nova página do texto(beta)

nova página do texto(beta) Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Similares em

SciELO

Similares em

SciELO

Permalink

Permalink

Introduction

Most orthodox economists share consensus regarding the determinants of Mexico's slow economic growth. According to them, the problem was explained by the country's incapacity to implement second-generation structural reforms to complement the international integration strategy, along with a poor institutional environment characterized by a want of rule of law. In their narrative, a process of adjustment and structural change began in the aftermath of the 1982 external debt crisis. Fiscal and external accounts were brought into equilibrium, and the inflation rate was controlled. Through an ample process of deregulation, privatization, and liberalization, distortions were eliminated and competition in key markets was promoted. Moreover, an institutional convergence effort was set forth, manifested in the creation of essential liberal institutions, while others were strengthened by gaining constitutional autonomy (i. e. Banco de México in 1994). With the entry into force of the North America Free Trade Agreement (Nafta), a mechanism for consolidating the institutional changes achieved, the first generation of reforms saw their crowning moment.

In their account, everything was going according to schedule, until a set of economic and political events provoked a “reform fatigue” that truncated the structural change process.1 It is often asserted that the complementary reforms needed for benefiting from the opening of trade and finance were not implemented because, from a political economy perspective, vested interests defended their privileges to the detriment of the general productivity level. Labor markets remained rigid, public education under the control of teachers' unions, and essential input markets uncompetitive. The binding constraints to economic growth are henceforth insufficient human capital, non-competitive key sectors, distortions that affect productive firms while subsidizing unproductive ones, and a weak state of law.2 An inefficient allocation of resources follows, diminishing Total Factor Productivity (TFP) and output growth. The Pacto por México (2012), 11 neoliberal second-generation reforms3 that were approved in the first third of Enrique Peña Nieto's mandate (2012-2018), sought to overcome these problems. Yet, at least until now, it has not delivered the expected results.

Regardless of its popularity, we believe that this diagnosis misses the central factor behind Mexico's stagnated economy: a slow rate of capital accumulation that is mediated by a lack of profitability in the modern sectors. In this paper, we address the following question: why have the Pacto por México structural reforms not transformed the country's productive structure through an accelerated process of capital accumulation?

The paper is divided as follows. In the first section, we analyze the latest economic census, concluding that Mexico is a paradigmatic example of a dual economy. In the second section, searching for an alternative explanation of the causes behind economic stagnation, we review some of the classical development theory (CDT) lessons. In the third section, based on this framework, we advance a hypothesis of the reasons behind the ineffectiveness of the Pacto por México reforms. We conclude with some remarks.

I. The mexican economy productive structure

The uneven growth patterns of the Mexican economy have generated a dualistic productive structure. On the one hand, there are some highly productive firms, many of which compete in international markets, such as Bimbo or Telcel. On the other hand, there is a myriad of low-productivity and traditional firms, mostly producing non-tradable goods and services using labor-intensive technologies. The share of resources employed by the high-productivity firms is small in comparison with those of low-productivity ones. And, as Levy (2018) has consistently documented, there has been a “dysfunctional dynamic” in which the share of resources allocated to micro, unproductive and informal firms has risen over the last decades.

To illustrate this point, we analyzed the Censo Económico 2018 (the census), published by the Mexican National Statistical Office (Inegi). Elaborated every five years, it surveys firms located in populations with over 2,500 inhabitants that operate in fixed establishments. This represents a shortcoming since millions of people survive in rural activities or informal jobs done on the streets. Levy (2018), for instance, estimated that in 2013 around 2.6 million economic units employing 7.6 million workers were not located on fixed premises. Notwithstanding, in its latest edition, it surveyed around 4.8 million firms that employed over 27 million workers.

The census organizes data according to the North American Industry Classification System (Naics). At its highest level of disaggregation, it provides information for 1,084 economic sectors, divided into 186 different dimensions. We choose six of these variables: firms, value-added, total workers employed, non-remunerated workers employed, gross fixed capital formation (GFCF), and capital stock. With them, we constructed indicators for labor productivity (value-added/total workers employed) and capital per worker (capital stock/total workers employed). We applied a Tukey test, eliminating those observations in which the productivity of labor was three times above the third quartile or three times below the first quartile. At the cost of removing some of the most productive firms, we eliminated outliers that would have skewed the distribution even further. Table 1 shows the distribution of our selected variables according to the formality status of firms.

Table 1 Distribution of Selected Variables according to the Firms' Formality Status

| Concept | Total | Formal | Informal | Formal under

mean productivity of labor |

Informal under

mean productivity of labor |

| Firms | 4,774,111 | 37.4% | 62.6% | 93.8% | 100.0% |

| Value Added | 7,792,481 | 96.1% | 3.9% | 52.4% | 99.3% |

| Total Workers Employed | 25,521,852 | 80.1% | 19.9% | 82.0% | 100.0% |

| Non Remunerated Workers | 6,153,335 | 35.2% | 64.8% | 97.0% | 100.0% |

| Gross Fixed Capital Formation | 444,189 | 102.6% | -2.6% | 38.6% | 100.0% |

| Capital Stock | 8,311,242 | 96.6% | 3.4% | 45.9% | 99.9% |

Source: Own elaboration with data from the Censo Económico 2018, Instituto Nacional de Estadística y Geografía.

Notes: Monetary values are expressed in millions of Mexican pesos.

