Servicios Personalizados

Revista

Articulo

Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Accesos

Accesos

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkEconomía: teoría y práctica

versión On-line ISSN 2448-7481versión impresa ISSN 0188-3380

Econ: teor. práct no.36 México ene./jun. 2012

Artículos

Financial globalization and financial development in transition countries*

Edgar Demetrio Tovar García*

* National Research University "Higher School of Economics", Moscow, Russia, beno09@yahoo.com y veno09@hotmail.com.

* Fecha de recepción: 25/07/2012.

Fecha de aceptación final: 20/02/2011.

ABSTRACT

This paper examines the impact of financial globalization on financial development in transition countries. An empirical test is elaborated with new indicators of financial globalization and financial development, closer to theoretical and conceptual framework. On the basis of Blundell and Bond (1998) a dynamic panel data model is employed. The principal results suggest, in general, that financial globalization has a positive and significant relationship with the process of growth of the financial system, but not with the process of development, that is to say, without a better performance of basic financial functions.

Key words: financial globalization, financial development, transition countries and dynamic panel data.

Classification JEL: F39; G19; O16; P20.

RESUMEN

Este artículo examina el efecto de la globalización financiera sobre el desarrollo financiero en los países en transición. Se elabora una prueba empírica con nuevos indicadores de globalización financiera y desarrollo financiero más cercanos al marco teórico y conceptual. Con base en Blundell y Bond (1998) se emplea un modelo con datos de panel dinámico. Los principales resultados sugieren, en general, que la globalización financiera tiene una relación positiva y significativa con el proceso de crecimiento del sistema financiero, pero no con el proceso de desarrollo, es decir, sin un mejor desempeño de las funciones financieras básicas.

Palabras clave: globalización financiera, desarrollo financiero, países en transición y panel de datos dinámico.

Clasificación JEL: F39; G19; O16; P20.

INTRODUCTION

The international flows of capital augmented notably in the last three decades, particularly, after 1987 most of the countries liberated their capital account. Transition countries, especially members of European Union and accession candidates, had progressed significantly into the financial globalization, and for this purpose their financial systems are key factors to get benefits and to withstand the risks associated with the globalization. Under these conditions, the literature is motivated by the question: does financial globalization cause financial development?

Notwithstanding financial crises, economic literature argues theoretically and empirically that globalization promotes financial development because it allows to financial systems a better performance in their basic functions. Financial globalization reduces the power of interest groups (who are opposed to the development of the financial system) and it permits the adaptation of the institutional structure, in favor of the best practices and financial innovations.

Financial development favors larger rates of growth and economic development, because it has an influence over saving decisions and investment (Levine, 2005; Ang, 2008). In consequence, it is relevant to know what determines financial development. There is a body of research that examines financial globalization shaping financial development; this nexus in transition countries is the main topic of this paper.

It is worth noticing that financial system is a channel through which financial globalization can influence growth and economic development, therefore, that relationship deserves direct theoretical, empirical and analytical attention.

The paper is as follows: Section 1 discusses shortly the theoretical relationship between financial globalization and financial development, with special attention to impacts on basic financial functions. Also, it describes previous empirical studies and their main results. Section 2 specifies the econometric model, a dynamic panel data based on Blundell and Bond (1998) and describes the data sets (sample of transition countries). Section 3 reports and discusses the econometric results. Finally, it presents conclusions.

1. FINANCIAL DEVELOPMENT AND GLOBALIZATION

For mainstream economists there are no doubts about the potential advantages of financial globalization. As Obstfeld (2008: 2) points out that "over the longer term, an internationally open financial system is likely to be more competitive, transparent, and efficient than a closed one". Free capital mobility implies an efficient allocation of resources on a global scale.1

But, growth economics rates in the last 30 years had been smaller than in the 60s and 70s. Prasad, Rajan and Subramanian (2007) did not find evidence that an increase in foreign capital inflows implies a quicker economic growth. Also, the financial uncertainty is a characteristic of the current globalization. The underdeveloped countries, especially, suffered financial crisis: Mexico in 1994-1995, Asia in 1997, Russia in 1998, Brazil in 1998-1999, Argentina in 2000-2001 and recently the United States in 2007-2008 and Europe in 2011.

It is obvious that financial crises, and their easy infection, are the main warning signals against financial globalization. But, Bailliu (2000), Eichengreen and Leblang (2003) and Bekaert, Harvey and Lundblad (2005) argue that the impact on economic development of financial globalization will be positive if countries have a developed and good regulated financial system. Under these conditions, the allocation of capital will be efficient and the inCIDEnce of financial crises will be smaller.

A financial system is formed by organizations (banks, central bank and other financial intermediaries), a financial market and an institutional framework (formal and informal institutions; laws, rules, regulations, customs, culture, etc.). According to the classification of Levine (1997 and 2005), a financial system has five basic functions: 1) To produce information ex ante about possible investments and allocate capital, 2) To monitor investments and exert corporate governance after providing funds, 3) To facilitate the trading, diversification, and management of risk, 4) To mobilize and pool savings, and 5) To ease the exchange of goods and services. A better performance of the functions indicates a larger financial development.

