 2008-2019 are dealt with. Our econometric analysis is based on a panel vector autoregression (PVAR) methodology; it is empirically shown that policy rate changes and policy innovations such as forward guidance strategies turn out to be effective over the first twelve months. However, the empirical evidence appears to suggest that the effectiveness of the ECB’s balance sheet policy with regards reducing the unemployment rate is not as strong. Our results reveal that unconventional monetary policies have contributed to a gradual, albeit slow, recovery of both economic activity and the labor force’s employment level.

JEL Code: E24; E52; E58

Keywords: unconventional monetary policy; ECB; unemployment; PVAR

El presente trabajo analiza las principales características de la política monetaria no convencional del banco central europeo (BCE) y su efectividad sobre el desempleo entre 2008-2019. En nuestro análisis empírico utilizamos una metodología PVAR; encontramos efectividad atribuible a cambios en la tasa de interés de la política monetaria y a los anuncios de política con estrategias forward guidance durante los primeros 12 meses. Asimismo, identificamos una escasa certeza en la reducción del desempleo mediante el uso de la hoja de balance del BCE. Los resultados sugieren que las medidas de política no convencionales han contribuido en la gradual, aunque lenta, recuperación económica y en la reducción de la tasa de desempleo.

Código JEL: E24; E52; E58

Palabras clave: política monetaria no convencional; BCE; desempleo; PVAR

Introduction

The Great Recession (GR) led to large fluctuations in production and employment levels in the eurozone. According to figures from the European Statistical Office (Eurostat), the unemployment rate across the region went from 7.6% in 2008 to 12% in 2013. Spain and Greece were the hardest hit, with rates of 26.1% and 27.5%, respectively. Therefore, the aftermath of the financial crisis conditioned economic policy in terms of objectives and instruments.

During the post-GR years, several economies-including the eurozone-adopted a nonconventional monetary policy (NCMP) to stabilize the economy. This represented a departure from the inflation targeting regime (IT) of the 1990s, which posits that the objective of low and stable inflation is achieved through the interest rate. In the process, the central bank brings output and unemployment closer to their potential levels and long-term trends (Bernanke & Mishkin, 1997). Hence the relevance of analyzing the modus operandi and the results obtained by the European Central Bank (ECB) in applying it as a short-term stabilizer.

This study argues that the NCMP adopted by the ECB between 2009-2019 operated based on proprietary instruments and transmission mechanisms-vis à vis the IT-whose impact on reducing the unemployment rate was limited in the short run, requiring a greater prolongation in its application. Likewise, this study aims to demonstrate dynamically that when the policy rate is at the zero lower bound, not all central bank instruments are optimal for stabilizing employment. The estimation of a PVAR model indicates that forward guidance signaling reinforces the effect of tight policy rate cuts and that the specific use of balance sheets and extraordinary liquidity targeting dysfunctional segments of the financial market has little impact on the unemployment rate. The results test the hypothesis.

In addition to this introduction, the first section studies the theoretical aspects of the NCMP adopted by the ECB. It then presents some stylized facts based on the main variables of interest. Subsequently, it estimates a PVAR model for a sample of 8 euro area countries to identify the effectiveness of unconventional measures on the unemployment rate. Finally, it discusses the findings derived from the econometric exercise.

Theoretical and empirical aspects of NCMP in the eurozone

Theoretical review

In 2003, the ECB adopted the IT, a monetary scheme that postulates that low and stable inflation optimizes economic growth and employment (Bernanke & Mishkin, 1997). The main refinancing operations rate (MRO) and the two standing facility rates, credit and deposit, were the instruments used by this monetary authority until 2008 when the GR weakened the fundamentals of the economy in the region. In 2009, the theoretical problem of the interest rate at the zero lower bound was the most significant operational difficulty for several central banks, leading to an alternative monetary policy.

The NCMP, so called to distinguish it from the pre-crisis one of 2008, emerged as a way of maintaining the transmission mechanism of the monetary rule in economic activity, prices, and financial stability (Giannone et al., 2011). While not entirely innovative in some instruments, the combination of measures, an unprecedented operational scale, and the purposes pursued placed the monetary authority in an unconventional position vis-à-vis private agents (Potter & Smets, 2009). In this context, the ECB adopted this alternative monetary framework with four instruments, namely:

The balance sheet of the central bank, through asset purchases, has the potential to lower short and long-term interest rates; restore expectations and the behavior of stock prices in the financial market (Bernanke, 2012); and, subsequently, foster conditions for an increase in output and employment with a consequent decrease in deflationary risks.

Monetary policy signaling with forward guidance operates through the interest rate and inflation expectations channel. The central bank contributes to the forward-looking formulation of agents by stating its forward guidance1 and reducing uncertainty. The strategy is most efficient when statements are conditional on macroeconomic outcomes with long periods and are accompanied by asset purchase programs (Coenen et al., 2017).

The negative nominal interest rate was a monetary policy innovation that posits the existence of a cost for holding reserves with the central bank. It is considered to function analogously to an unrestricted zero lower bound. Its effects run through the credit channel that causes the re-composition of the balance sheet of companies by choosing to hold assets instead of deposits and by demanding the credit offered by banking institutions (Altavilla et al., 2019), subsequently affecting aggregate demand and output.

Extraordinary liquidity measures aim to provide counterparties to the banking system. Their unconventional nature lies in the characteristics of the interventions: the greater the number of operations, amounts, and terms, the lower the costs, the wider the range of collateral and the operations conditioned on the granting of non-bank loans. Its effects flow through the interest rate channel.

According to Bernanke (2017), the NCMP affects the asset yield curve generated by purchasing bonds. It has a broad influence on the agents' expectations, so communication takes on an even more important role, and it impacts longer-term interest rates. The introduction of unconventional measures was gradual and in response to economic developments in the eurozone (see Table 1). Initially, those concerning extraordinary liquidity with long-term refinancing operations (LTRO), accompanied by the first covered bond purchase program (CBPP) in May 2009, stand out. Subsequent problems in the government bond market segments in Greece, Spain, Italy, Ireland, and Portugal led to the government bond purchase program (SMP) in 2010.

Table 1 Unconventional monetary policy of the ECB, 2008-2019

| Date | Non-Conventional Monetary Policy Instruments | |||

|---|---|---|---|---|

| Negative interest rate on the deposit facility | Use of the balance sheet | Forward guidance | Liquidity | |

| 27/03/2008 | LTRO Introduction of six-month refinancing transactions | |||

| 08/10/2008 | Commencement of operations at the established rate and full allotment | |||

| 15/10/2008 | Announcement of operations with a maintenance period | |||

| 07/05/2009 | CBPP collateralized bond purchase program | LTRO three one-year refinancing operations announced | ||

| 10/05/2010 | SMP public debt purchase program | |||

| 04/08/2011 | LTRO announcement of a 6-month refinancing transaction | |||

| 06/10/2011 | CBPP 2-second bond purchase program | LTRO two one-year refinancing operations announced | ||

| 08/12/2011 | VLTRO announcement of two 3-year refinancing transactions | |||

| 18/01/2012 | Decrease in the reserve requirement ratio from 2% to 1% | |||

| 02/08/2012 | OTM unlimited public debt purchase program | |||

| 04/07/2013 | "The Governing Council expects key ECB interest rates to remain at current levels or lower over an extended period." | |||

| 05/06/2014 | -0.10% | TLTRO I Longer-term refinancing operations with a specific purpose | ||

| 04/09/2014 | S.C. | CBPP 3 Third bond purchase program ABSPP Asset-backed securities purchase program | ||

| 02/10/2014 | -0.20% | |||

| 22/01/2015 | S.C. | PSPP Purchase program for bonds issued by European governments, agencies, and institutions APP Extension of the asset purchase program, includes CBPP3 ABSPP, and PSPP | ||