Though 63% of the firms censused are informal, they only generate 3.9% of the value-added, employ 19.9% of total workers,4 and possess 3.4% of the capital stock. Moreover, gross fixed capital formation (GFCF) in the informal sector was negative, indicating that in some economic activities the accumulation of capital has been negative. This fact is worrying since it underlines the fact that capital in the informal sector is decreasing, even though the absolute amount of people employed has risen over the years. It is worthwhile stressing that 64.8% of the non-remunerated workers are employed in the informal sector. Unlike Levy (2018), we assume that in most cases this bellies a “disguised unemployment”.5

Data shows that most informal firms are small and unproductive. The average number of workers per firm in the informal sector is only 1.7, whereas it is 11.45 in the formal sector. Moreover, our productivity of labor indicator tells us that, on average, formal firms are 376% more productive than informal ones. Indeed, while 93.8% of formal firms are under our mean labor productivity indicator, practically all informal firms are in this situation.

Unfortunately, the census does not provide data for firm size differentiating by formality status. Nonetheless, in Table 2 we present aggregate data by size.6

Table 2 Distribution of Variables by Firm Size

| Total | Micro | Small | Medium | Large | |

| Firms | 4,770,918 | 95.07% | 3.96% | 0.77% | 0.20% |

| Value Added | 6,174,927 | 19.43% | 18.00% | 22.67% | 39.98% |

| Total Workers Employed | 25,332,132 | 39.66% | 15.52% | 15.38% | 29.44% |

| Non Remunerated Workers | 6,150,047 | 93.57% | 4.91% | 1.10% | 0.42% |

| Gross Fixed Capital Formation | 467,787 | 5.07% | 8.15% | 24.96% | 61.82% |

| Capital Stock | 6,775,681 | 17.63% | 18.21% | 20.82% | 43.34% |

Source: Own elaboration with data from the Censo Económico 2018, Instituto Nacional de Estadística y Geografía.

Notes: Monetary values are expressed in millions of Mexican pesos.

The distribution is highly skewed towards micro-firms; more than 95% of economic units employ five workers or less. Despite most being enterprises, they only generate 19.4% of the value-added and possess 17.6% of the capital stock. In addition, they employ 93.5% of all non-remunerated workers, implying that their vast majority are family businesses. By contrast, representing only 0.2% of the total, large firms generate almost 40% of the value-added, employ 29.4% of total workers, own 43.3% of the capital stock, and concentrate 61.8% of GFCF.

As firm size increases, the shares of value-added, GFCF, and the capital stock soar, while that of non-remunerated workers diminishes. There is a positive relation between firm size and productivity level. For instance, employing 26% fewer workers than micro firms, large economic units generate more than twice the value-added. The mean labor productivity of large firms (.35) is, on average, two times the value of micro-ones (.17). Table 3 shows the percentage of variables that are under the mean productivity of labor.

Table 3 Percentage of Variables under the Mean of Productivity of Labor and Capital per Worker

| Variable | Total | Under the

mean productivity of labor |

Three

Standard Deviations Above the Mean |

Under the

mean capital per worker |

| Firms | 4,770,918 | 93.24% | 0.10% | 95.07% |

| Value Added | 6,174,927 | 38.21% | 6.03% | 65.46% |

| Total Workers Employed | 25,332,132 | 70.13% | 1.32% | 81.47% |

| Non Remunerated Workers | 6,150,047 | 36.32% | 0.04% | 96.41% |

| Gross Fixed Capital Formation | 467,787 | 21.66% | 5.06% | 27.43% |

| Capital Stock | 6,775,681 | 33.82% | 5.59% | 34.44% |

Source: Own elaboration with data from the Censo Económico 2018, Instituto Nacional de Estadística y Geografía.

Notes: Monetary values are expressed in millions of Mexican pesos.

As we can see, 93.2% of firms are under the mean productivity of labor, employing 70.1% of workers, generating 38.2% of the value-added, and owning 33.8% of the capital stock. Only 0.10% of the firms, by contrast, are three standard deviations above the mean. These enterprises generate 6% of the value-added, employ 1.32% of the censused workers, and possess 5.6% of the capital stock. From a universe of more than 25 million workers, only 334,384 are hired by these modern and productive firms.

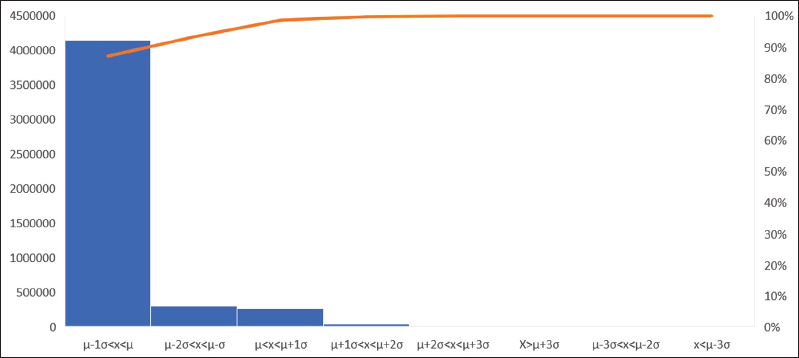

Figure 1 shows the frequency distribution of all firms according to our productivity of labor indicator:

Around 90% of firms (4,148,498) are located between the mean of labor productivity and one standard deviation below (µ-1σ<x<µ). To place these results in perspective, compare this with the 5% of firms (260,920) with labor productivity between the mean and one standard deviation above (µ<x<µ+1σ). The distribution skewness is 1.44, signaling that most firms are micro and unproductive. Table 4 shows the percentage of variables under the mean labor productivity by firm size.

Table 4 Variables under the Mean Productivity of Labor (as a percentage of each Firm's size values)

| Firm Size | Firms | Value Added | Total

Workers Employed |

Non Remunerated |

Gross

Fixed Capital Formation |

Capital Stock |

| Micro | 94.92% | 69.76% | 91.71% | 96.32% | 100.00% | 71.42% |

| Small | 62.79% | 35.09% | 62.53% | 88.93% | 39.98% | 33.05% |

| Medium | 51.64% | 28.41% | 49.89% | 88.98% | 15.43% | 32.32% |

| Large | 58.25% | 29.76% | 55.64% | 95.31% | 14.68% | 29.69% |

Source: Own elaboration with data from the Censo Económico 2018, Instituto Nacional de Estadística y Geografía.