In the world there are financial systems more developed than others, that is to say, financial systems that perform basic functions better (more efficiently) than others, and thanks to financial globalization it is possible to import a developed financial system, through a process of catching up.

Rajan and Zingales (2003) support the hypothesis that financial systems are not developed because there are interest groups (incumbents) that oppose financial development because it harms their power and benefits. But, financial and trade openness weaken these interest groups, because the external agents press the national financial system to perform better their basic functions (through competition). Besides, when an economic agent invests in another country it is supposed that he also transfers financial technology and innovations. Financial globalization chooses the most productive technology (Saint Paul, 1992 as cited in De Gregorio, 1999).

Analyzing financial globalization and each one of the basic functions that a financial system should perform to get a higher level of financial development, it is feasible to hope: First, financial globalization will destroy private and privileged information in the financial markets of the interest groups, because the financial system (their organizations, institutions and the own market) will spread all available information, as a result of confrontation and new demands of the external economic agents, who are not subordinated to interest groups. Specifically, the participation of external economic agents generates competition among them and with local agents and in that way it is achievable to produce more truthful and deeper information about domestic financial market conditions. On the contrary, if external economic agents are interested in collusion and cooperation with domestic interest groups, the financial system will not be able to give all available information to all agents.

Second, with financial globalization it is feasible that the best practices and methods of financial supervision spread around the world and improve corporate governance. Morck and Steier (2005) point out that, contrary to the United States, most of the capitalist countries have corporations with a pyramidal organization that belong to the richest families, therefore, the allocation of capital responds to these interest groups and their arrangements with the state. But, the arrival of external economic agents will confront bad decisions in allocation of capital of the interest groups, assessing firms and monitoring managers, and then they will improve corporate governance (Levine, 2002). On the contrary, Shleifer and Vishny (1986) argue that the liberalization can weaken corporate control, because it reduces the incentives of shareholders, thanks to more liquidity, to supervise borrowers and managers.

Third, financial globalization favors risk diversification. This is obvious on a global scale, because domestic economic agents can share risks with foreign agents in domestic and foreign financial markets. This way, in a peak time a country can lend to the foreigner, and in a recession, it can borrow, which helps to mitigate the impacts up and down on the income level, and in consequence, also in consumption and investment. obstfeld (1994) argues that international risk diversification allows the world economy to move from a portfolio with low risk and low returns to one with higher risk and higher returns. In addition, financial contracts that favor risk diversification will spread in all countries. on the contrary, if agents prefer domestic assets, nontradable goods and international trade has high transaction costs, the incentives to international diversification of risk could decrease. Also, if international financial markets are incomplete, with the risk of a unstable exchange rate and expropriations, there is not any insurance against all future contingencies (Kose, Prasad and Terrones, 2007).

Fourth, if capitals flow freely around the world, it will favor mobilization and pooling of savings on a global scale. Domestic savings will be able to seek foreign financial markets, looking for better returns, and the domestic financial market will have to improve methods to pool savings, as a result of international competition. Furthermore, it is supposed that external saving does not substitute domestic saving. On the contrary, if financial globalization offers better protection against uncertainty, this may in fact lower the needs to save for the future, which might lead to a better stock market without an increase in savings (Devereux and Smith, 1994, as cited in Naceur Ghazouani and omran 2008: 677).

Fifth, financial globalization reduces international transaction costs and it favors a global relationship between financial and real sector. In others words, globalization facilitates exchanges in the real economy on a global scale.

1.1 Analysis of the previous empirical evidence

The financial globalization-financial development nexus has specially been approached in empirical studies. Levine and Zervos (1998), De Gregorio (1999) and Klein and Olivei (2001) were the first to examine this nexus, shortly after Chinn and Ito (2002 and 2006) discussed the nexus with the introduction of institutional variables. Later on, Law and Demetriades (2006), Huang W. (2006), Calderón and Kubota (2009), Law (2009) and Baltagi, Demetriades and Law (2009) extended the literature, especially they used econometrics models with a sample of developed and underdeveloped countries.

There are few case studies or methodologies applied to special groups of countries, Naceur et al. (2008) analyzed a sample of 11 countries of the Middle East and North Africa region, Ito (2006) put special attention on 15 Asian countries, Ahn (2008) analyzed Korea, and Law (2008) studied Malaysia.

Financial development, as a dependent variable, has been approached principally with indicators of credit (liquid liabilities over GDP and private credit over GDP) and with indicators of the stock market (stock market capitalization, stock market total value as a ratio of GDP, and stock market turnover).

Rarely, literature uses the neologism "financial globalization". The studies especially talk about financial openness like an explanatory variable of financial development, and the main indicators to approach this variable are based upon the IMF's categorical enumeration reported in Annual Report on Exchange Arrangements and Exchange Restrictions (AREAER). Few studies employ the international flows of capital or some measure of financial integration.

The econometric models used to evaluate the financial globalization-financial development nexus have improved with the time. In the beginning, studies employed more graphic analysis and least squares (LS), later models with panel data (DP) and recently dynamic panel data and generalized method of moments (GMM). The regressions are controlled with income level, inflation and trade openness. Chinn and Ito (2002) were the first to take account of institutional variables, according to La Porta, Lopez-of-Silanes, Shleifer and Vishny (1998), who highlight that institutional framework is an important factor to explain financial development.