| 03/12/2015 | -0.30% | |||

| 10/03/2016 | -0.40% | CSPP Corporate Asset Purchase Program (part of the APP) | Linking the future interest rate path to the purchase programs: "until well beyond the horizon of our net purchases." | TLTRO II Second series of longer-term refinancing operations for specific purposes |

| 13/12/2018 | S.C. | Completion of the APP | Maintenance of rates: "until at least summer 2019." | |

| 24/01/2019 | S.C. | On interest rates: "We expect them to remain at their current levels through at least summer 2019, and in any case for as long as necessary." In asset purchases: "we expect to continue to fully reinvest the principal of securities purchased under the maturing asset purchase program for an extended period after the date on which we begin to raise key ECB interest rates and, in any event, for as long as necessary to maintain favorable liquidity conditions and a large degree of monetary accommodation." | ||

| 07/03/2019 | S.C. | TLTRO III Third series of longer-term refinancing operations for specific purposes | ||

| 12/09/2019 | -0.50% | Announcement of the restart of the APP as of November 2019 | On interest rates: "We now expect ECB policy rates to continue at current or lower levels until we see a solid convergence of the inflation outlook." | introduction of the two-tranche system for reserve remuneration exempting one tranche from the negative rate |

| 24/10/2019 | S.C. | |||

| 12/12/2019 | S.C. | Regarding APP purchases: "We expect them to continue for as long as necessary to reinforce the accommodating impact of our policy rates and to shortly end before we begin to raise the key ECB interest rates." | ||

Source: created by the author based on ECB. Press Conferences. Available at: https://www.ecb.europa.eu/press/pressconf/html/index.en.html

In July 2013, forward guidance signaling-which included interest rates-was adopted for the first time, explicitly linked to the purchase programs since 2016. From 2014 onwards, the deposit facility rate was set at -0.10%, i.e., it crossed the zero lower bound and continued to decline until it reached -0.5% in September 2019. Since the second half of 2014, the ECB has been using all four unconventional instruments simultaneously as a monetary policy strategy.

The NCMP enabled the transmission mechanism to function adequately in stressed financial markets (Millaruelo & Del Río, 2013). The measures dissipated extreme risks of financial instability and deflationary pressures to restore the functioning of certain financial markets and support the economy's recovery (Berganza et al., 2014). However, during the first years after 2008, there was an expectation of normalization of monetary policy as the main risks dissipated; the macroeconomic performance and the succession of measures that reinforced the unconventional role demonstrated the difficulty of returning to the conventional framework.

Review of empirical studies

Some theoretical and empirical studies analyze the NCMP. Lenza et al. (2010) identify that the three transmission channels, namely very short-term interest rate, interest rate differentials, and expectations, affect the yield curve and long-term interest rates. Farmer and Zabczyk (2016) build a general equilibrium model with rational expectations to test whether changing the risk composition of the central bank's balance sheet controls asset price volatility and stabilizes output and employment.

Beyer et al. (2017) describe the favorable macroeconomic effects of asset purchases and liquidity provision facilities. The evidence indicates that these programs effectively reduced interest rates by improving liquidity in dysfunctional segments, while the latter mitigated private funding constraints. On the other hand, forward guidance signaling helped alleviate zero lower bound constraints. The authors also indicate that the implications of negative interest rates on financial and economic stability require further study.

Regarding the NCMP conducted by the US Federal Reserve, Cùrdia and Woodford (2011) analyze the balance sheet’s effectiveness. With the extension of the New-Keynesian model and estimation of impulse-response functions, the authors examine various unconventional scenarios vis à vis the standard interest rate and conclude that the increase in assets held by the central bank is irrelevant for macroeconomic equilibrium when financial markets perform well. However, in the face of financial instability, credit policy is effective, including for the population's welfare, if the financial authority acts efficiently.

Dell'Ariccia et al. (2018) investigate the impacts of negative interest rates, forward guidance, and quantitative easing in the euro area, the United Kingdom, and Japan. Their argument states that the expansion of the balance sheet of these central banks promotes the proper functioning of the financial system, economic activity, and price stability. They test their hypothesis for the specific case of the European region.

Hachula et al. (2020) study the macroeconomic effects of NCMP in the eurozone using structural autoregressive vectors. Their results indicate that monetary expansions increase prices, consumption, and output and decrease regional unemployment. They also find that public and private interest rates, asset prices, and credit volume are the most important transmission mechanisms. However, primary spending increases significantly, which limits the degrees of freedom of fiscal policy.

Regarding methodology, Boeckx, Dossche, and Peersman (2014) estimate a structural vector autoregressive regression (SVAR) model to find that an expansion of the ECB balance sheet favorably affects output and inflation. However, the magnitude of this relationship is smaller in countries with problems in their banking systems that prevent more credit from reaching households and companies. In the same vein, the multi-country estimation with global vector autoregressive (GVAR) models by Burriel and Galesi (2016) reinforces the evidence of the stabilizing role of economic activity and the price level, albeit with local heterogeneity. Gambacorta, Hofmann, and Peersman (2014) identify with a panel SVAR that the increase in the balance sheet generates a temporary rise in income similar to that expected with IT. However, the impact on prices is low and of little persistence over time.

Gambetti and Musso (2017) perform a variable parameter VAR model with counterfactual scenarios to show the direct impact on GDP and inflation through the asset purchase program. Elbourne, Ji, and Duijndam (2018) argue that both effects-on output and prices-for the set of euro-area countries are economically insignificant due to their size. Despite this, the close link with the functioning of monetary policy transmission channels is apparent at the country level. On employment, the study by Laine (2020), with the help of factor-augmented vector autoregressive (FVAR) models, finds a weak response of the unemployment rate to changes in the policy rate between 2007-2017.

However, most of the literature has favored a time-oriented analysis of the first years after 2008 or one focused on specific programs, which generates a partial picture that requires more empirical evidence on the comprehensive results and implications of a continuous and prolonged NCMP for more than a decade.

Stylized facts

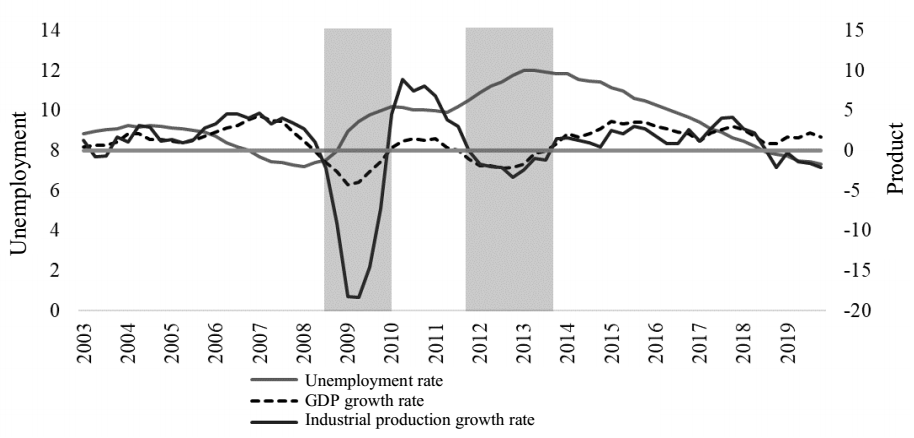

Before the GR, eurozone output experienced moderate growth accompanied by a decline in the unemployment rate (see Figure 1). After the deterioration of financial markets, both variables fell sharply. Despite the brief recovery in income between 2010-2011, unemployment did not return to its previous level. It continued to rise due to the worsening sovereign debt between 2011 and 2013. In the face of the damage suffered by the labor market, the improvement in employment figures since 2014 was encouraging but not an extraordinary phenomenon. Figure 1 also makes it possible to appreciate the close empirical link between the two real variables that economic theory formulates as Okun's Law (Okun, 1962). Given this relationship, it is crucial to address the effectiveness of the monetary policy on the unemployment rate.