Around 95% of micro firms are under the mean, generating 69.7% of the value-added, employing 91.7% of total workers and 96.8% of the non-remunerated workers, while possessing 71.4% of the capital stock of all micro firms. In contrast, only 58.2% of large firms are under the mean of this indicator, generating 29.8% of value-added, employing 55.6% of total workers, explaining 14.7% of GFCF, and holding 29.6% of the capital stock of large firms. In the case of large firms, value-added, capital stock, and GFCF are concentrated in firms with labor productivity over the average.

Now, for appraising the activities in which unproductive firms are located, we selected those units that are under the mean of labor productivity and arranged data by firm size.

Table 5 Variables under the Mean Productivity of Labor by Economic Sector (as percentage of values under the mean productivity of labor)

| Economie Sector/Firm Size | Firms | Value Added | Total Workers | Non-remunerated workers | GFCF | Capital Stock |

| Manufacturing | ||||||

| Micro | 12.17% | 4.27% | 7.07% | 12.43% | 2.88% | 3,S2% |

| Small | 2.67% | 16.53% | 13.84% | 4.53% | 15.04% | 17.79% |

| Retail Trade | ||||||

| Micro | 43.02% | 15.43% | 20.17% | 41.10% | 7.52% | 11.13% |

| Small | 0.32% | 2.61% | 1.53% | 0.13% | 4.00% | 3.11% |

| Accomodation and Food Services | ||||||

| Micro | 13.67% | 5.01% | 9.06% | 15.17% | 2.80% | 5.45% |

| Small | 0.57% | 3.16% | 2.90% | 0.39% | 2.51% | 3.92% |

| Total | 72.42% | 47.02% | 54.57% | 73.75% | 34.75% | 45.22% |

Source: Own elaboration with data from the Censo Económico 2018, Instituto Nacional de Estadística y Geografía.

Although the census is divided into 20 activities, 72.4% of firms with a productivity of labor under the average are micro and small operating in three of them: manufacturing (14.84%), retail trade (43.34%), and accommodation and food services (14.24%). These are, to a large extent, the self-employment businesses that proliferate through Mexican cities: bakeries, shoe stores, tortillerías, small restaurants, and grocery stores, among other micro and uncapitalized firms. This employment structure sheds light on the calculations of Ros (2011), who documented that from 1980 to 2005 the share of people employed in the service sector increased, provoking an aggregate labor productivity decrease. This also confirms the findings of McMillan et al. (2014), who pointed out that in Latin America globalization has typically brought a growth-reducing structural change, characterized by the transfer of resources from manufacturing to low-productivity service sectors that serve as “employers of last resort”.

Recapitulating, we can conclude that the distribution of firms in Mexico is skewed toward micro, informal, and unproductive. Moreover, there is an acute gap in the labor productivity of large/formal and micro/informal, with the former presenting levels consistently above the latter. In sum: Mexico is a paradigmatic example of a dual economy.

II. Economic growth and classical development theory (CDT)

The so-called new growth theory stressed how knowledge Romer (1986), human capital Lucas (1988), and research and development Aghion et al. (1992) are essential factors for increasing potential output growth. However, these models were built for the conditions of mature economies, where modern capital-intensive sectors prevail. Accordingly, they lack a proper structure for explaining one of the most salient features of underdeveloped economies: the interdependence of modern and traditional sectors and firms.

This structural heterogeneity, in contrast, is well-captured by the CDT.7 Authors such as Ragnar Nurkse (1952), Arthur Lewis (1954), Paul Rosenstein-Rodan (1943), and Albert O. Hirschman (1958) understood how duality is both a cause and a consequence of underdevelopment. In this section, we will present an endogenous growth model that is indebted to this theoretical tradition. But first, we will address some of its core elements.

In a paper that had a profound influence on the international development practice, Rosenstein-Rodan (1943) departed from the neoclassical paradigm by postulating an aggregate production function with increasing returns to scale (IRS).8 Capital accumulation, he asserted, has spillover effects in the form of pecuniary externalities. He used the example of a shoe factory in a poor country that would be unprofitable due to the limited size of the domestic market. In his story, if many sectors industrialized at the same time, the increased demand would make the shoe factory and other industries that invested in expanding their capacity profitable. In other words, by increasing wages and profits, these investments would create additional markets. Moreover, procuring “social overhead capital” also requires an industrialization process, since due to indivisibilities and minimal efficient scales of operation, it would only be profitably built if several firms use it. The core of his argument is that there are “coordination failures” due to market failures such as asymmetric information, an imperfect appropriability of external economies, or missing markets. Economies are prone, thus, to getting trapped in low-industrialization equilibria. What could be done to overcome these failures and benefit from these positive externalities? The author proposed programming a “big push” -coordinated and simultaneous planning of complementary industries- that generates the critical mass of investment required for eradicating the bottlenecks found in the development process.

In his seminal contribution, Lewis (1954) complemented Rodan's ideas by positing that in underdeveloped economies a capitalist and a subsistence sector interact -the difference being that the former is “fructified” by capital while the latter is not. Underdeveloped economies have a shortage of capital in relation to the population size, provoking a surplus of labor that is forced to find employment in subsistence activities. This being so, the subsistence sector has negligible marginal productivity, so labor can be withdrawn from it without diminishing output. Henceforth, the subsistence sector provides “unlimited supplies of labor” at a constant real wage, which amounts to the subsistence incomes plus a premium to account for higher urban living costs. The assumption of an elastic supply of labor at constant real wage entails that, so long as the average productivity of labor in the subsistence sector does not increase with its migration to the capitalist sector, capital accumulation would not provoke an increase in the real wages of the modern sector. Also, the subsistence sector imposes a floor on real wages, so a point is reached when increasing aggregate demand further does not reduce real wages and hence causes higher employment in the modern sector. Unlike advanced economies, where unemployment is provoked by insufficiency of effective demand, in underdeveloped economies it is conditioned by a shortage of capital per worker. The solution to underdevelopment is thus associated with increasing capital accumulation and not with Keynesian management of aggregate demand. Redundant workers could only be absorbed in the capitalist sector by investing in “progressive activities”, which would raise the profit share and hence stimulate further capital accumulation until the labor surplus has disappeared and the economy reaches maturity.