In general, the results of the empirical tests suggest a positive effect of financial globalization on financial development, especially in developed countries. In the case of underdeveloped countries the evidence is mixed, but the positive effect is found in samples of emerging economies. In addition, the results, after inclusion of institutional variables, suggest that the impact of financial globalization on financial development will be positive if a country has a good quality of institutional structure.

Buiter and Taci (2003) employed a graphic analysis and least squares to investigate transition countries. They found a positive relationship between legal transition and private sector credit (% of GDP), progress in banking sector reform, share of foreign bank ownership (% of total assets), privatization and stock market capitalization (% of GDP). They concluded that "more than ten years of transition have brought significant progress in restructuring and developing the financial sector in most (but not all) transition countries" (p. 34). But, in times of international capital flows, the challenges are related to institutional framework and corporate governance.2

2. EMPIRICAL SPECIFICATION

Recently, the main econometric methodology to study the financial globalization - financial development nexus is the dynamic GMM estimator developed by Arellano and Bond (1991), but if the autoregressive parameter is moderately large (around 1) and the number of time series observations is moderately small, the estimators obtained have bias and poor precision. The sample of transition countries has not small time series observations (see section 3.2), but the autoregressive parameters obtained by Arellano and Bond (1991) showed values between 0.12 and 0.98.3 Therefore, this investigation employed the methodology developed by Blundell and Bond (1998), they review the importance of using the initial condition in generating efficient estimators of the dynamic panel data model.

The model has different levels, it allows lagged values of a dependent variable to enter as regressors, and it provides a better control of endogeneity for all explanatory variables because it use lags of variables like instruments (in first differences and levels).4 In addition, the explanatory variables are entered in logarithms5 and with a lag to prevent simultaneity and reverse causality (see equation 1).

Where FD is a measure of financial development, FG is a measure of financial globalization and X is a vector of control variables: log per capita GDP (constant 2 000 US$) (GDP), the inflation rate (INFLA) and log trade openness (XM) measured as the ratio of the sum of exports and imports to GDP.7 D1 is a dummy variable: Commonwealth of Independent States (CIS) countries (1) and otherwise (0).

The fundamental interesting hypothesis is that financial development depends positively upon the level of financial globalization. Also, financial development depends positively upon a series of control variables (except the inflation rate).

2.1 Some notes about panel data

Chinn and Ito (2002: 4-5 and 2006) argue that it is difficult to control secular trends in financial deepening in the context of the panel regression in levels with annual frequency, due to the large cyclical variations in the financial deepening variables, along with trending behavior of the explanatory variables. Their solution is to use the average annual growth rate over a five year period; in order to avoid problems of endogeneity associated with short term cyclical effects (other studies used the same strategy).

Nevertheless, this study uses a panel data with annual frequency (W. Huang, 2006, Naceur et al. 2008, calderon and Kubota, 2009, and Baltagi et al. 2009 also used annual frequency), in order to use all available information. Furthermore, it is feasible to think that the recurrent variations in the financial markets behave according to random walks model, and if there are bubbles, they are rational and a consequence of the normal cycle of business (Fama, 1965 and 1991), and financial globalization has to move according to these cycles. In other words, the cycles are a part of interest of this analysis.

It is worth noticing that financial markets, interest rates and international capital flows, move quickly every day (or at least in the short term), then we find daily adjustments. Therefore, data of annual frequency that correspond to a daily behavior should be enough to mitigate the abrupt movements in relation to the explanatory variables.8

2.2 Data, measurement and sources

The data are drawn from the World Bank's World Development Indicators (WDI) 2005 and 2008, and the databases associated with Beck, Demirgüç-Kunt and Levine (2009). The analysis is based upon data recorded at an annual frequency, over the 1995-2008 period, covering 26 transition countries. Details are reported in Appendix, table a3 resumes descriptive statistics, table A4 shows a correlation matrix and figure a1 shows a line graphics of means.

2.2.1 Indicators of financial development

In the literature, the main indicators to approach financial development are measures of credit and stock market, other financial intermediaries such as pension funds and insurance companies are underestimated and the informal financial sector is omitted.

Levine (2005) points out that the main problem in empirical studies are the proxies for financial development, they do not frequently measure very accurately the concepts emerging from theory. Empirically, it has been showed that high levels in ratio m2/GDP or credit/GDP do not necessarily imply a developed financial system (Ang, 2008).

Under the conditions described above, this investigation uses six measures of financial growth, three of them approach credit and size of the financial system: 1) liquid liabilities over GDP (LLY), 2) private credit by deposit money banks and other financial institutions over GDP (PCFS) and, 3) financial system deposits over GDP (FSD). In the appendix table a3 shows that the mean and the median of these indicators are close, and have a small standard deviation, so the majority of transition countries have similar rates. Hungary, Bulgaria, Croatia, and Slovak Republic have high rates, but Czech Republic has the best performance: 0.66 (LLY), 0.47 (PCFS) and 0.58 (FSD), just to compare, Russia has 0.25, 0.17 and 0.18, and USA has 0.67, 1.71 and 0.65, respectively (means of the same period, 1995-2008).