Source: created by the author with data from Eurostat and ECB; Statistical Data Warehouse

Note: Year-on-year growth rates; industrial production uses the industrial production index (2015=100)

Figure 1 Output and unemployment; euro area, 2003-2019

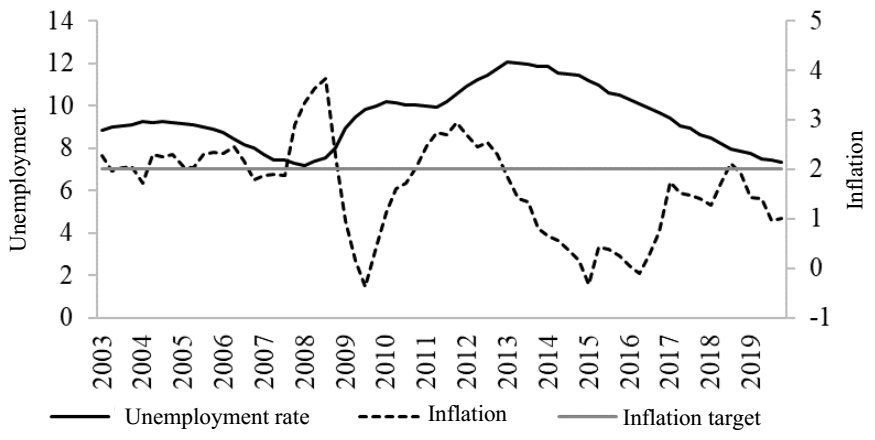

Figure 2 shows how the low inflation rate after the 2008 crisis was associated with higher unemployment rates. Given this situation, the problem was not limited to achieving the satisfactory operation of the financial markets. The monetary authority sought to remove obstacles in the transmission of policy so that its measures would reach the real sector of economic activity. However, since 2013, it has been difficult to stabilize the economy at output and unemployment levels in line with the quantitative target of the ECB. Deflationary risks were latent even in 2019 despite improving labor markets and positive GDP growth since 2014.

Source: created by the author with data from the ECB; Statistical Data Warehouse

Figure 2 Unemployment and inflation; eurozone, 2003-2019

With the crisis, the immediate focus of monetary policy was the financial market, where liquidity and credit contracted, and the systemic risk of potential damage to the real economy grew. The ECB, in addition to granting liquidity through rate cuts and refinancing operations, henceforth assumed an unconventional stance through its asset purchase programs, which made it possible to attend to dysfunctional segments with greater precision and prioritized that the transmission mechanism should not be hindered in its transit through the financial market.

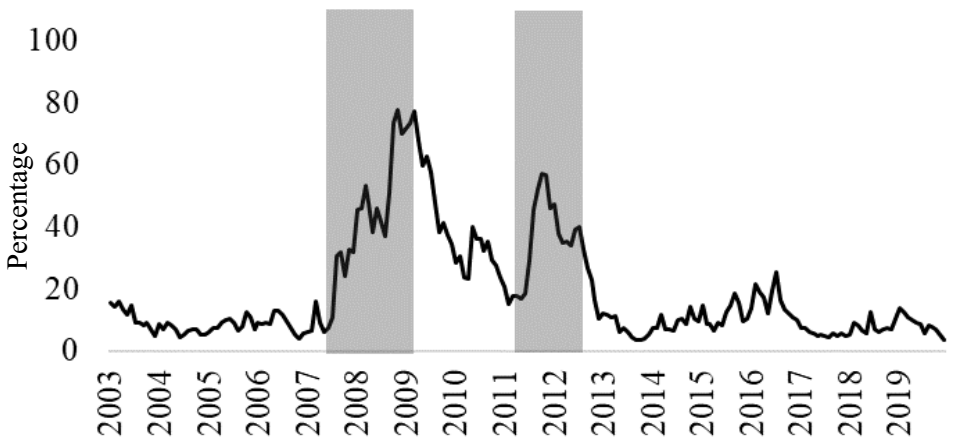

Through the composite indicator of systemic stress (CISS)2 presented in Figure 3, this study identifies the rise in systemic risk since months before the collapse of September 2008 and the subsequent tensions in sovereign debt segments that threatened the stability of the euro between 2011-2012. It is also possible to appreciate the moments of stability brought about by using the NCMP instruments, such as the decline in the index since mid-2009 with the first CBPP and the announcement of the OTM in August 2012.

Source: created by the author with ECB data; Statistical Data Warehouse

Figure 3 Composite indicator of systemic stress CISS; eurozone, 2003-2019

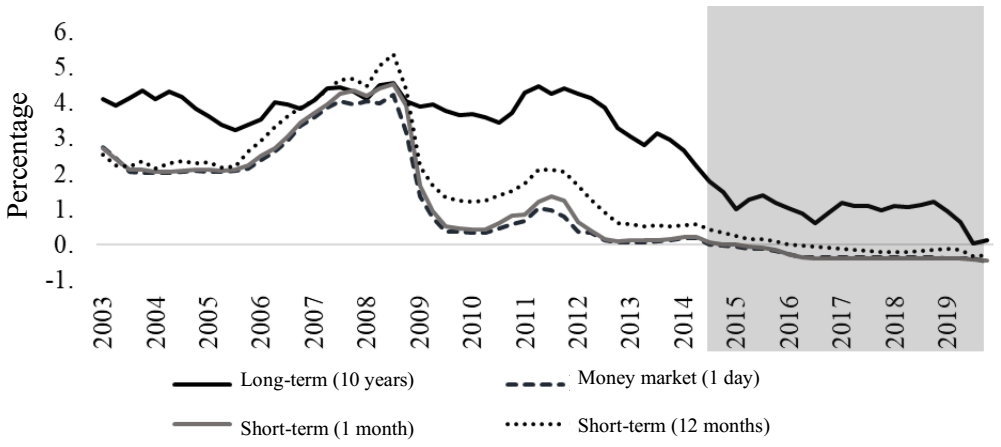

Figure 4 shows the representative interest rates for different terms, where it is possible to see that between 2003-2008 the short-term rates followed convergent trends. With the financial crisis, these rates were close to zero, and a considerable differential began to emerge concerning long-term rates. Since 2012, deflationary risks have led to the second round of adjustments. Thus, as the NCMP widened its scope, the narrowing of the term spread was identifiable in practice. In 2019, 10-year bond yields were practically at zero.

Source: created by the author with Eurostat data

Note: the shaded part corresponds to the period with negative interest rates in the money market