Hirschman (1958) rejected the idea of “balanced growth”, implicit in Rodan's paper, and put forth an “unbalanced growth” theory. If poor countries were endowed with the resources required to start a balanced growth process, he argued, they would not be underdeveloped. In contrast, development is a never-ending process of disequilibria, in which investment opportunities found in certain activities “induce” subsequent and complementary actions. Once an entrepreneur installs a beer factory, for example, the incentives for harvesting barley, constructing a bottling plant, or brewing substitutes are put in place in an uneven cumulative causation process. Likewise, one investment project could provide indispensable resources for the realization of numerous other economic activities, such as when an essential commodity starts being produced. Even imports signal the existing demand for goods not produced locally and hence stimulate the production of import substitutes. Development should be understood as a permanent process of widening the range of activities an economy performs through this process of discovery, disequilibria, and inducement. Naturally, it hinges upon several factors, including institutional and financial constraints, so policy should focus on spawning the proper conditions for creating and strengthening the “forward and backward linkages” between economic activities and sectors. An industrialization project must be engineered, as envisaged by Rodan, by prioritizing sectors that generate the highest positive externalities and induce stronger linkages.

This theoretical paradigm addresses several of the structural conditions of underdeveloped economies, paramount among them the interdependence of modern and traditional sectors in the same economic space. Nevertheless, it was dismissed by mainstream economics for at least the following reasons: It was deemed “logically meaningless” for its lack of mathematical foundations (Krugman, 1992); its policy prescriptions denied the markets-efficiency proposition (Stiglitz, 1992); policymakers drew the wrong lessons (Matsuyama, 1995), and many of the development projects based on it failed due to poor institutional environments (Easterly, 2006). Even the late Hirschman (1982) recognized that “third world disasters”, like humanitarian crises or coups d'état, made the development process more complex than originally thought. Thus, the theoretical explanation of the causes of underdevelopment shifted from lack of physical capital (1940-70) to entrepreneurship (1958-65), incorrect relative prices (1970-80), missing international trade (1980), and human capital (1988) (Adelman, 2000). With the advantage of hindsight, we may add that the now dominant paradigm could be resumed as “getting institutions right”, a euphemism for liberal policies of the Washington Consensus kind such as deregulating markets, privatizing public firms, and securing property rights Acemoglu and Robinson (2012).

Nonetheless, the East Asia Tigers' remarkable experience revived interest in industrialization as a source of structural change. Many relevant authors supported this idea. Krugman (1994), for instance, asserted that East Asia's growth performance was explained by the accumulation of production factors and not by allocative efficiency gains. In a similar vein, Rodrik (1994) stressed that the growth miracles of Korea and Taiwan were more related to public interventions that eliminated coordination failures and fostered linkages than to an exportled strategy. Utilizing an aggregate meta-production function, Kim and Lau (1993) estimated that between 48 and 72% of the four East Asia tigers' growth was provoked by capital accumulation. Analyzing the case of Singapore, Young (1992) concluded that between 1970 and 1990 practically all the growth of output per worker was explained by capital accumulation, whereas TFP had a negative contribution.

With the reassessment of capital accumulation as a source of structural change, the 1980s saw the revival of models with IRS, coordination failures, multiple equilibria, and interdependence between sectors. Below, we will review some of this literature.

The first successful attempt to formalize Rodan's big push argument was undertaken by Murphy et al. (1989), who proposed a set of models in which firms with constant and IRS technologies interact. In their models, the extent of the domestic market, and hence the profits of modern firms, are a positive function of the number of sectors that adopt IRS technologies. The authors demonstrated that by raising wages and profits, simultaneous industrialization would make the adoption of IRS technologies profitable, even if no firm would break even in isolation. Moreover, it would only be profitable to build large infrastructure projects if sufficient IRS sectors use it at the same time, for this allows defraying their large inherent fixed costs. As a result, industrialization also makes it profitable to build strategic infrastructure, which reduces IRS firms' production costs. In both cases, be it because it increases demand or reduces costs, industrialization causes pecuniary external effects that steer the economy towards a high-income equilibrium.

Drawing on Young (1928), a related model was proposed by Rodríguez-Claire (1996), who provided a formalization of Adam Smith's proposition that the division of labor depends on the extent of the market that depends on the division of labor. In his presentation, a final goods sector with two firms and an intermediate goods sector with one firm are interdependent. In the final goods sector, one of the firms is capital-intensive and the other is not, whilst the sole intermediate-goods sector's firm operates under IRS. There is a coordination failure: the capital-intensive firm would only be profitable if a diversified intermediate-goods sector provides low-cost specialized inputs, but a diversified intermediate-goods sector would only be profitable in the presence of strong demand from the capital-intensive firm. Unlike Murphy et al. (1989), the problem is not related to a paucity of domestic demand, but to the weakness of the intermediate-goods sector. Capital accumulation, which transfers resources to the capital-intensive firm and hence increases the linkages with the intermediate goods sector, is essential for achieving industrialization.