Other three measures are associated with the stock market: 1) stock market capitalization over GDP (STMK), 2) stock market total value traded over GDP (STTV) and, 3) stock market turnover ratio (STTR). Transition countries have dissimilar rates, the means and the medians are substantially different, and have a large standard deviation (see table 3). Small countries have not information (have not markets). Estonia, Poland, Hungary, and Czech Republic have the highest rates, although Russia has the best performance; 0.42 (STMK), 0.17 (STTV) and 0.32 (STTR), USA has 1.32, 2.09 and 1.51, respectively.9

In addition, the investigation uses other four measures to approach with more fidelity the financial development, because they approach four of the five basic functions of the financial system.10 The first of them is bank concentration (Informa), the assets of the three largest banks as a share of assets of all commercial banks.11 It is a measure of competition, and for mainstream economists, to more competition correspond prices that reflect all available information more faithfully.12 Therefore, this indicator approaches the first function of the financial system: provide more and better information.

Transition countries have similar rates of bank concentration, the mean is 0.70 and the standard deviation is 0.18 (see table A3), the best performance corresponds to Russia (0.35), but CIS countries usually have a high bank concentration (low competition), USA has 0.25.

This investigation uses deposit money bank assets over (deposit money + central) bank assets (Control), as a measure of the relative importance of commercial vis-à-vis the central bank. "Countries where deposit money banks have a larger role in financial intermediation than central banks can be considered as having higher levels of financial development" (Beck et al., 2009: 7). In addition, "it proxies the advantage of financial intermediaries in channelling savings to investment, monitoring firms, influencing corporate governance and undertaking risk management relative to the central bank" (Y. Huang, 2005: 13). Therefore, Control is a proxy of the second function of the financial system.

Transition countries have similar rates of Control, the mean is 0.83 and the standard deviation is 0.20 (see table A3), USA has a mean of 0.92. Estonia, Latvia, Lithuania, Serbia, Croatia, Poland, Slovak Republic and Czech Republic have a very good performance (close to 1).

The third function of the financial system, diversification of risk, is approached on the basis of studies that relate consumption growth variability to diversification of risk. Particularly, based on the studies of Prasad et al. (2003), Bekaert et al. (2006) and Kose et al. (2007), this investigation uses fluctuations in consumption over income. First, it is calculated the growth in real consumption for country i between year t and t+1, then it is defined the growth rate variability, as the standard deviation of the consumption growth rate estimated over five years. The same is calculated for GDP. The indicator RISK is consumption growth rate variability over GDP growth rate variability, if it is smaller implies a bigger diversification of risk. In this case, transition countries have a large variance, the mean is 2.06, the median is 1.33 and the standard deviation is 2.73 (see table A3). USA has a mean of 0.83 and Russia, Romania and Slovak Republic have rates close to 1.

The fourth indicator is bank credit over bank deposits (SAVE) that approaches the ability of banks in channeling savings of the society toward private sector. In consequence, it approaches the fourth function ofthe financial system: to mobilize and pool savings. The mean is 1.33 and the standard deviation is 2.20, so transition countries have dissimilar performance. USA has a mean of 0.79,13 Bosnia and Herzegovina has the largest rate (7.19), and other interesting countries are: Serbia (1.91), Estonia (1.54), Georgia (1.49), Latvia (1.41), Kazakhstan (1.38) and Russia (0.96).

2.2.2 Indicators of financial globalization

Literature usually approaches financial globalization with indicators of financial openness; many measures have been designed and it is difficult to find one that satisfies completely. The main discussion disputes if they are measures de facto (related with facts, for example capital flows) or measures de jure (related with policies, for example policies of capital controls).14 The main problem in samples of transition countries is that measures de jure are not available over a long period.15

Financial openness is an important characteristic of financial globalization, but the magnitude of international flows of capital is the basic reflection of it. Foreign currencies, stocks, bonds and other financial instruments are moving around the world like never before. This way, to measure financial globalization it is necessary to know how large those flows are. This investigation uses gross private capital flows as a ratio to GDP (FLOW), the sum of the absolute values of direct, portfolio, and other investment inflows and outflows recorded in the financial account of the balance of payments, excluding changes in the assets and liabilities of monetary authorities and general government. The mean of the transition countries is 18.7 and the standard deviation is 13.56, USA has a mean of 13.41,16 Azerbaijan 41.69, Estonia 35.81, Latvia 28.14, Hungary 24.67, Croatia 23.08 and Czech Republic 21.15.

Also, financial globalization implies a process of financial interdependence. If goods, services and factors of production can move freely among countries, then the market should balance their prices, reflecting the process of economic interdependence and integration. The price of capital is the interest rate and if capital can move freely among countries, their interest rates should converge (obstfeld and Taylor, 2003).17

To measure the convergence process, this study employs the variable integration of real interest rate (Intere) calculated subtracting the interest rate of a country less the reference interest rate (average of the g7, United States, Canada, England, Italy, France, Japan and Germany) in absolute terms. When this difference is closer to zero, the integration and financial globalization are larger.18 Transition countries have a mean of 9.54 and standard deviation of 13.13, Hungary has a very good integration (2.17), other interesting countries are: Czech Republic (2.37), Slovak Republic (3.25), Latvia (3.76), Croatia (4.27), Estonia (4.37), Poland (4.85) and Lithuania (5.56).