Figure 4 Representative nominal interest rates: euro area, 2003-2019

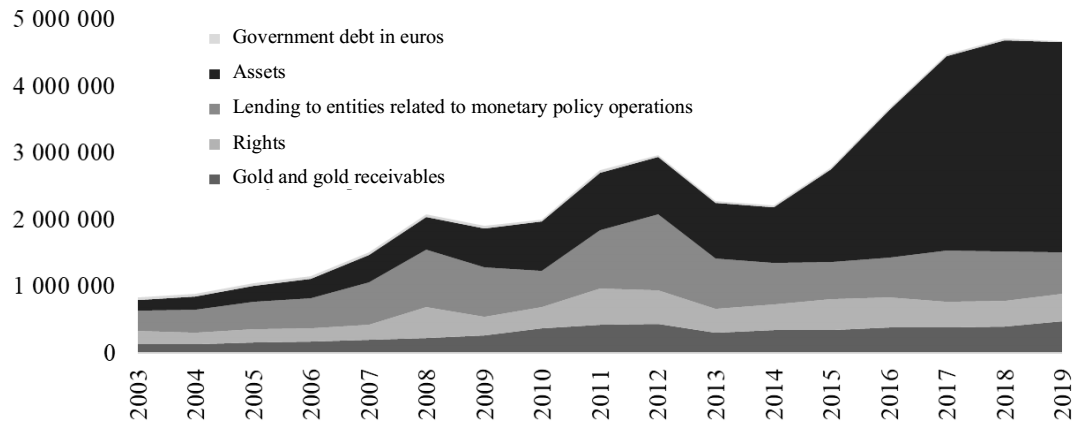

The ECB balance sheet shown in Figure 5 was characterized by an expansion of assets with no changes in its total composition between 2008-2012. Starting in 2014, the increase in assets held for monetary policy purposes and subsequent purchase programs affected the whole structure. The expansion in the range of assets included securities market programs (SMP), the three covered bond purchase programs (CBPP), the corresponding one for corporate assets (CSPP), asset-backed securities purchases (ABSPP), and the purchase of bonds issued by governments, agencies, and European institutions (PSPP). The second component that explains the growth of the balance sheet is loans to entities for monetary policy purposes. This category includes the main refinancing (MRO), long-term (LTRO), and targeted (TLTRO) operations, instruments through which the liquidity required by financial institutions was introduced.

Source: created by the author with data from the ECB; available at https://www.ecb.europa.eu/pub/annual/balance/html/index.en.html

Figure 5 ECB balance sheet, 2003-2019; assets in millions of euros

Empirical analysis

Data

The ad hoc methodology for our study consists of the panel vector autoregressive model (PVAR) with both endogenous and exogenous variables. The measurement of this study made it possible to capture and control the heterogeneity or panel effect for a group of countries, having the advantage of not requiring too many assumptions about the structure of the model (Holtz-Eakin et al., 1988). The generalized method of moments (GMM) estimation was performed with estimators from Arellano and Bover (1995).

The sample that integrates the long-type panel consists of eight euro area countries divided according to their unemployment rate: Germany, the Netherlands, Belgium, and Austria represent low rates, and France, Italy, Spain, and Greece represent high rates. In addition to the heterogeneity in unemployment figures, the sample includes the leading economies of the area by GDP size. The data are monthly and cover the period of 2003:01- 2019:12.

Based on the empirical literature reviewed, this study proposes the seasonally adjusted unemployment rate3, the harmonized consumer price index (CPI) 2015=100, and the seasonally adjusted gross domestic product (GDP) in real values 2015=100 as endogenous variables4. It includes the composite indicator of financial stress (CISS) for Austria, Belgium, Germany, the Netherlands, France, Italy, and Spain, and the composite indicator of sovereign stress (CISSov), in the case of Greece, as the financial market performance variable.

The deposit facility rate is included as an exogenous and invariant variable between countries and makes it possible to capture conventional and non-conventional movements linked to negative nominal values. The movements of this instrument conceptually operate through the interest and credit channel. The balance sheet total of the ECB captures the magnitude of asset purchases, with effects flowing through the asset price, portfolio rebalancing, and expectations channels. While the balance sheet may contain an endogenous component due to the forward-looking process of monetary policy implementation, this study assumes it to be exogenous. Finally, it includes a dichotomous variable that captures the announcement dates of forward guidance monetary policy decisions that the study considers to act through the expectations channel.

Data were obtained from Eurostat and ECB Statical Data Warehouse. In the case of the ECB balance sheet and CISS, the series were seasonally adjusted with Census X12. Subsequently, CPI and balance sheet Napierian logarithms were applied for GDP. The policy and unemployment rates are in percentages, while the CISS variable is in an index. The study worked with stationary variables for the first differences, except for the policy rate, given its low variability in a large part of the sample5 and the forward guidance indicator. The Im-Pesaran-Shin unit root test for panel data confirms the presence of post-differencing stationarity (see Table 2). The panel obtained is balanced and satisfies the Kao and Pedroni panel cointegration tests (see Tables A1 and A2 of the statistical Annex).

Table 2 Im-Pesaran-Shin unit root test, 2003:01-2019:12

| Augmented Dickey-Fuller Regression | ||||||||

|---|---|---|---|---|---|---|---|---|

| Variable | Z-t-tilde-bar | 1% | 5% | 10% | Panels | Periods | Panel means | Time Tend |

| du | -17.441 *** | -2.75 | -2.58 | -2.49 | 8 | 203 | including | including |

| y | -35.979 *** | -2.75 | -2.58 | -2.49 | 8 | 203 | including | including |

| p | -27.909 *** | -2.75 | -2.58 | -2.49 | 8 | 203 | including | including |

| dciss | -27.271 *** | -2.75 | -2.58 | -2.49 | 8 | 203 | including | including |

| balance | -27.647 *** | -2.75 | -2.58 | -2.49 | 8 | 203 | including | including |

Ho: all panels contain a unit root

Note: all variables are in first differences; p-val; *** p<0.01, ** p<0.05, * p<0.1

Source: created by the author

Model

The estimated model includes the sets of endogenous variables Yit and exogenous variables Xt (see Equation 1); where Uit is the unemployment rate, GDPit is the gross domestic product, IPCit is the consumer price index, CISSit is the composite indicator of systemic stress, MPRt is the nominal interest rate for the deposit facility, Bt is the total value of balance sheet assets, and FWt corresponds to the dichotomous indicator variable of forward guidance monetary policy announcements. Since the ECB determines the exogenous variables, they are invariant across countries.

A p-order vector autoregressive panel model is defined as shown in Equation 2:

Where i = {1,2,3, . .. , 8} corresponds to the observations of each country at time t = {1,2,3,… ,203}, Yit represents the vector of previously defined endogenous variables, Xt is the vector of exogenous variables, ai are the individual effects of the panel specification, eit is the idiosyncratic error, and A1…Ap,B are the parameter matrices to be estimated. The idiosyncratic error represents innovations and is assumed to have three properties, E(eit) = 0, E(eiteis) = 0 ∀ t ≠ s, and E(eiteit) = ∑ = variance − covariance matrix.

Three estimations were performed with the long and balanced panel, corresponding to the whole time data (2003:01-2019:12) with 1,592 observations and the subperiods of CMP (2003:01-2008:08) with 512 observations and NCMP (2008:09-2019:12) with 1,080 observations. These last two estimates will make it possible to identify differences in the effects on endogenous variables in different policy outlines.

The PVAR estimates (see Tables A3-A6 in the statistical annex) follow the optimal order of moments criterion (MMSC) of Andrews and Lu (2001) based on the J-statistic, which aims to specify the autoregressive order and valid instruments. After evaluating different order alternatives and instrument sets, this study proposes the appropriate AR specifications for each estimate and lags 5 to 20 as instruments. The PVAR estimates satisfy the stability condition and the over-identification test. Subsequently, dynamic multipliers were obtained over a 12-month time period. The study refers to the cumulative effects of changes in monetary policy variables as the sum of the multipliers after 1, 6, and 12 months.

According to Lütkepohl (2005), for the calculation of the dynamic multipliers, it is necessary to rewrite Equation (2) in its reduced form using lag operators to determine Equation (3):

Where D corresponds to the matrix of dynamic multipliers for the exogenous variables, the components A(L)−1eit are the endogenous innovations, and bi is the panel effect.

Results

Estimation without distinction of the type of monetary policy

Based on the estimation of the dynamic multipliers of the monetary policy variables on the unemployment rate, output growth, the CISS indicator, and the inflation rate (see Table 3), the study identified a 12month cumulative effect of 0.054% in the unemployment rate in response to a one percentage point change in the policy rate; the effect is as indicated by macroeconomic theory. Output reacts inversely to 1% increases in the policy rate, decreasing by -0.058% in the first six months, diluting the effect.