Using similar logic, Rodrik (1996) proposed an open-economy model in which middle-income countries that are poorly endowed with physical capital but possess a sufficient level of human capital could specialize in low or high-tech goods. Because of coordination failures provoked by non-tradable specialized inputs subject to IRS, multiple equilibria arise. The profitability of the high-tech sectors depends on the existence of a well-trained workforce. The existence of a well-trained workforce, the non-tradable specialized input in this model, hinges upon a strong demand for its services. To achieve a high-tech equilibrium level, governments could implement a high-wage policy, diminishing the relative profitability of labor-intensive sectors, thereby attracting industries based on the skills of the workforce rather than on its low-cost advantage.

Finally, Rada (2007) demonstrated the relationship between Kaldor-Verdoorn law and effective demand in structural change processes. Using a dual model with a capitalist and a traditional sector, in which the former operates under IRS whereas the latter does it with constant returns to scale (CRS), she shows how the level and composition of effective demand leads to multiple equilibria. A positive aggregate demand shock in the IRS sector, such as an exogenous rise in manufactured exports, provokes a transfer of resources to the capitalist modern sector, increasing output and TFP. By contrast, a negative aggregate demand shock in the IRS sector, like the one caused in Mexico by China's accession to the WTO in 2001, transfers resources to traditional sectors, igniting a deindustrialization process that decreases output and TFP. More generally, an aggregate demand increase (decrease) leads to an increase (decrease) in output and TFP via the Kaldor-Verdoorn effect. Moreover, Rada stressed how an increase in the modern-sector productivity, if not accompanied by a sufficient increase in output, may provoke a transfer of labor to the CRS sector; a modern-sector productivity increase could lead to a “jobless growth”. Macroeconomic policy should, henceforth, steer aggregate demand to IRS sectors and strengthen linkages.

The most comprehensive formulations we found are the “Rosenstein Rodan-Hirschman” models elaborated by Skott and Ros(1997) and Ros (2013) that we will derive in the rest of this section. They differ from Murphy et al. (1989) in making capital accumulation a source of external effects; from Rodríguez-Claire (1996) in incorporating Lewis' proposition of perfectly elastic labor supplies; from Rodrik (1993) in making explicit the function that the traditional sector plays in the development process; and from Rada (2007) in focusing on aggregate supply instead of aggregate demand constraints to economic growth. They stress the importance of capital deepening in modernizing an economy plagued with surplus labor where, borrowing a Lewis expression, “islands” of modern capital-intensive firms thrive in a “sea” of subsistence labor-intensive ones. Although these models use a neoclassical production function, and we know since the Cambridge controversy that there are logical aggregation problems with their notion of capital, they are inscribed in the structuralist tradition. They analyze the interaction between modern and traditional sectors and abandon important assumptions of the neoclassical paradigm such as perfect competition or CRS. Thanks to these modifications, they arrive at multiple equilibria, opening the door for Pareto-improving public interventions. Using neoclassical theoretical tools, it is possible to build models in which the State must play an active role in promoting the structural change of traditional economies.

Three sectors interact. First, there is a traditional competitive sector, which operates with CRS technologies and uses labor (L) according to the following production function:

This sector transforms one unit of labor into one unit of output. Second, there is an intermediate-goods sector that also uses labor as its only factor but operates on a monopolistic-competitive market structure and is subject to IRS.

IRS are represented by the parameter u. Finally, there is a modern-competitive sector, operating with CRS technology, which uses capital (K) and a set of intermediate goods (I) according to a traditional Cobb-Douglas production function:

As in Rodrik (1993), the I

sector has a CES technology

Where Pm and PI , the prices of the modern and intermediate goods sector, are considered parametric values by the modern-sector firms. The first-order condition for profits maximization is thus:

The second-order condition is automatically satisfied since (3) is strictly concave. Profits in the M sector, as is evident from (5), are a positive function of the variety of domestically produced intermediate-goods n. This “love for variety” effect, widely studied by Rodríguez-Claire (1996), leads to IRS. Solving (5) for I we get:

With PI = nPi under the assumption that the prices charged by different intermediate goods firms are equal pi = pj . As the equation (6) shows, I* is an increasing function of K and Pm and a decreasing function of PI . If there was only one firm in this sector, the I producer would face an intertemporal choice, since maximizing its profits by increasing PI would imply diminishing πm and hence the demand of its own product. However, when many producers are considered, as this model does, the intertemporal link is weakened. Operating on a monopolist-competitive market structure, firms in the I sector face a downward sloping demand curve given by the following function:

Where θ > 1 is the elasticity of demand and D

represents a position parameter. For many n, θ is

approximated by

Where we use the equilibrium condition for

From which we can solve for the i firm price. In this sector, firms have market power, so they can add a profit margin (1 + z) to the marginal cost function just derived. The price of the i firm, henceforth, can be stated as follows:

In which (1 + z) is equal to the elasticity of demand

On the other hand, by solving I from the i firm supply function we obtain:

Finally, substituting (11) in (12) and solving for I we get:

For simplifying equation (13), we make

Where the stability condition implies that f > 0. This expression allows the derivation of the short-term equilibrium schedule. To this end, we must recognize that total employment is equal to the sum of people employed in the traditional and in the intermediate-goods sectors L = Ls + LI . Moreover, LI is derived from the demand of the intermediate-good sector:

Under the assumption Ii

= Ij

. When the traditional sector exists, the short-term equilibrium locus would

be equal to PM

= w which, for the sake of simplicity, are equated to 1. Since the

traditional and the modern sectors produce the same good, the former provides a

perfectly elastic supply of labor at a constant real wage. However, when the economy

reaches Lewis' turning point, that is, when the traditional sector disappears

because labor has been absorbed in the intermediate goods sector, we must solve

From where, using the fact that L = L1+u

, we can solve for

Equation (17) represents the real wage needed for maintaining equilibrium in the labor market. To close the model, we need to analyze changes in the capital stock. To this end, we postulate a profit function for the modern sector that incorporates K as a variable.