3. EMPIRICAL ANALYSIS AND ESTIMATION RESULTS

This paper contributes to the empirical literature in several ways. First, it approaches the financial globalization - financial development nexus using two indicators of financial globalization, each one measures a substantial part of globalization, instead of discussing if they are indicators defacto or de jure. Second, besides the typical measures of financial deepening, this paper uses four indicators to approach in a better way the basic functions of the financial system; therefore, they are better indicators of financial development. Finally, the econometric test includes a sample of transition countries that had been not used before.

Tables 1 and 2 summarize the main results of the estimation of the model [1], it was transformed to include the different measures of financial globalization. In columns there are dependent variables and in rows the explanatory variables. It is worth noticing that a dynamic panel is justified, because the dependent variables, as regressors, have statistical significant coefficients. Sargan tests do not manifest inconveniences with the used instruments, however, the second order serial correlation tests show problems in some cases, consequently those results must be treated with a fair amount of caution.19

3.1 International capital flows and financial development

Equation [2] shows the transformation of the model [1], to use as a measure of financial globalization the indicator FLOW (gross private capital flows).

Table 1 presents the main results. The capital flows enter with positive and statistically significant coefficient at the 10% and 5% level in the case of PCFS and DSF (indicators of credit and size of the financial system), and at the 1% level in the case of STTV and STTR, (indicators of growth of the stock market).

Flow enters with negative and statistically significant coefficient at the 1% level in the case of Control, the proxy variable of the second function of the financial system, consequently the capital flows are positive related with financial systems where the banks have a smaller role in financial intermediation than central banks, for that reason it is possible to expect a weak corporate governance in transition countries. on the other hand, FLoW mobilizes and pools savings (the coefficient is positive and statistically significant at the 5% level). There is not evidence of any significant relationship with the rest of indicators.

Trade openness (XM) does not have the predicted sign and significant coefficients in the case of STMK, STTV and Informa, it has positive and significant coefficient with Control, and it has no other significant relations. Therefore, the evidence suggests that trade openness does not favor the stock market if it is accompanied with bank concentration, and subsequently, with poor information about market conditions. But it encourages financial systems where banks have a larger role in financial intermediation than central banks.

The control variable GDP has few significant coefficients and INFLA enters with the predicted sign and significant coefficients in the majority of the cases. The dummy variable (D1) suggests that Commonwealth oflndependent States countries, in comparison with other transition countries, have financial systems where banks have a smaller role in financial intermediation than central banks and they do not mobilize and pool savings, although they have less bank concentration.

Buiter and Taci (2003) point out that, CIS countries developed many nonviable private banks in the early 1990s and they created reforms to sustain their interests and prevent the success of these banks. In addition, their stock exchanges are inactive, small, illiquid, and practically only obligations of the government are traded (Russia is clearly an exception) and the stock markets are dominated by a small number of large firms in such sectors as banking, electric power, natural resource and telecommunications. According to these facts, D1 has a negative sign and significant coefficient in the case of STTR.

3.2 Financial integration and financial development

Equation [3] shows the transformation of the model [1], to use as a measure of financial globalization the indicator Intere (integration of real interest rate).

Table 2 presents the main results. The measure of financial integration enters with predicted sign and statistically significant coefficients in the cases of PCFS, FSD and SAVE, that is to say, financial integration promotes credit and mobilizes and pools savings. Also, Intere does not have the predicted sign and statistically significant coefficient at the 1% level with Informa, therefore, financial integration encourages bank concentration (consequently with poor information about market conditions). Financial integration has no significant relationship with other indicators.

XM does not have the predicted sign and significant coefficients in the cases of FSD, STTV, Informa and save. For a second time, GDP has few significant coefficients and INFLA enters with the predicted sign and significant coefficients in the majority of the cases.

The dummy variable once more suggests that CIS countries, in comparison with other transition countries, have financial systems where banks have a smaller role in financial intermediation than central banks. Buiter and Taci (2003: 20) found that "the state still maintains a high degree of control over the banking sector, with the exception of Armenia, Kazakhstan and Tajikistan... The issue of government-directed lending is pervasive in these countries". But they do not favor bank concentration.

It is worth noticing, that CIS countries are characterized by macroeconomic and political instability, accompanied with corruption and limited legal system, with a low institutional development, with weak supervisory agencies and skills; obviously Russia is an exception in many aspects (see Buiter and Taci, 2003).

Both indicators of financial globalization show poor evidence in favor of the main hypothesis. Financial globalization has a positive effect only on SAVE (the fourth function of the financial system: to mobilize and pool savings), PCFS (private credit by deposit money banks and other financial institutions over GDP) and FSD (financial system deposits over GDP). Furthermore, the capital flows support the stock market (STTV and STTR). However, financial globalization has few and mixed effects on basic financial functions.

CONCLUSIONS

Theoretically, financial globalization can favor the growth and development of domestic financial systems, because the best financial practices can travel around the world through a process of catching up.

The empirical evidence about financial globalization-financial development nexus has grown considerably in the last ten years, however, indicators of financial development were not well related with the theory. This investigation, besides the typical indicators of credit and stock market, employed new indicators of financial development related to basic financial functions. The previous empirical results used samples with developed and underdeveloped countries, and found positive impacts on the financial development of financial globalization; but in samples of underdeveloped countries the evidence is not supported. In the same sense, the results ofthis investigation suggest that in transition countries it is not possible to find strong evidence of positive impacts, except for the credit market. At least, also it is not possible to argue a negative impact. The results are strong to a big range of alternative measures.

An interesting result is that trade openness favors financial systems where the banks have a larger role in financial intermediation than central banks. For that reason it is possible to expect strong corporate governance in transition countries. But also it encourages bank concentration; consequently it produces poor information about market conditions. This result supports the hypothesis of Hymer (1976) who argued that foreign investments arise from oligopolistic or monopolistic firms, which look for investments to conserve a non-competitive market structure. Furthermore, this is not a good evidence to support the hypothesis of Rajan and Zingales (2003), who argue that openness, either financial or trade, favors financial development.

Capital flows are the measure of financial globalization that enter better in the model; therefore, for policy makers in transition countries the advice is to carry out a strong integration and in the same time expand their policies of liberalization and facilitate the free flows of capital (their levels are lower than in developed countries), like previous empirical studies suggest. on the other hand, one could argue that it is possible to wait until these countries get a developed financial system, and later to facilitate the openness processes, that will enhance the financial development.

Future research must help to find other determinants of financial development in transition countries, and indicate which conditions are required to get positive impacts from financial globalization. Some investigations suggest that institutional framework is a key determinant (see La Porta et al. 1998), and so it will be necessary to elaborate more sophisticated institutional indicators, because the current measures do not change significantly in time and, by this reason they are not useful in empirical tests. Finally, it is necessary to point out that theoretical contribution about financial globalization-financial development nexus is supported on empirical studies, therefore, it is indispensable to develop a better theory.

REFERENCES

Ahn, Byung (2008), "Capital Flows and Effects on Financial Markets in Korea: Developments and Policy Responses", in Financial Globalisation and Emerging Market Capital Flows, Bank for International Settlements, 44: 305-320. [ Links ]

Ang, James (2008), "Survey of Recent Developments in the Literature of Finance and Growth", Journal of Economic Surveys 22: 536-576. [ Links ]

Arellano, Manuel and Stephen Bond (1991), "Some Tests of Specification for Panel Data: Monte Carlo Evidence and an Application to Employment Equations", The Review of Economic Studies 58: 277-297. [ Links ]

Arestis, Philip; Machiko Nissanke and Howard Stein (2005), "Finance and Development: Institutional and Policy Alternatives to Financial Liberalization", Eastern Economic Journal 31(2): 245-263. [ Links ]

Bailliu, Jeannine (2000), "Private Capital Flows, Financial Development, and Economic Growth in Developing Countries", Working Paper No. 15, Bank of Canada. [ Links ]

Baltagi, Badi, Panicos Demetriades and Siong Law (2009), "Financial Development and Openness: Evidence from Panel Data", Journal of Development Economics 89: 285-296. [ Links ]

Beck, Thorsten; Asli Demirgüç-Kunt and Ross Levine (2009), "Financial Institutions and Markets across Countries and over Time Data and Analysis", Policy Research Working Paper No. 4943. World Bank. [ Links ]

Bekaert, Geert, Campbell Harvey and Christian Lundblad (2006), "Growth Volatility and Equity Market Liberalization", Journal of International Money and Finance 25: 370-403. [ Links ]

----------, Campbell Harvey and Christian Lundblad (2005), "Does Financial Liberalization Spur Growth?", Journal of Financial Economics 77: 3-56. [ Links ]

Blundell, Richard and Stephen Bond (1998), "Initial conditions and moment restrictions in dynamic panel data models", Journal of Econometrics 87: 115-143. [ Links ]

Boyd, John; Ross Levine and Bruce Smith (2001), "The Impact of inflation on Financial Sector Performance", Journal of Monetary Economics 47: 221-248. [ Links ]

Buiter, Willem and Anita Taci (2003), "Capital Account Liberalization and Financial Sector Development in Transition Countries", in Bakker, Age F. P. and Bryan Chapple (eds.) Capital Liberalization in Transition Countries: Lessons from the Past and for the Future, Cheltenham, UK, Edward Elgar, pp. 105-141. [ Links ]

Calderón, César and Megumi Kubota (2009), "Does Financial Openness Lead to Deeper Domestic Financial Markets?" Policy Research Working Paper Series No. 4973, World Bank. [ Links ]

----------, and Lin Liu (2003), "The Direction Of Causality Between Financial Development And Economic Growth", Journal of Development Economics 72: 321-334. [ Links ]

Chinn, Menzie and Hiro Ito (2002), "Capital Account Liberalization, Institutions and Financial Development: Cross Country Evidence", Working Paper 8967, Cambridge, Ma, NBER. [ Links ]

----------(2006), "What Matters For Financial Development? Capital Controls, Institutions and Interactions", Journal of Development Economics 81, 163-192. [ Links ]

----------(2008), "A New Measure of Financial Openness", Journal of Comparative Policy Analysis 10(3): 309-322. [ Links ]

De Gregorio, José (1999), "Financial Integration, Financial Development and Economic Growth", Estudios de Economía 26(2): 137-161. [ Links ]

Do, Quy-Toan and Andrei Levchenko (2004), "Trade and Financial Development", Policy Research Working Paper No. 3347, World Bank. [ Links ]

Edison, Hali and Francis Warnock (2001), "A Simple Measure of the Intensity of Capital Controls", International Finance Discussion Paper No. 708, Washington, D.C., Board of Governors of the Federal Reserve System, September. [ Links ]

----------, Ross Levine; Luca Ricci and Torsten Slok (2002), "International Financial Integration and Economic Growth", Working Paper 9164, Cambridge, Ma, NBER. [ Links ]

Edwards, Sebastian (2001), "Capital Mobility and Economic Performance: Are Emerging Economies Different?", Working Paper 8076, Cambridge, Ma, NBER. [ Links ]

Eichengreen, Barry and David Leblang (2003), "Capital Account Liberalization and Growth: Was Mr. Mahathir Right?" Working Paper 9427. Cambridge, Ma, NBER. [ Links ]

Fama, Eugene (1991), "Efficient Capital Markets: II", The Journal of Finance 46(5): 1575-1617. [ Links ]

----------(1965), "The Behavior of Stock Market Prices", Journal of Business 38(1): 34-105. [ Links ]

Huang, Wei (2006), "Emerging Markets Financial Openness and Financial Development", Discussion Paper No. 06/588, Department of Accounting and Finance, University of Bristol. [ Links ]

Huang, Yongfu (2005), "What Determines Financial Development?" Discussion Paper No. 05/580, University of Bristol [ Links ]

Huang, Yongfu, and Jonathan Temple (2005), "Do External Trade Promote Financial Development?", Bristol Economics Discussion Paper No. 05/575, Department of Economics, University of Bristol. [ Links ]

Hymer, Stephen (1976), The international operation of national firms: A study of direct foreign investment, Cambridge, Mass., MIT Press. [ Links ]

Ito, Hiro (2006), "Financial Development and Financial Liberalization in Asia: Thresholds, Institutions and the Sequence of Liberalization", North American Journal of Economics and Finance 17: 303-327. [ Links ]

Klein, Michael and Giovanni Olivei (2001), "Capital Account Liberalization, Financial Depth and Economic Growth", Working Paper 7384, Cambridge, Ma, NBER. [ Links ]

Kose, Ayhan; Eswar Prasad and Marco Terrones (2007), "How Does Financial Globalization Affect Risk Sharing? Patterns and Channels", IZA Discussion Paper No. 2903. [ Links ]

Lane, Philip and Gian Milesi-Ferreti (2006), "The External Wealth of Nations Mark II: Revised and Extended Estimates of Foreign Assets and Liabilities, 1970-(2004)", International Monetary Fund Working Paper 06/69, Washington, International Monetary Fund. [ Links ]

La Porta, Rafael; Florencio Lopez-de-Silanes; Andrei Shleifer and Robert Vishny (1998), "Law and Finance", Journal of Political Economy 106(6): 1113-155. [ Links ]

Law, Siong (2009), "Trade openness, Capital Flows and Financial Development in Developing Economies", International Economic Journal 23(3): 409-426. [ Links ]

----------(2008), "Does a Country's Openness to Trade and Capital Accounts Lead to Financial Development? Evidence from Malaysia", Asian Economic Journal 22(2): 161-177. [ Links ]

----------, and Panicos Demetriades (2006), "Openness, Institutions and Financial Development", Working Paper WEF 0012, World Economy and Finance Research Programme. [ Links ]

Levine, Ross (2005), "Finance and Growth: Theory and Evidence", in Aghion P. and S. Durlauf (eds.), Handbook of Economic Growth, Amsterdam, North-Holland Elsevier Publishers, pp. 865-934. [ Links ]

----------(2002), "Bank-Based or Market-Based Financial Systems: Which Is Better?", Journal of Financial Intermediation 11: 398-428. [ Links ]

----------(1997), "Financial Development and Economic Growth: Views and Agenda", Journal of Economic Literature 35: 688-726. [ Links ]

----------, and Sara Zervos (1998), "Capital Control Liberalization and Stock Market Development", World Development 26: 1169-1184. [ Links ]

Morck, Randall and Lloyd Steier (2005), "The Global History of Corporate Governance an Introduction", Working Paper 11062. Cambridge, Ma., NBER. [ Links ]

Naceur, Samy; Samir Ghazouani and Mohammed Omran (2008), "Does Stock Market Liberalization spur Financial and Economic Development in the MENA Region?", Journal of Comparative Economics 36: 673-693. [ Links ]

Obstfeld, Maurice (2008), "International Finance and Growth in Developing Countries: What Have We Learned?" World Bank Working paper No. 34, Washington, DC, Commission on Growth and Development, World Bank. [ Links ]

----------(1994), "Risk-Taking, Global Diversification, and Growth", American Economic Review 84: 1310-1329. [ Links ]

----------and Alan Taylor (2003), "Globalization and Capital Markets, in Bordo, Michael; Alan Taylor and Jeffrey Williamson (eds.)", Globalization in Historical Perspective, Cambridge, Ma, NBER, pp. 121-188. [ Links ]

Prasad, Eswar; Raghuram Rajan and Arvind Subramanian (2007), "Foreign Capital and Economic Growth", Brookings Papers on Economic Activity 1: 53-230. [ Links ]

----------, Kenneth Rogoff; Shang-Jin Wei and Ayhan Kose (2003), "Effects of Financial Globalization on Developing Countries: Some Empirical Evidence", International Monetary Fund Occasional Paper No. 220, Washington, International Monetary Fund. [ Links ]

Rajan, Raghuram and Luigi Zingales (2003), "The Great Reversals: the Politics of Financial Development in the Twentieth Century", Journal of Financial Economics 69: 5-50. [ Links ]

Roubini, Nouriel and Xavier Sala-I-Martin (1995), "A Growth Model of inflation, Tax Evasion, and Financial Repression", Journal of Monetary Economics 35: 275-301. [ Links ]

Shleifer, Andrei and Robert Vishny (1986), "Large Shareholders and Corporate Control", Journal of Political Economy, 94: 461-488. [ Links ]

Stiglitz, Joseph (2000), "Capital Market Liberalization, Economic Growth and Instability" World Development 28(6): 1075-86 [ Links ]

1 This result is not possible if the financial market does not have perfect information (Stiglitz, 2000) or not developed institutions (Arestis, Nissanke and Stein, 2005).

2 It is worth noticing that Buiter and Taci (2003) did not explore the nexus of financial globalization-financial development, although they point out some ideas.

3 The estimations based on Arellano and Bond (1991) are not showed, but the results are similar to estimations with Blundell and Bond (1998).

4 We allow maximum of 2 lags to be used as instruments, to keep a sensible relationship between the number of cross-sectional observations and the number of overidentifying restrictions.

5 Indicators KAOPEN (financial openness) and INFLA (inflation) have not logarithmic transformation, because they are able to have some negative values.

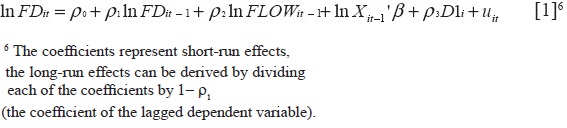

6 The coefficients represent short-run effects, the long-run effects can be derived by dividing each of the coefficients by 1-ρ1 (the coefficient of the lagged dependent variable).

It is assumed that the error term is not serially correlated, particularly; there is not a second order serial correlation. And Sargan's over-identification test is employed to validate the instruments. For further discussion, see Blundell and Bond (1998).

7 GDP is included like a control variable because the literature suggests a reverse causality with financial development (Levine, 2005; Calderón and Liu, 2003). inflation is included because it implies frictions in markets and credit rationing (Roubini and Sala-i-Martin, 1995; Boyd, Levine and Smith, 2001). And trade openness is a control variable because the empirical studies found a positive correlation with financial development (Do and Levchenko, 2004, Huang and Temple, 2005; Law, 2009; Baltagi, Demetriades and Law, 2009).

Also, literature suggests the inclusion of institutional variables, La Porta, Lopez-de-Silanes, Shleifer and Vishny (1998) argue that institutional framework is an important determinant of financial development, and the empirical studies about the financial globalization-financial development nexus, include institutional variables like explanatory variables. But, the available institutional variables do not change significantly in the time, and there are not good indicators of institutional levels for transition countries; so it is better to assume that these countries have similar levels of institutional development, therefore, investigation does not include institutional variables.

8 Baltagi et al. (2009) argue that financial development indicators are considerably persistent and dependent on history, so, they used a logarithmic transformation, like in this paper.

9 These six indicators include a deflation method, for details see Beck et al. (2009).

10 It was not possible to find a good indicator of the fifth function (to ease the exchange of goods and services).

11 Herfindahl-Hirschman is another popular index of concentration, but it was not possible to estimate it because the information about the number of banks was not available for these countries over the period of analysis.

12 It is also a measure of market failure, where the allocation of financial services is not efficient because of non-competitive markets. It is worth noticing, that the indicator does not include the possibility of market failure because of information asymmetries, principal-agent problems or externalities.

13 This is a small rate among rich countries, for example, United Kingdom has a mean of 1.32.

14 For further discussion, see Edison and Warnock (2001), Edwards (2001), Edison et al. (2002), Lane and Milesi-Ferretti (2006); Chinn e Ito (2008).

15 Principally, information is available over 1995-1998 period.

16 This is a small rate among rich countries, for example, the United Kingdom has a mean of 71.66.

17 Central banks frequently intervene in the course of interest rates; the market does not act freely. So, the convergence of interest rates has some bias to measure financial globalization, but it is still a good indicator of financial liberalization in times of globalization.

18 To measure financial interdependence other studies used international arbitrage pricing models, but the indicator Intere is simple and has not relevant differences with other indicators.

19 The model was transformed in different forms, but it was not possible to correct the problem, and like Baltagi et al. (2009: 292), the solution is to notify.

INFORMACIÓN SOBRE EL AUTOR:

Edgar Demetrio Tovar García. Miembro del Sistema Nacional de Investigadores (candidato), posdoctorado en la Facultad de Economía de la Universidad Nacional Autónoma de México, doctor europeo en Economía por la Universidad de Barcelona con estancia en la Universidad de Tampere, Finlandia.