Table 3 Dynamic Multipliers, 2003:01-2019:12

| 1 month | 6 months | 12 months | |

|---|---|---|---|

| Unemployment rate | |||

| ECB Balance | 0.000 | -0.014 | -0.009 |

| Policy rate | 0.014 | 0.033 | 0.054 |

| Forward guidance | -0.014 | -0.027 | -0.028 |

| Production | |||

| ECB Balance | 0.010 | 0.000 | 0.009 |

| Policy rate | -0.003 | -0.058 | 0.033 |

| Forward guidance | 0.090 | 0.019 | -0.092 |

| CISS | |||

| ECB Balance | 0.425 | 0.449 | 0.475 |

| Policy rate | 0.394 | 0.364 | 0.261 |

| Forward guidance | 0.860 | 0.512 | 0.583 |

| Inflation | |||

| ECB Balance | 0.002 | 0.003 | 0.004 |

| Policy rate | 0.008 | -0.005 | -0.012 |

| Forward guidance | -0.143 | -0.131 | -0.133 |

Notes: correspond to cumulative multipliers for periods of 1, 6, and 12 months Source: calculations by the author

Percentage unit changes in the ECB balance sheet show little cumulative 12-month effect on the unemployment rate -0.009% and output of 0.009%. Additionally, a fall in the inflation rate of -0.012% was identified with a 1% increase in the policy rate and a reduction of -0.133% with forward guidance announcements after 12 months. Balance sheet growth contributes little to higher inflation. The estimate indicates a 0.39% drop in CISS financial stress with a 1% decrease in the monetary policy variable during the first month and 0.26% after 12 months; however, the indicator does not decrease with increases in balance sheet size or forward guidance.

Estimation with sub-periods corresponding to the monetary policy rate

Distinguishing by sub-periods (see Table 4) with CMP, a 1% increase in the policy rate exerts a cumulative 12-month effect of -0.013% on the unemployment rate and -0.003% with a 1% increase on the balance sheet. Changes in the former suggest greater effectiveness on output during this period, reducing it by 0.038% during the first month after that, an effect that loses strength in the following months. Changes in the balance sheet do not motivate an increase in output; on the contrary, they exert inverse effects, a situation that the study interprets as consistent with the conventional modus operandi where the conduct of policy is centered exclusively on the management of the policy rate. On the other hand, a 1% increase in the interest rate increases systemic risk, while the balance sheet generates a -0.107% reduction during the first subsequent month, followed by rapid diffusion of the effect. It is impossible to identify an inverse effect between inflation and the policy rate; however, a one percentage point increase in the latter causes a 0.05% increase in inflation after 12 months.

Table 4 Dynamic multipliers by periods of monetary policy

| CMP (2003:01-2008:08) | NCMP (2008:09-2019:12) | |||||

|---|---|---|---|---|---|---|

| 1 month | 6 months | 12 months | 1 month | 6 months | 12 months | |

| Unemployment rate ECB | ||||||

| Balance | -0.003 | -0.003 | -0.003 | -0.004 | -0.018 | -0.023 |

| Policy rate | -0.011 | -0.013 | -0.013 | 0.062 | 0.142 | 0.177 |

| Forward guidance | -0.009 | -0.082 | -0.107 | |||

| Production ECB Balance | -0.056 | -0.049 | -0.049 | 0.012 | 0.025 | 0.033 |

| Policy rate | -0.038 | 0.019 | 0.019 | 0.032 | -0.220 | -0.253 |

| Forward guidance | 0.096 | 0.222 | 0.254 | |||

| CISS ECB Balance | -0.107 | -0.065 | -0.065 | 0.504 | 0.468 | 0.530 |

| Policy rate | 0.305 | 0.383 | 0.385 | 1.803 | 1.724 | 1.395 |

| Forward guidance | 2.636 | 1.753 | 2.171 | |||

| Inflation ECB Balance | 0.018 | 0.016 | 0.016 | -0.003 | 0.001 | 0.004 |

| Policy rate | 0.063 | 0.050 | 0.050 | -0.009 | -0.076 | -0.092 |

| Forward guidance | -0.128 | -0.136 | -0.118 | |||

Notes: correspond to cumulative multipliers for time periods of 1, 6, and 12 months

Source: calculations by the author

The sub-period corresponding to NCMP makes it possible to identify changes in the unemployment rate from a one percentage point increase in the policy rate of 0.142% after the first 6months and 0.177% at 12 months. Forward guidance strategies present cumulative effects on the unemployment rate of -0.107% over the next 12 months, giving indications of the functioning of the expectations channel. Innovations in the ECB balance sheet continue to produce little effect, -0.023% after 12 months, although higher than that found in the CMP period.

In terms of output, the effects of changes in the policy rate begin to show with a lag, as reductions of -0.22 and -0.253% in the subsequent 6 and 12 months. In other words, a 1% cut in the policy rate improves output by 0.25% after one year. Balance sheet changes increase output by 0.033% over the same period. Forward guidance announcements are favorable for output and similar to those offered by policy rate changes. No reduction in the CISS is found from balance sheet increases or forward guidance announcements. Inflation has different effects due to changes in policy instruments; balance sheet expansion causes it to rise, whereas increases in the policy rate and forward guidance signaling cause it to fall.

As a robustness strategy, this study conducted panels with pooled, fixed effects, and random effects estimators for the CMP and NCMP sub-periods with the unemployment rate as the dependent variable. The results (see Table 5) do not make it possible to identify with statistical sufficiency the effectiveness resulting from the deposit facility rate nor the ECB balance sheet between 2003:01-2008:08; however, they do statistically strengthen the results found for the unconventional measures in the period 2008:08-2019:12. The parameters present similar implications to the PVAR: the decrease in the policy rate and forward guidance strategies are moderately effective in decreasing the unemployment rate, whereas balance sheet growth offers slight effectiveness. As with any econometric exercise, the results should be taken cautiously, favoring discussion and future estimations that reinforce or reject what is suggested here.

Table 5 Estimates using different methodologies

| CMP | NCMP | |||||

|---|---|---|---|---|---|---|

| Variables | Pooled | Random Effects | Fixed Effects | Pooled | Random Effects | Fixed Effects |

| y | -0.00979** | -0.00979** | -0.0102** | -0.0150 | -0.0150* | -0.0132 |

| (0.0368) | (0.0100) | (0.0344) | (0.112) | (0.0693) | (0.125) | |

| L.y | -0.00527 | -0.00527 | -0.00575 | -0.00962 | -0.00962 | -0.00770 |

| (0.183) | (0.140) | (0.176) | (0.194) | (0.151) | (0.246) | |

| p | -0.0983* | -0.0983** | -0.102* | -0.0242 | -0.0242* | -0.0164 |

| (0.0776) | (0.0388) | (0.0691) | (0.112) | (0.0689) | (0.320) | |

| L.p | 0.0550 | 0.0550* | 0.0513 | 0.0156 | 0.0156 | 0.0224 |

| (0.135) | (0.0916) | (0.176) | (0.182) | (0.138) | (0.101) | |

| dciss | 0.000812 | 0.000812 | 0.000841 | -0.00105 | -0.00105* | -0.00106 |

| (0.580) | (0.562) | (0.572) | (0.114) | (0.0712) | (0.107) | |

| L.dciss | -0.00254 | -0.00254* | -0.00259 | -0.000183 | -0.000183 | -0.000197 |

| (0.126) | (0.0825) | (0.118) | (0.805) | (0.797) | (0.791) | |

| Policy rate | -0.00562 | -0.00562 | -0.00538 | 0.0863** | 0.0863** | 0.0881** |

| (0.804) | (0.797) | (0.812) | (0.0387) | (0.0111) | (0.0357) | |

| ECB Balance | -0.00169 | -0.00169 | -0.00164 | -0.00374* | -0.00374** | -0.00392** |

| (0.529) | (0.508) | (0.540) | (0.0534) | (0.0203) | (0.0457) | |

| Forward guidance | -0.0625* | -0.0625** | -0.0613* | |||

| (0.0792) | (0.0401) | (0.0815) | ||||

| Constant | 0.00570 | 0.00570 | 0.00692 | 0.0360 | 0.0360* | 0.0340** |

| (0.896) | (0.892) | (0.879) | (0.124) | (0.0805) | (0.0296) | |

| Observations | 528 | 528 | 528 | 1 088 | 1 088 | 1 088 |

| ID number | 8 | 8 | 8 | 8 | ||

Notes: robust p-value in parentheses *** p<0.01, ** p<0.05, * p<0.1; L( ) refers to the first lag of the endogenous variable

Source: calculations by the author

The findings made it possible to argue that the NCMP has preserved its effectiveness in influencing output and the unemployment rate. However, this statement recognizes a certain nuance. The NCMP acted slowly, requiring a prolonged implementation, even with the capacity to influence macroeconomic variables. This is moderate when considering the magnitude of the effect produced, added to the observed inability of the ECB to achieve its inflation target since 2014.