Now, we differentiate the profit function with respect to K:

Solving (19) for r and substituting (16) into this expression yields:

After some algebra:

As equation (21) entails, the profit

rate (r) is an increasing function of the capital stock. A higher

K translates into a higher I which, due to

IRS, are produced under decreasing marginal costs. Now, for obtaining the long-term

equilibrium locus, we will use Solow's steady-state condition. Solow stated that

capital per effective worker grows at a constant rate when there is an equality

between the investment rate (Sπ

r), the capital stock depreciation rate (δ), and

the increase in population and technological change. For analytical convenience,

population growth and technological change are assumed away. Henceforth, capital

accumulation per effective worker is determined by

Equation (22) represents the real wage needed for maintaining the capital-stock constant. Graphically:

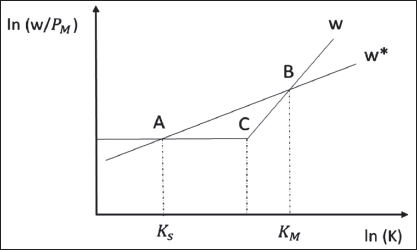

The w locus shows all the points where the labor market clears. It has a horizontal segment since, if there is a labor surplus in the traditional sector, real wages remain constant. As capital accumulation proceeds, the pool of labor surpluses is exhausted, so real wages rise. The w* curve, on its hand, shows the real wages that keep the capital stock constant. It has a positive slope since, due to IRS, a larger capital stock must be accompanied by higher real wages to maintain the equality between marginal profits and costs. Multiple equilibria arise. There is a low-income equilibrium, represented by point A, where the capital stock is low. In this scenario, profits of the M sector are low, for I goods are produced at high costs. Conversely, there is a high-income equilibrium, represented by point B, where wages and profits are high because I goods are produced at low costs. Point C denotes Lewis' turning point where labor has been absorbed in the intermediate goods sector and real wages rise with capital accumulation. When point C is surpassed, the system tends to point B.

The conclusions are straightforward: for attaining a high-income equilibrium, governments could implement policies for increasing the production of I directly or stimulate the production of M by increasing I indirectly. Why is this model relevant to the Mexican case? Because we claim that the Mexican economy is in a development trap (point A in the graph) in which the levels of capital per worker are not enough for absorbing the workers located in traditional sectors. The Pacto por México reforms tried to address this problem from a microeconomic perspective. However, as we will see in the next section, they failed to accelerate capital accumulation.

III. A hypothesis on why the Pacto por México structural reforms have not delivered their expected results

The Pacto por México second-generation reforms sought to foster capital accumulation and improve allocative efficiency. They were expected to turn the goods markets more competitive, provoking a reduction in the prices of essential inputs such as electricity, gasoline, financial products, or telecommunications. The conjunction of the education and labor reforms, moreover, would enhance human capital, diminish the costs of hiring formal workers, and eliminate incentives for informality. Together, they would increase the economy's productivity and competitiveness by fostering the efficiency of I, deriving into lower prices thanks to IRS and lower mark-ups.

By reducing PI , these reforms would, ceteris paribus, increase πM . Consequently, capital accumulation would be stimulated in modern firms that intensively use these non-tradable goods and services, absorbing workers located in rural, informal, and other low productivity activities. So, if these long-awaited reforms have been finally enacted, why has the Mexican economy not grown as expected?

We claim that the ineffectiveness of these structural reforms boils down to one factor: even though they increased investment in some sectors such as energy, the share of investment as a percentage of GDP has marginally decreased (see Table 7 below). In simple words, they did not generate the critical mass of investment for making the economy “take-off” and provoke a productivity-increasing reallocation of resources.

Table 6 Growth Performance and Gross Fixed Capital Formation / GDP for selected countries

| Country/Year | Average

annual GDP Growth |

Variation | Average Investment/GDP |

Variation |

| China | ||||

| 1956-1978 | 3.8 | 0 | 10.05 | 0 |

| 1979-2017 | 7.31 | 92 | 28 | 178 |

| Japan | ||||

| 1956-1992 | 6.49 | 0 | 34.7 | 0 |

| 1993-2017 | 0.92 | -85.85 | 24.44 | -29.56 |

| Korea | ||||

| 1955-1965 | -4.9 | 0 | 14.72 | 0 |

| 1966-1997 | 9.31 | 2900 | 35.59 | 141.7 |

| 1998-2017 | 4 | -57 | 33.67 | -5.3 |

| Singapore | ||||

| 1965-1997 | 9.06 | 0 | 54.93 | 0 |

| 1998-2017 | 4.97 | -45.14 | 35.59 | -35.2 |

Source: Penn World Tables.

Table 7 Mexico Investment Behavior (1950-2017)

| Year | Average

annual GDP Growth |

Variation | Average GFCF/GDP |

Variation | Public Investment/GDP | Variation | Private Investment/GDP |

Variation |

| 1950-1970 | 6.51 | 0 | 20.42 | 0 | 5.77 | 0.00 | 14.65 | 0 |

| 1971-1981 | 6.3 | 4.45 | 23.1 | 13 | 8.22 | 42.46 | 14.88 | 1.56 |

| 1982-1989 | 0.61 | -91.1 | 13.03 | -22 | 6.61 | -19.59 | 11.42 | -23.25 |

| 1990-2012 | 2.77 | 354 | 19.85 | 10 | 4.66 | -30.00 | 15.19 | 33 |

| 2012-2018 | 2.68 | -3.2 | 19.75 | -0.50 | 4.38 | -6.00 | 15.37 | 1.18 |

Source: Own elaboration with information from Penn World Tables, Inegi Estadísticas Históricas de México (2014), and INEGI Banco de Información Económica.

Notes: Data for GFCF/GDP were obtained from Pen World Tables. Data for Public investment/GDP was obtained from Estadísticas Históricas Inegi 2014.

To calculate private investment/GDP we substracted GFCF/GDP from public investment/GDP.

To understand this phenomenon, we must recognize, first, that high-growth periods are usually determined by accelerated capital deepening. To illustrate this point, we selected some countries that have registered very high growth rates for a considerable time and divided data into high and low growth rate periods.

We will point out China's and Japan's cases. From 1956 to 1978, before the market-oriented reform process began with Deng Xiaoping's access to power, the average GFCF in China was 15% of GDP, and the average output growth was 3.8%. By contrast, between 1978 and 2017, GFCF increased to an average of 28% and output growth to 7.31%. We can confirm the same results in Japan. From 1956 to 1992, when Japan became an industrial powerhouse, GFCF as a percentage of GDP was 34.7%, and GDP expanded at an average annual rate of 6.49%. In contrast, after the 1992 debt-deflation crisis, the average GFCF/GDP diminished to 24.4%, and GDP growth fell to 0.92%. Table 7 shows how GFCF has evolved in Mexico.

From 1950 to 1970, a period that encompasses the so-called “Desarrollo Estabilizador”, the Mexican economy grew at an average rate of 6.51%, with a mean GFCF/GDP of 20.42%. During these years, Mexico transformed into an urban country and consolidated a relatively strong import-substitution industry of intermediate and durable consumption goods. From 1971 to 1981, known as the populist era, the average GFCF/GDP increased 13%, reaching 23.1%. This stimulated GDP growth, with an average of 6.8% per year, the highest registered thus far. However, these high growth rates were attained at the cost of generating twin macroeconomic imbalances, which in conjunction with adverse external shocks -specifically Paul Volcker's contractionary monetary policy and the subsequent decline in the international prices of oil- resulted in the 1982 foreign debt crisis. The “lost decade” that ensued provoked a collapse of the levels of both public (-19.5%) and private (-15.1%) investment. From 1982 to 1989, mean output growth was only 0.6%, and the average GFCF/GDP fell to 18%. Although the renegotiation of the foreign debt with the Brady Plan and the consolidation of the integration process with the enactment of Nafta resumed capital accumulation and output growth, these variables have not reached the pre-external debt crisis levels. From 1990 to 2012, the mean GFCF/GDP was 19.85%, and GDP grew at an average rate of 2.77%. Did this situation change with the Pacto por México?

The short answer is no, but it is worthwhile emphasizing some points. First, from 2012 to 2018, public investment as a share of GDP was 46.7% lower than in 1971-1981. Public investment has been on a downward trend since the post-1982 fiscal adjustment and, in 2019, it registered the lowest level in sixty years (2.7% of GDP). Second, private investment did not increase as expected. Despite the first-generation reforms, in the period 1990 to 2012, the average GFCF/GDP was only slightly higher than from 1950 to 1970. Third, the Pacto por México reforms have not led to a higher level of investment. The ratio of GFCF/GDP, for instance, was 3.2% lower from 2012 to 2018 than in the previous period. Albeit private investment surged from 15.17 to 15.39 % of GDP, public investment declined from 4.66 to 4.38%, causing a marginal fall in the overall level of investment from 19.85 to 19.75%. Why did the levels of investment not increase despite this comprehensive package of market-oriented reforms? We advance three interrelated explanations:

1. Mexico's public revenues and expenditures are low by international standards. In 2019, public revenues as a share of GDP (16.5) were below the average of the OECD (33.8) and Latin America (23). When considering highly developed countries, such as Sweden (42.9) or Norway (39.9), this lack of public income becomes dramatic. In terms of public expenditures, on the other side of the coin, Mexico (20) falls behind the average of the OECD (29) and Latin America (28).

Table 8 International Comparison of Public Revenues and Expenditures (Percentage of GDP, 2019)

| Region | Public Revenues | Public

Expenditures of Central Government |

| Mexico | 16.5 | 20 |

| Latin America | 23 | 28 |

| OECD | 33.8 | 29 |

Source: For public revenues OECD's Global Revenue Database. For public expenditures International Monetary Fund.

Notes: Public revenues include invome taxes, property taxes, sales taxes, and contributions to social security.

The country has low expenditures on social development and, as we have seen, on public investment. This paucity of public expenditures in social development has negative effects on the country's human capital (the population's levels of education and health), while the low levels of public investment increase firms' production, distribution, and transaction costs. In both cases, private-sector profits are negatively affected.

2. The linkages between modern and traditional sectors are weak or non-existent, which becomes obvious when analyzing the relationships between the exporting and the intermediate-goods sectors. The reform process had among its objectives to benefit from Mexico's vicinity with the United States to transform it into an export-led country; the liberalization of commercial and financial accounts, along with macroeconomic stability and the strengthening of rule of law, would attract FDI and transform the country into a technologically sophisticated manufacturing exporter. The growth of manufactured exports has been, indeed, one of the achievements of the structural change process.

Table 9 Mexico's Exports by Economic Sector (US million dollars)

| 1980 | 1985 | 1990 | 1995 | 2000 | 2005 | 2010 | 2015 | 2018 | |

|---|---|---|---|---|---|---|---|---|---|

| Total Merchandise | 18,031 | 26,757 | 40,711 | 79,542 | 166,367 | 214,207 | 298,305 | 380,550 | 450,713 |

| Agricultural Products | 12.66% | 7.40% | 8.51% | 9.04% | 5.47% | 5.86% | 6.30% | 7.19% | 7.80% |

| Fuel and Mining Products | 62.77% | 52.84% | 27.91% | 13.13% | 10.98% | 16.71% | 16.69% | 8.44% | 9.32% |

| Manufactures | 24,34% | 39.75% | 62,04% | 77,49% | 83,34% | 77.03% | 74,53% | 81.93% | 80,45% |

Source: Own elaboration with World Trade Organization data.

Total exports surged from around 18 billion dollars in 1980 to more than 450 billion in 2018. The composition of exports, moreover, changed dramatically. In 1980, fuel and mining products were equivalent to 62.7% of all exports, while manufactured products only amounted to 24.3%. In 2018, manufactured exports represented 80.4% of total exports, whereas fuel and mining products only 9.3%. The spectacular increase in exports raised the importance of the tradable goods sector as a driver of economic growth. However, due to the absence of internal linkages, the local value-added of exports is low. Several studies have shown how the opening of external accounts led to an increase in the income elasticity of imports and balance of payments constraints Moreno-Brid (1999); Blecker and Ibarra (2013); Romero and Rodríguez (2020). Perhaps not surprisingly, Mexico's internal value-added of exports is more than 20 points below the averages of the OECD, the European Union, and the G-20.

The high dependence on imports reduces the value-added multiplier effects of an expansion of exports, from a demand perspective, and hinders the achievement of economies of scale and scope in the intermediate-goods sector, from a supply one. The combination of an export success with a mediocre output growth Gómez et al. (2018) is not paradoxical, then. To increase local value-added, Mexico would need to implement a reinvigorated industrial policy that provides incentives for boosting investments in strategic and complementary sectors, along the lines of policy recommendations advanced by authors such as Moreno-Brid (2013). An active industrial policy is essential for creating new economic sectors and allowing the existing ones to reach IRS. The Pacto por México, which assumes that market forces will automatically solve this coordination problem, did not even consider industrial policies as part of its neoliberal structural reforms package.

Finally, the monetary policy framework, based on inflation targeting, is provoking a recurrent appreciation of the real exchange rate, diminishing the profitability of exporting and intermediate goods sectors. Because of the high imported content of Mexico's production, Banco de México has a “fear to float”, and it is using the real exchange rate as an anchor to control costs and inflation expectations. This monetary policy taxes exporting activities and incentivizes importing ones. By increasing the profitability of exporting activities, a competitive real exchange rate would stimulate the expansion of modern sectors, reallocating recourses to IRS activities Razmi et al. (2011). A wide recent empirical study found that a sustained undervaluation of the real exchange rate typically promotes an increase in GDP, investment, and exports, as well as a decrease in the relative size of the service sector Martins and Razmi (2022). These are exactly the changes that the Mexican economy needs.

In sum, since the outset of the neoliberal structural change process, the country was subjected to international competition without having the conditions to succeed. As the East Asia experience demonstrates, a competitive real exchange rate, the accumulation of human and physical capital, as well as an active industrial policy are essential to insert virtuously into global markets. Missing these elements, modern sectors with IRS will not find enough profitability to expand and absorb labor surpluses. The Pacto por México reforms, the ultimate phase of this neoliberal project, did not address these constraints; insofar as we do not implement complementary macro-economic policies, which entail strengthening the economic role of the State, Mexico will remain in the slow growth and high-income inequality trap of the last four decades, with all its negative social repercussions Ros (2013).

Conclusions

Mexico is a paradigmatic example of a dual economy. Since the 1980s, the bet has been to transform its productive structure by promoting competition through the liberalization of external trade and finance. Efforts have been concentrated on setting the framework conditions -macroeconomic stability, an educated workforce, a competitive environment, strengthening the rule of law- for deepening the integration process. The Pacto por Mexico reforms enacted almost ten years ago are just the last endeavor on this neoliberal path. Until now, however, this 40 year strategy has yielded negative results. Although Mexico became a leading manufacturing exporter, the transformative capacity of its modern sectors has been limited, while the opening of external accounts increased the share of resources allocated to low productivity activities; local value-chains were destroyed in a “creative destruction” process that “liberated” resources in the Marxian conception of the term without fully absorbing them in modern activities.

Drawing on the CDT lessons, in this paper we advanced a hypothesis for explaining this phenomenon: due to a lack of complementary policies, the structural reforms have not increased the rate of capital accumulation enough to modernize the productive structure of the country. It is essential to ask whether the structural change process is truncated not because Mexico has not implemented the umpteenth microeconomic reform -as the OECD recurrently claims- or has been unable to guarantee the rule of law, but because some relevant macroeconomic reforms for complementing the integration strategy are missing. For instance, it could be the case that public expenditures are too low for supplying adequate social and physical infrastructure, that a modern industrial policy for fostering firms' competitiveness is absent, or that the inflation-targeting monetary policy regime provokes a harmful real exchange rate appreciation. These elements are certainly reducing the profitability of the modern sectors, explaining the paucity of investments and a feedback process between economic stagnation and the consequent growth of informal, traditional, and subsistence activities. Given Mexico's demographic trends, specifically the demographic bonus that is being wasted, it is imperative to accelerate the rate of capital accumulation, so every young person can have access to remunerative work in socially productive activities, instead of surviving through self-employment in the informal sector or illegal activities.

It cannot be stressed enought that this does not mean that we should not work on strengthening our fundamentals. Education is lacking at all levels, our weak rule of law provokes uncertainty and a systematic misallocation of resources, our innovative capabilities are poor, and our low-quality institutional framework generates perverse incentives and rises transaction costs. However, as the experience of the last 40 years has shown, improving these factors is a necessary but not a sufficient condition for achieving inclusive growth; there is no point in training more doctors, engineers, or scientists if they are going to end up working as Uber drivers due to a lack of appropriate job opportunities. The country's leaders should concentrate on designing a new development agenda that fosters a process of structural change characterized by the absorption of labor surpluses into productive activities. Mexico's social, economic, and political future depends on it.