It reinforces the evidence that policy rate reductions have real effects in reducing the unemployment rate and increasing output, a finding also suggested in the work of Laine (2020). This study confirms some effect-although of small magnitude-on output and inflation during the first 6 months in the face of balance sheet increases, which is in line with the evidence found in the papers by Buriel and Galesi (2016) and Gambacorta et al. (2014). The impact on the unemployment rate derived from the balance sheet and interest rate has no similarity across monetary policies. This leads to arguing that they are not substitutes but complementary instruments. In practice, the non-substitution is evident even with the expansion of the balance sheet. The ECB decided to continue cutting the policy rate and take it beyond the lower limit.

The significance of forward guidance and policy rate changes reinforces the initial hypothesis that the modus operandi of monetary policy has been modified but continues to achieve a change in output and unemployment. On the other hand, the lower contribution of the balance sheet can be explained by its significance in addressing segments of the financial market that hindered the adequate functioning of the transmission mechanism. Buriel and Galesi (2016) argue that balance sheet expansion has effectively reduced financial fragmentation, considering not only interbank credit conditions. Boeckx et al. (2014) also defend the hypothesis of positive balance sheet effects on credit conditions for companies and households. Therefore, its contribution to real economic performance is indirect and even focused during the first asset purchase programs.

Conclusions

After the 2008 crisis, the ECB adopted an unconventional monetary policy comprising four instruments: negative nominal interest rates for deposit facilities, use of the balance sheet through asset purchase programs, forward guidance signaling, and extraordinary liquidity. The literature indicates that using this monetary strategy can stabilize the economy's fundamentals. This study conducted three PVAR models with dynamic multipliers for a panel of eight countries over the period 2003-2019 to test the hypothesis, which made it possible to identify the effectiveness of NCMP instruments in reducing the unemployment rate and increasing output. The overall results suggest that changes resulting from decreases in the deposit facility rate and forward guidance signaling over a 12-month time period contract the dependent variable. The study finds a negative effect coming from an expansion of the balance sheet and a reduction in the CISS-following cuts in the policy rate. Moreover, estimating three simple models provides robustness and confidence to the econometric derivations.

The empirical evidence leads to the following result that constitutes the specific contribution of this study: the reduced effect of the instruments captured in the size of the dynamic multipliers and the parameters of the simple panel models are consistent with the slow decline in unemployment in the decade after the 2008 crisis. In this sense, the effectiveness of the NCMP is moderate concerning its unemployment stabilizing role and heterogeneous in terms of its instruments. Although the estimates are reliable, there is the possibility of extending the model by considering more countries in the region or fiscal, financial, or qualitative variables.

REFERENCES

Andrews, D. W. K. y Lu, B. (2001). Consistent model and moment selection procedures for GMM estimation with application to dynamic panel data models. Journal of Econometrics, 101 (1), 123-164. https://doi.org/10.1016/S0304-4076(00)00077-4 [ Links ]

Altavilla, C., L. Burlon, M. Giannetti, y S. Holton (2019). Is there a Zero Lower Bound? The Effects of Negative Policy Rates on Banks and Firms, ECB Working Paper Series No. 2289, European Central Bank. https://dx.doi.org/10.2139/ssrn.3402408 [ Links ]

Arellano, M. y Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68 (1), 29-51. https://doi.org/10.1016/0304-4076(94)01642-D [ Links ]

Berganza, J. C., I. Hernando y J. Vallés (2014). Los Desafíos para la Política Monetaria de las Economías Avanzadas tras la Gran Recesión, Documentos Ocasionales No. 1404, Banco de España. https://dx.doi.org/10.2139/ssrn.2497884 [ Links ]

Bernanke, B. S. (2017). Monetary Policy in a New Era. Brookings Institution. Disponible en: https://www.brookings.edu/wp-content/uploads/2017/10/bernanke_rethinking_macro_final.pdf . Consultado: 06/02/2021. [ Links ]

Bernanke, B. S. (2012). Monetary Policy since the Onset of the Crisis: a speech at the Federal Reserve Bank of Kansas City Economic Symposium, Jackson Hole, Wyoming, August 31, 2012, Board of Governors of the Federal Reserve System U.S. Speech 645. Wyoming: Federal Reserve System U.S. Disponible en: https://www.federalreserve.gov/newsevents/speech/bernanke20120831a.pdf . Consultado: 06/02/2021. [ Links ]

Bernanke, B. S., y Mishkin, F. S. (1997). Inflation Targeting: A New Framework for Monetary Policy? The Journal of Economic Perspectives, 11 (2), 97-116. https://doi.org/10.1257/jep.11.2.97 [ Links ]

Bernanke, B. S., y A. S. Blinder (1990). The Federal Funds Rate and the Channels of Monetary Transmission, NBER Working Paper No. 3487, National Bureau of Economic Research. https://doi.org/10.3386/w3487 [ Links ]

Beyer, A., Coeuré, B. y Mendicino, C. (2017). Foreword - The crisis, ten years after: Lessons learnt for monetary and financial research. Economie et Statistique / Economics and Statistics, Institut National de la Statistique et des Études Économiques, july-september (494-495-496), 45-64. https://doi.org/10.24187/ecostat.2017.494t.1918 [ Links ]

Boeckx, J., M. Dossche y G. Peersman (2014). Effectiveness and transmission of the ECB’s balance sheet policies, Working Paper Research No. 275, National Bank of Belgium. [ Links ]

Buriel, P. y A. Galesi (2016). Uncovering the Heterogeneous Effects of ECB Unconventional Monetary Policies Across Euro Area Countries, Documentos de trabajo No. 1631, Banco de España. [ Links ]

Campbell, J., Evans, C., Fisher J. y Justiniano A. (2012). Macroeconomic effects of Federal Reserve forward guidance. Brookings Papers on Economic Activity, 43(1), 1-80. https://doi.org/10.1353/eca.2012.0004 [ Links ]

Coenen, G., M. Ehrmann, G. Gaballo, P. Hoffmann, A. Nakov, S. Nardelli, E. Persson y G. Strasser (2017). Communication of Monetary Policy in Unconventional Times, ECB Working Paper Series No. 2080, European Central Bank. https://dx.doi.org/10.2139/ssrn.2993893 [ Links ]

Curdia, V., y Woodford, M. (2011). The central-bank balance sheet as an instrument of monetarypolicy. Journal of Monetary Economics, 58(1), 54-79. https://doi.org/10.1016/j.jmoneco.2010.09.011 [ Links ]

Dell'Ariccia, G., Rabanal, P., y Sandri, D. (2018). Unconventional monetary policies in the euro area, Japan, and the United Kingdom. Journal of Economic Perspectives, 32(4), 147-72. https://doi.org/10.1257/jep.32.4.147 [ Links ]

Denton, F. (1971). Adjustment of monthly or quarterly series to annual totals: An approach based on quadratic minimization. Journal of the American Statistical Association, 66 (333), 99-102. https://doi.org/10.2307/2284856 [ Links ]

Elbourne, A., Ji, K. y S. Duijndam (2018). The effects of unconventional monetary policy in the euro area, CPB Discussion Paper No. 371, Netherlands Bureau for Economic Policy Analysis. [ Links ]

Farmer, R., y Zabczyk, P. (2016). The theory of unconventional monetary policy, NBER Working Paper No. w22135, National Bureau of Economic Research. https://doi.org/10.3386/w22135 [ Links ]

Gambacorta L., Hofmann, B. y Peersman, G. (2014). The Effectiveness of Unconventional Monetary Policy at the Zero Lower Bound: A Cross-Country Analysis. Journal of Money, Credit and Banking, 46 (4), 615-642. https://doi.org/10.1111/jmcb.12119 [ Links ]

Gambetti, L. y A. Musso (2017). The macroeconomic impact of the ECB’s expanded asset purchase programme (APP), ECB Working Paper Series No. 2075, European Central Bank. https://dx.doi.org/10.2139/ssrn.2985385 [ Links ]

Giannone, D., Lenza, M., Pill, H., y Reichlin, L. (2011). Non-standard monetary policy measures and monetary developments., ECB Working Papers Series No. 1290, European Central Bank. https://doi.org/10.1017/CBO9781139044233.008 [ Links ]

Hachula, M., Piffer, M., y Rieth, M. (2020). Unconventional monetary policy, fiscal side effects, and euro area (im) balances. Journal of the European Economic Association, 18(1), 202-231. https://doi.org/10.1093/jeea/jvy052 [ Links ]

Holtz-Eakin, D., Newey, W. y Rosen, H. S. (1988). Estimating vector autoregressions with panel data. Econometrica, 56 (6), 1371-1395. https://doi.org/10.2307/1913103 [ Links ]

Laine, O. J. (2020). The effect of the ECB’s conventional monetary policy on the real economy: FAVAR-approach. Empirical Economics. 59 (6), 2899-2924. https://doi.org/10.1007/s00181-019-01739-9 [ Links ]

Lenza, M., H. Pill y L. Raichlin (2010). Monetary Policy in Exceptional Times, ECB Working Papers Series No. 1253, European Central Bank. https://dx.doi.org/10.2139/ssrn.1683963 [ Links ]

Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis, Springer: Berlin. [ Links ]

Millaruelo, A. y A. Del Río (2013). Las Medidas de Política Monetaria No Convencionales del BCE a lo Largo de la Crisis, Boletín Económico 01/2013, Banco de España. Disponible en: https://www.bde.es/f/webbde/SES/Secciones/Publicaciones/InformesBoletinesRevistas/BoletinEconomico/13/Ene/Fich/be1301.pdf . Consultado: 29/01/2021. [ Links ]

Okun, A. (1962). Potential GNP: Its Measurement and Significance, Cowles Foundation Paper 190, Yale University. [ Links ]

Potter, S. M. y F. Smets (2019). Unconventional monetary policy tools: a cross-country analysis, BIS CGFS Papers No 63, Bank for International Settlements. [ Links ]

1Guidance can be of the Delphic type when it offers a forecast of how it expects macroeconomic variables to behave and its reaction or odyssey when it undertakes to carry out a certain policy (Campbell, 2012).

2CISS corresponds to an index that measures systemic risk that considers a broad segment of the financial market by including money markets, fixed and variable income assets, currencies, and financial intermediaries.

4Obtained by Denton's (1971) interpolation method using as a high frequency series the industry production index (2015=100). Once interpolated, it was adjusted for inflation with the monthly CPI (2015=100).

5The differentiation of policy rates causes loss of information and predictive capacity, which is aggravated in cases where the rate does not change for several periods. Works such as Bernanke and Blinder (1990) consider this to be an inadequate approach.

Anexx

Table A1 Panel cointegration tests

| Kao Test | ||

|---|---|---|

| Statistic | p-value | |

| Modified Dickey-Fuller | -100 | 0 |

| Dickey-Fuller | -22.9773 | 0 |

| Augmented Dickey-Fuller | -15.5027 | 0 |

| Modified Dickey-Fuller (unadjusted) | -92.8316 | 0 |

| Dickey-Fuller (unadjusted) | -23.2324 | 0 |

| Number of panels | 8 | |

| Number of periods | 201 | |

| Kernel: | Bartlett | |

| Lags | 3.38 | (Newey-West) |

| Increased lags | 1 | |

Ho: All panels are not cointegrated

Source: created by the author

Table A2 Panel cointegration tests

| Pedroni Test | ||

|---|---|---|

| Time trend: not included | Statistic | p-value |

| Modified Phillips-Perron | -23.1102 | 0 |

| Phillips-Perron | -20.8112 | 0 |

| Dickey-Fuller Augmented | -22.2859 | 0 |

| Number of panels | 8 | |

| Number of periods | 202 | |

| Kernel | Bartlett | |

| Lags | 0.00 | (Newey-West) |

| Increased lags | 1 | |

| Time trend: included | Statistic | p-value |

| Modified Phillips-Perron | -20.8246 | 0 |

| Phillips-Perron | -20.07 | 0 |

| Dickey-Fuller Augmented | -21.6159 | 0 |

| Number of panels | 8 | |

| Number of periods | 202 | |

| Kernel: | Bartlett | |

| Lags | 0.00 | (Newey-West) |

| Increased lags | 1 | |

Ho: All panels are not cointegrated

Source: created by the author

Table A3 PVAR Estimates

| Model 1, 2003:01-2019:12 | Model 2, 2003:01-2008:08 | Model 3, 2008:08-2019:12 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Variables | Unempl oyment rate (du) | GDP (y) | CPI (p) | CISS (dciss) | Unempl oyment rate (du) | GDP (y) | CPI (p) | CISS (dciss) | Unempl oyment rate (du) | GDP (y) | CPI (p) | CISS (dciss) |

| L.du | 0.435*** | 0.857 | 0.0867 | 7.850** | 0.332*** | -3.448*** | 0.327*** | -2.242* | 0.424*** | 1.313 | 0.091 | 6.370* |

| (0.000) | (0.343) | (0.588) | (0.026) | (0.000) | (0.000) | (0.000) | (0.076) | (0.000) | (0.117) | (0.525) | (0.077) | |

| L2.du | 0.409*** | -1.524* | -0.392*** | 2.446 | 0.459*** | -1.333* | -0.308** | 2.147 | ||||

| (0.000) | (0.052) | (0.006) | (0.459) | (0.000) | (0.072) | (0.021) | (0.498) | |||||

| L3.du | -0.064 | -0.688 | -0.144 | -8.867*** | -0.092 | -1.177 | -0.251* | -3.180 | ||||

| (0.460) | (0.368) | (0.283) | (0.002) | (0.313) | (0.108) | (0.053) | (0.304) | |||||

| L.y | -0.015 | -0.476*** | -0.069*** | -0.243 | -0.015*** | -0.612*** | 0.003 | -0.912*** | -0.003 | -0.712*** | -0.028 | 1.213*** |

| (0.236) | (0.000) | (0.003) | (0.579) | (0.001) | (0.000) | (0.700) | (0.000) | (0.765) | (0.000) | (0.154) | (0.010) | |

| L2.y | -0.057*** | 0.112 | 0.006 | 1.333*** | -0.043*** | -0.001 | 0.004 | 1.730*** | ||||

| (0.000) | (0.388) | (0.797) | (0.006) | (0.000) | (0.990) | (0.843) | (0.000) | |||||

| L3.y | -0.030*** | 0.0857 | 0.018 | 1.009** | -0.018* | -0.059 | -0.002 | 0.962** | ||||

| (0.004) | (0.491) | (0.352) | (0.023) | (0.084) | (0.590) | (0.915) | (0.025) | |||||

| L.p | 0.085 | 0.53 | -0.106 | 1.219 | 0.097** | -0.908* | 0.073 | 5.076*** | 0.204*** | 0.604 | -0.231** | 1.849 |

| (0.239) | (0.462) | (0.347) | (0.642) | (0.033) | (0.085) | (0.278) | (0.000) | (0.006) | (0.404) | (0.030) | (0.522) | |

| L2.p | -0.145** | 0.515 | 0.070 | 3.155 | -0.137* | -0.169 | 0.092 | 1.937 | ||||

| (0.039) | (0.476) | (0.575) | (0.275) | (0.056) | (0.817) | (0.429) | (0.515) | |||||

| L3.p | 0.074 | 0.720 | 0.098 | -0.0896 | 0.102 | 0.551 | 0.136 | 0.582 | ||||

| (0.269) | (0.234) | (0.369) | (0.973) | (0.147) | (0.380) | (0.197) | (0.839) | |||||

| L.dciss | -0.002 | 0.036 | -0.012*** | 0.008 | 0.001 | 0.201*** | -0.028*** | 0.450*** | -0.001 | 0.017 | -0.010*** | 0.156* |

| (0.319) | (0.105) | (0.001) | (0.930) | (0.740) | (0.000) | (0.000) | (0.000) | (0.613) | (0.417) | (0.004) | (0.092) | |

| L2.dciss | 0.001 | 0.017 | -0.001 | 0.034 | 0.003 | 0.028 | -0.006 | 0.031 | ||||

| (0.596) | (0.444) | (0.746) | (0.703) | (0.182) | (0.157) | (0.105) | (0.719) | |||||

| L3.dciss | -0.004* | -0.027 | 0.002 | 0.0849 | -0.004** | -0.039** | 0.002 | -0.003 | ||||

| (0.087) | (0.203) | (0.549) | (0.375) | (0.049) | (0.041) | (0.557) | (0.975) | |||||

| Polic y rate | 0.009 | -0.049 | 0.008 | 0.300 | -0.014*** | -0.046 | 0.061*** | -0.053 | 0.045*** | -0.174 | -0.003 | 1.501*** |

| (0.161) | (0.412) | (0.440) | (0.197) | (0.000) | (0.331) | (0.000) | (0.612) | (0.005) | (0.275) | (0.878) | (0.007) | |

| ECB Bala nce Sheet | 0.0002 | -0.017 | 0.007*** | 0.408*** | -0.004** | -0.060** | 0.014*** | -0.167*** | -0.003 | 0.024 | 0.003 | 0.423*** |

| (0.905) | (0.285) | (0.007) | (0.000) | (0.017) | (0.023) | (0.000) | (0.007) | (0.115) | (0.175) | (0.261) | (0.000) | |

| Forward guidance | 0.002 | 0.226 | -0.128*** | 1.051* | 0.014 | 0.417** | -0.127*** | 1.968*** | ||||

| (0.934) | (0.207) | (0.000) | (0.099) | (0.427) | (0.015) | (0.000) | (0.002) | |||||

| Obs. | 1 592 | 1 592 | 1 592 | 1 592 | 528 | 528 | 528 | 528 | 1 080 | 1 080 | 1 080 | 1 080 |

Note: robust p-value in parentheses *** p<0.01, ** p<0.05, * p<0.1

Source: calculations by the author

Table A4 Optimal order of lags and instruments

| Model 1 (2003:01- 2019:12) |

Lags (Instruments) |

AR | CD | J | J-pvalue | MBIC | MAIC | MQIC | Obs. |

|---|---|---|---|---|---|---|---|---|---|

| L.(5) - L.20) | 1 | 0.1478 | 346.6493 | 0.0000 | -1 422.8100 | -133.3507 | -612.2901 | 1 592 | |

| 2 | -0.0034 | 289.4875 | 0.0021 | -1 362.0080 | -158.5125 | -605.5225 | |||

| 3 | -0.0719 | 215.1414 | 0.3524 | -1 318.3900 | -200.8586 | -615.9393 | |||

| Model 1 (2003:01- 2008:08) |

Lags (Instruments) |

AR | CD | J | J-pvalue | MBIC | MAIC | MQIC | Obs. |

| L.(5) - L.20) | 1 | 0.7780 | 230.6789 | 0.6556 | -1 266.5190 | -249.3211 | -648.0627 | 512 | |

| 2 | 0.5423 | 222.9008 | 0.5082 | -1 174.4840 | -225.0992 | -597.2581 | |||

| 3 | -2.3128 | 193.5191 | 0.7562 | -1 104.0520 | -222.4809 | -568.0569 | |||

| Model 1 (2008:09- 2019:12) |

Lags (Instruments) |

AR | CD | J | J-pvalue | MBIC | MAIC | MQIC | Obs. |

| 1 | -0.0619 | 341.7993 | 0.0000 | -1 334.5330 | -138.2007 | -591.1884 | 1 080 | ||

| 2 | -0.0936 | 286.2760 | 0.0031 | -1 278.3000 | -161.7240 | -584.5125 | |||

| 3 | 0.2065 | 216.9665 | 0.3206 | -1 235.8540 | -199.0335 | -591.6228 |

Notes: The MMSC criterion suggests selecting the AR order that minimizes the criteria and shares correct specification given a certain set of instrumented lags, i.e., one that does not reject the J-pvalue.

L( ) refers to lag i used as an instrument

Source: calculations by the author

Table A5 Stability condition

| Model 1 (2003:01-2019:12) | Model 2 (2003:01-2008:08) | Model 3 (2008:09-2019:12) | ||||||

|---|---|---|---|---|---|---|---|---|

| Eigenvalue | Module | Eigenvalue | Module | Eigenvalue | Module | |||

| Real | Imaginary | Real | Imaginary | Real | Imaginary | |||

| 0.9837 | 0.0000 | 0.9837 | -0.5148 | 0.0000 | 0.5148 | 0.8644 | 0.0000 | 0.8644 |

| -0.6910 | 0.0000 | 0.6910 | 0.1969 | -0.3730 | 0.4218 | -0.7726 | 0.0000 | 0.7726 |

| 0.4858 | 0.4516 | 0.6633 | 0.1969 | 0.3730 | 0.4218 | 0.5842 | -0.4161 | 0.7172 |

| 0.4858 | -0.4516 | 0.6633 | 0.3639 | 0.0000 | 0.3639 | 0.5842 | 0.4161 | 0.7172 |

| -0.1352 | 0.6112 | 0.6260 | -0.6798 | 0.0000 | 0.6798 | |||

| -0.1352 | -0.6112 | 0.6260 | -0.0579 | -0.5762 | 0.5791 | |||

| -0.5411 | 0.1687 | 0.5668 | -0.0579 | 0.5762 | 0.5791 | |||

| -0.5411 | -0.1687 | 0.5668 | -0.4628 | 0.2834 | 0.5427 | |||

| -0.3704 | -0.3993 | 0.5446 | -0.4628 | -0.2834 | 0.5427 | |||

| -0.3704 | 0.3993 | 0.5446 | 0.4208 | 0.0000 | 0.4208 | |||

| 0.3450 | 0.0613 | 0.3503 | -0.1618 | -0.1900 | 0.2496 | |||

| 0.3450 | -0.0613 | 0.3503 | -0.1618 | 0.1900 | 0.2496 | |||

Source: calculations by the author

Received: April 21, 2021; Accepted: June 27, 2022; Published: June 27, 2022

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons