nueva página del texto (beta)

nueva página del texto (beta) Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

Permalink

Introduction

After the pioneering works of Booth et al. (1982), Cheung (1993), and Baum et al. (1999), emphasis on the exchange rate shifted from conceptualization and pass-through to the understanding of its econometric characteristics. The exchange rate is a price that is very precious to the government. Its concept is sub-divided into two-the nominal and the real exchange rates.

The inquiry of exchange rate undercurrents and its cointegrating relationships has gained traction among researchers in the last three decades (see Baillie & Bollerslev, 1994a,b; Wang, 2004; Crato and Ray, 2000; and Fang et al. (1994). Studies on the exchange rates in Nigeria did not explicitly consider mean-reversion. Instead, they viewed the exchange rate as a macroeconomic variable and its impact on economic growth(see Oloyede and Fapetu, 2018; Ikpesu and Okpe, 2019) while others dwelled on its short-term forecasting(see Nyoni, 2018; Ejem and Ogbonna, 2019). Also, some studies considered its effect on the financial dollarization and remittance inflows (see Udoh and Udeaja, 2019; Adejumo and Ikhide, 2019).

The measurement of the degree of persistence is critical since it represents the stability of the country's Exchange rate. Furthermore, this type of information is useful for policymakers in the case of an exogenous shock, when alternative policy measures must be implemented based on the degree of persistence. Breaks in the series are another essential element of exchange rate data that must be modeled based on the data's particular properties. According to Taylor and Sarno (2001), research on the behavior of currency rates in transition economies is fairly scarce.

This study seeks to investigate the stochastic properties of exchange rates using the fractional cointegration VAR model with a multivariate set-up developed by Nielsen and Popiel (2018) and complemented with the univariate VAR model using weekly series. In line with the suggestions by Baillie & Bollerslev (1994a&b) and Diebold et al. (2004), persistence needs to be thoroughly investigated when dealing with cointegrating relationships of exchange rates. The need to enhance policy innovation and efficiency underscored the linkage of the observed shocks to the degree of persistence of exchange rates. Because of the relevance of the exchange rate to all facets of the Nigerian economy, including monetary policy decisions, and the fact that this study is the pioneering work on the test for the nominal exchange rates persistence in Nigeria pre and post the global financial crisis, necessitates the study.

Utilization of an alternative technique of Narayan et al. (2016) and Narayan and Liu (2015) GARCH-based approaches with different data frequencies (weekly and monthly) to test for the robustness in the nominal exchange rates. In contrast to other techniques applied in checking for robustness, the GARCH-based procedure is robust in handling data frequencies that are susceptible to elevated volatility.

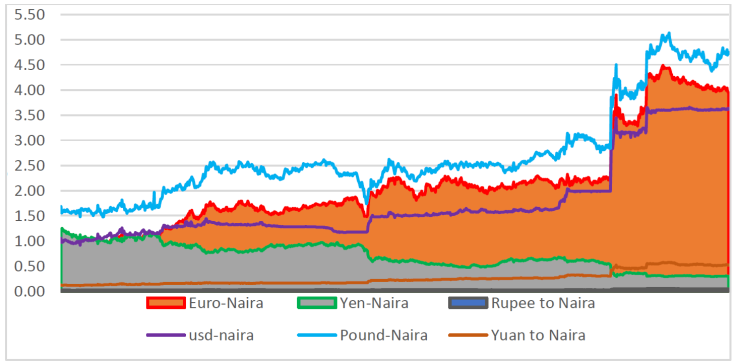

Finally, the descriptive statistics (see Table 1 Figure 1) clearly show an upward trend in the nominal exchange rates after the GFC, except in Yen-Naira, which is due to the continuous depreciation of the naira. This depreciation is further accounted for by Nigeria’s import-dependent economy and crude oil receipt of over 95% of government revenue and the attendant consequences on the purchasing power of the country. These remarkable distinctions in the behavioral pattern of the nominal exchange rates in Nigeria pre and post the global financial crisis generate a key excitement for empirically following the same path in the analyses

Table 1 Bai-Perron test for structural shift

| Exchange Rate | Break date with intercept | Break date With intercept and trend |

|---|---|---|

| USD | 06/20/2005 | 06/20/2005 |

| EURO | 06/20/2005 | 06/20/2005 |

| YEN | 07/08/2002 | 07/08/2002 |

| POUND | 06/20/2005 | 07/15/2002 |

| RUPEE | 06/20/2005 | 06/20/2005 |

| YUAN | 06/20/2005 | 06/20/2005 |

From the results in Table 1 above, the absence of breaks Post-GFC period is confirmed, consequently, the data points are partitioned into the Pre- and Post-GFC periods.

Following the introduction, section 2 expounds on a review of the literature. The detailed methodology and data used are contained in section 3 whilst the empirical results are presented and discussed in section 4. Finally, Section 5 concludes the study.

Literature review

The literature on the dynamics of exchange rates could be categorized into two. They include the integer degrees of differentiation in exchange rate series (see Anthony and MacDonald,1999; Bleaney et al.,1999; Campa and Wolf, 1997 and Solis et al; 2002) and the long-run memory and fractional integration of exchange rates (see Booth et al., 1982; Cheung,1993; Baum et al.,1999; Crato and Ray, 2000; Gil-Alana and Mudida, 2018 and Wang, 2004).

Several studies have been conducted to investigate the existence or lack of long memory in exchange rates. Corazza and Malliaris (2002) conduct a study on foreign currency markets using the Hurst exponent and discover indications of long memory. Nath and Reddy (2002) examined the impact of long memory on the Indian foreign currency market versus the US dollar using Hurst R/S statistics and a variance ratio test. Peters (1996) investigated the Long Memory features of daily exchange rate data from the USD, Japanese yen, GBP, Euros, and Singapore dollar and discovered evidence of Long memory when utilizing the R/S technique. Bhar (1994) investigates Long memory in the Yen/dollar exchange rate and discovers no evidence of Long memory suggesting efficient pricing by market players when utilizing the modified R/S technique. kumar (2011) used the Hurst exponent, Hurst Mandelbrot R/S statistic, Lo's modified R/S statistic, Robinson's semi parametric estimator, and the modified GPH estimator to examine the presence of Long memory in the Indian foreign exchange market. The findings revealed that the Indian foreign currency market has a long memory.

Also, leveraging on data from 1980 to 2009, Arize (2011) showed the existence of a mean-reversion in both the linear and non-linear mean reversion for developing countries. Anouro et al. (2006) used a non-linear stationarity test to study the behavior of African exchange rates and uncovered that 11 out of the 13 are non-linear stationary. The result seems to suggest that bilateral nominal exchange rates are mean-reverting to the Purchasing Power Parity (PPP) equilibrium. Cashin and Mcdermott (2006) used data from 90 developed and developing countries. The outcome of the study shows that the speed of parity-reversion is slower for developing countries than developed countries, especially countries with fixed exchange rate regimes.

The effect of exchange rate shocks on the macroeconomy dominates the extant literature on the exchange rate for developing countries. For instance, Barhoumi (2007) using the structural VECM model, and the trends approach considers the exchange rate pass-through in 12 developing countries. The study concludes that the pass-through ratio in developing countries varies because of the diversity of structural shocks.

Lubinga and Kiiza (2013) applied a Panel-GARCH model to analyses the impact of the exchange rate dynamic bilateral trade flows between Uganda and her major trade partners. The evidence of the study suggests the importance of the issue of transitory or permanence of shocks in exchange rates for developing countries. Gil-Alana and Mudida (2018) examine nominal exchange rates in Kenya using the fractional integration technique. The evidence of the study suggests that exchange rates are nonstationary and non-mean-reverting

The empirical literature on exchange rates in Nigeria did not consider the issue of mean-reversion and, none of the existing studies either used the fractional integration approach or dichotomized the samples into pre-GFC and post-GFC. Also, none of the studies checked for robustness using the Garch-Model with weekly and monthly data frequencies. Most of the literature focuses mainly on using cointegration approaches to investigate the relationships between exchange rates and other macroeconomic variables. See (Ikpesu and Okpe (2019); Adejumo and Ikhide (2019); Oloyede and Fapetu (2018); Udoh and Udeaja (2019) and Nyoni (2018).

The literature on exchange rates in Nigeria mostly emphasizes the effect of exchange rate movement or regime on variables that determine the current behavior of the macro-economy. This study will contribute to the body of knowledge by filling the gap in the literature on the examination of shocks to nominal exchange rates in Nigeria to ascertain whether they are permanent or transitory using the fractional integration and fractional cointegration VAR models.

Methodology

The traditional univariate technique for evaluating persistence

A significant attribute of many time series data is non-stationarity. The evaluation of the persistence using the traditional univariate approach of order p [AR(p)] can be written as:

Given

The fractionally integration model

The study also applies the fractional integration technique based on the recent findings in the literature (See Canarella and Miller, 2017; Gil-Alana and Carcel, 2018; Canarella and Miller, 2016; Usman and Akadiri, 2021 and Ebuh et al 2021) that stationary economic series can be given in a fractional form and may not take integer values. The fractional integration approach indicates that the series might be fractionally integrated. Such that shocks are not permanent but die out over long horizons.

Consequently, we examine Nigeria’s nominal exchange rates

L is the lag operator

Hence,

Accordingly, Equation (1) is presented as follows:

Equation (5) is developed to emphasize the critical role

We employ the parametric method in analyzing fractional integration which involves the maximum likelihood estimator of Sowell (1992). A major wrench to the fractional integration technique is the accuracy gained by leveraging on the news in the data via the parameter estimates. However, in line with Sowell (1992), a downside of the model is the sensitivity of the parameter estimates to models considered which could be misleading due to misspecification.

Fractionally cointegrated VAR (FCVAR) for nominal exchange rates

We examine Nigeria’s Nominal exchange rates, to check if they display long-run characteristics using the fractionally cointegrated VAR (FCVAR) proposed by Johansen (2008) and later extended by Johansen and Nielsen (2010, 2012), and Nielsen and Popiel (2018). The FCVAR allows for a fractional process of order d that cointegrates to order d-b. From a policy viewpoint, if Nominal exchange rates are cointegrated, this implies that policy targeted at one of the exchange rates will also influence other rates. Additionally, if the cointegration is fractional, the impact of policy on these rates will only disperse only after short horizons. Consider

The FCVAR model is a derivative of Equation (6), this is done by interchanging the

Given

The method of estimating the FCVAR follows the following steps: (a) the optimal lag length model is estimated; (b) the cointegration rank is established; (c) the data from (a) and (b) are employed to check for fractional cointegration; and in conclusion, (d) the Likelihood Ratio (LR) test is used to compare FCVAR model with the CVAR model by placing a limiting the null. If the null hypothesis is not accepted, then the FCVAR is favored, if not, the CVAR is accepted.

Results and discussions

Testing for structural shift in persistence

The Bai and Perron (2003) test is employed to test for structural shifts in persistence. The maximum number of structural breaks allowed in the time series is five. This procedure comprises a chronological application of test, assumed to produce an optimal result in selecting the number of breaks. The results are reported in Table 1

Preliminary analysis

Weekly data from 1999 to 2020 were used for the analyses. The nominal exchange rate pairings covered are USD-Naira, Euro-Naira, Yen-Naira, Pound-Naira, Rupee-Naira, and Yuan-Naira rates. The data for this study were sourced from the Central bank of Nigeria Statistical and Bloomberg databases. Various descriptive statistics carried out on the six nominal exchange rate variables were tabulated in Table 2. The data for the study were subdivided into two subsamples, given the results of the Bai-Perron test in Table 1 and consequently were split into Pre and post the Global financial crisis (GFC) individually. The Post-GFC captures the period of the crisis and afterward whilst the Pre-GFC is the period before September 2007. The Post-GFC stretch is so defined because of Nigeria’s peculiarity in which the effect of the GFC on macroeconomic fundamentals postdates the crisis period. Inferring from Table 2, the exchange rates for USD-Naira, Euro-Naira, Yen-Naira, Pound-Naira, Rupee-Naira, and Yuan-Naira exhibit higher volatility before the GFC than afterward.

Table 2 Descriptive statistics.

| Statistic | Usd-Naira | Euro-Naira | Yen-Naira | Pound-Naira | Rupee to Naira | Yuan to Naira |

|---|---|---|---|---|---|---|

| Full Sample | ||||||

| Mean | 177.25 | 212.16 | 70.17 | 269.92 | 3.25 | 25.41 |

| Standard Deviation | 82.53 | 94.22 | 25.36 | 92.68 | 0.92 | 13.23 |

| Skewness | 1.45 | 1.13 | -0.04 | 1.21 | 1.40 | 1.21 |

| Kurtosis | 0.58 | 0.39 | -1.09 | 0.50 | 0.71 | 0.17 |

| No. of Observations | 1084 | 1084 | 1084 | 1084 | 1084 | 1084 |

| Pre-GFC | ||||||

| Mean | 122.53 | 137.21 | 94.92 | 207.26 | 2.70 | 14.99 |

| Standard Deviation | 12.10 | 30.18 | 11.26 | 37.55 | 0.29 | 1.59 |

| Skewness | -0.81 | -0.22 | 0.30 | -0.18 | -0.21 | -0.78 |

| Kurtosis | -0.58 | -1.68 | -0.77 | -1.64 | -1.42 | 0.77 |

| No. of Observations | 433 | 433 | 433 | 433 | 433 | 433 |

| Post-GFC | ||||||

| Mean | 213.52 | 261.88 | 53.76 | 311.51 | 3.62 | 32.32 |

| Standard Deviation | 89.05 | 89.19 | 17.60 | 94.92 | 1.00 | 13.01 |

| Skewness | 0.81 | 0.96 | 0.37 | 0.87 | 0.85 | 0.73 |

| Kurtosis | -1.08 | -0.78 | -0.27 | -0.86 | -0.92 | -1.02 |

| No. of Observations | 652 | 652 | 652 | 652 | 652 | 652 |

Source: Authors’ Computation

Besides, the mean and standard deviations of the variables were higher Post-GFC than before GFC. Thus, implying the presence of more asymmetry GFC afterward on the nominal exchange rates.

The descriptive statistics and the plot of the six nominal exchange rate variables in Figure 1, clearly shows an upward trend in the nominal exchange rates after the GFC except in Yen-Naira. This upward trend in the nominal exchange rates could be attributed to the continuous depreciation of the naira. These outstanding distinctions in the behavioral pattern of the nominal exchange rates in Nigeria before and afterward of the GFC create the needed enthusiasm for empirically following the same path in the analyses.

Main results

The study examines the nominal exchange rates in Nigeria using the full, pre-GFC, and post-GFC sample periods to test for the existence and the degree of persistence of the nominal exchange rates in Nigeria. The study leveraged on the univariate and the fractional cointegrated VAR models with and without a trend. Table 3 presents the results on the traditional approach for persistence on the nominal exchange rates, which were observed to be non-stationarity as the magnitude of the persistence is close to unity for both with intercept and with intercept and trend. A further examination of the results shows that persistence is mean reverting in each sample considered, implying that the degree of persistence is temporal and not permanent. Thus, indicating that the nominal exchange rates will revert to their long-run mean.

Table 3 Traditional Approach with weekly Data

| Exchange Rate | Full Sample | Pre-GFC | Post-GFC | ||||

|---|---|---|---|---|---|---|---|

| Intercept | Intercept and Trend | Intercept | Intercept and Trend | Intercept | Intercept and Trend | ||

| US |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Euro |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Yen |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pound |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Rupee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Yuan |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(where () are standard errors, [] are p=values and A, B, C represent statistical significance at 1%, 5% and 10% respectively)

Also, the Wald test was used to if the degree of persistence is not statistically different from one. The outcome revealed that the persistence’s were statistically insignificant in all the samples at various degrees, except the US dollar exchange rate in the pre-GFC period.

Also, we compute the half-life estimates for a shock to Nigeria’s Nominal exchange rates. The half-life fundamentally reveals the period it takes for the impact of a shock on the exchange rates to divide into two. From the results presented in Table 4, it lends credence to the findings in the traditional approach that exchange rate persistence is higher in the post-GFC period than the pre-GFC period. This finding emphasizes the need for better coordination between the fiscal and the monetary authorities, to adequately manage the exchange rates in the post-GFC period.

Table 4 Half-Life of Nominal Exchange Rate in Nigeria

| Exchange Rate | Pre-GFC | Post-GFC | ||

|---|---|---|---|---|

| Intercept | Intercept & Trend | Intercept | Intercept & Trend | |

| USD | 85.178 | 30.8151 | 835.521 | 110.543 |

| EURO | 203.308 | 43.508 | 404.751 | 80.418 |

| YEN | 65.614 | 28.892 | 602.164 | 85.947 |

| POUND | 168.194 | 21.675 | 276.657 | 72.508 |

| RUPEE | 87.688 | 18.348 | 250.963 | 98.112 |

| YUAN | 113.766 | 16.996 | 720.019 | 68.920 |

Note: If mean reverting, (

To complement the traditional approach, we use a fractionally integrated approach to test for persistence. From Table 5, the estimates obtained using the fractionally integrated approach were reported under two cases (with intercept and with intercept and trend) and three samples (full sample, Pre-GFC, and Post-GFC), as with the traditional approach. Several features are noticeable in Table 1. First, all the estimated values are below 0.5, showing that the six nominal exchange rates under consideration are fractionally integrated and exhibit long memory. As in the traditional approach, we also find the level of persistence to be higher for the post-GFC sample for all exchange rates than the pre-GFC sample. Leveraging on the Wald test, the values of the fractional parameter estimates were statistically less than one, contrary to the traditional approach. This result indicates that, although the Nominal exchange rates exhibit long-run memory impact of any policy shock on the exchange rate to die out, it may not be permanent.

Table 5 Fractional Integration approach with weekly data

| Exchange Rate | Full Sample | Pre-GFC | Post-GFC | ||||

|---|---|---|---|---|---|---|---|

| Intercept | Intercept and Trend | Intercept | Intercept and Trend | Intercept | Intercept and Trend | ||

| US | d |

|

|

|

|

|

|

| d=1.0 |

|

|

|

|

|

|

|

| Euro | d |

|

|

|

|

|

|

| d=1.0 |

|

|

|

|

|

|

|

| Yen | d |

|

|

|

|

|

|

| d=1.0 |

|

|

|

|

|

|

|

| Pound | d |

|

|

|

|

|

|

| d=1.0 |

|

|

|

|

|

|

|

| Rupee | d |

|

|

|

|

|

|

| d=1.0 |

|

|

|

|

|

|

|

| Yen | d |

|

|

|

|

|

|

| d=1.0 |

|

|

|

|

|

|

|

(where () are standard errors, [] are p=values and A, B, C represent statistical significance at 1%, 5% and 10% respectively).

Are nominal exchange rates fractionally cointegrated in Nigeria?

In furtherance to the objective of the study, we evaluate the likelihood of fractional cointegration amongst the various nominal exchange rates. The test for fractional cointegration is because currencies from Nigeria’s major trading partners and its reserves expose the Nigerian economy to both commodity price and trade shock. Also, Nigeria’s economy largely depends on import and trade interconnectedness, which could impact on policy actions aimed at stabilizing the exchange rate. Thus, the six nominal exchange rate variables were tested for cointegration. The study estimated the FCVAR, which is a unique variant of the CVAR with a fractional value of the order of integration. This result is achieved by first obtaining the maximum lag value, followed by the rank. These two parameters are used to obtain the order of integration. Inferring from the results in Table 6, we observe across the three sub-samples, four cointegrating relationships for the full sample and five for the Pre-GFC and Post-GFC samples, respectively. This result implies the existence of a long-run relationship amongst the nominal exchange rates of the six selected currencies with Naira. For the full sample, cointegrating relationships are better formed using the CVAR model than the FCVAR as the estimated fractional parameter is greater than 1. However, in the two sub-samples, cointegrating relationships are better formed using the FCVAR model, as the fractional parameters are both 0.010. Hence, justifying the implementation of the fractional framework. Additionally, in Table 7, we find the data to lends support to estimating the fractional parameter using FCVAR over the conventional CVAR, for the sub-samples samples, as shown by the statistically significant LR statistics. However, the CVAR model is suitable to ascertain cointegrating relationships for the full sample period.

Table 6 FCVAR (Weekly)

| Rank | Lag | d | |

|---|---|---|---|

| Full Sample | 4 | 2 | 1.071(0.016) |

| Pre-GFC | 5 | 3 | 0.010(0.000) |

| Post-GFC | 5 | 3 | 0.010(0.000) |

where: d represents the fractional parameter. The AIC is used in determining the optimal lag length. using, a maximum of lag 3. The Values of the standard errors of the Fractional parameter are presented in ( ).

Table 7 CVAR vs FCVAR (Weekly)3

| LR | P-value | |

|---|---|---|

| Full Sample | 1.767 | 0.145 |

| Pre-GFC | 180.944 | 0.000 |

| Post-GFC | 102.708 | 0.000 |

Note: The LR test restricts the fractional parameter to 1 under the null hypothesis. A failure to reject the null implies the acceptance of the CVAR, while the opposite favour the FCVAR.

Robustness

We employed Narayan and Liu (2015) and Narayan et al. (2016) GARCH-based unit root techniques to check for the robustness of results. The benefit of using this approach over others, is its usefulness in allowing the error term to follow a GARCH based process, as against other methods. Tule et al. (2020), Salisu et al. (2020), Salisu and Adeleke (2016), Narayan and Liu (2015), and Narayan and Sharma (2015), argue the choice of data frequency is of importance in empirical analyses. On this note, we considered, in addition to the weekly series, a monthly data frequency of nominal exchange rates to supplement the results obtained.

The results were similar to the traditional approach and the fractionally integrated approaches (Table 8 & 9) with higher degrees of persistence observed in the post-GFC period. Also, from the FCVAR estimates (Table 10 & 11), using the monthly samples, we find similar results to the weekly frequency. The results from the CVAR are superior to the FCVAR for the full sample, and the FCVAR results are superior for the Pre-GFC and Post-GFC periods, respectively. From these findings, the results are unaffected by the different data frequencies.

Table 8 Narayan and Liu (2015) and Narayan et al. (2016) GARCH-based model (Monthly)

| Exchange Rate | Full Sample | Pre-GFC | Post-GFC | ||||

|---|---|---|---|---|---|---|---|

| Intercept | Intercept and Trend | Intercept | Intercept and Trend | Intercept | Intercept and Trend | ||

| US |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Euro |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Yen |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pound |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Rupee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Yuan |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where () are standard errors, [] are p=values and A, B, C represent statistical significance at 1%, 5% and 10% respectively).

Table 9 Narayan and Liu (2015) and Narayan et al. (2016) GARCH-based model (Monthly)

| Exchange Rate | Full Sample | Pre-GFC | Post-GFC | ||||

|---|---|---|---|---|---|---|---|

| Intercept | Intercept and Trend | Intercept | Intercept and Trend | Intercept | Intercept and Trend | ||

| US |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Euro |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Yen |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Pound |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Rupee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Yuan |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(where () are standard errors, [] are p=values and A, B, C represent statistical significance at 1%, 5% and 10% respectively).

Table 10 FCVAR (Monthly)

| Rank | Lag | d | |

|---|---|---|---|

| Full Sample | 5 | 3 | 0.905 (0.049) |

| Pre-GFC | 4 | 3 | 0.010 (0.000) |

| Post-GFC | 4 | 3 | 0.010 (0.000) |

where: d represents the fractional parameter. The AIC is used in determining the optimal lag length. using, a maximum of lag 3. The Values of the standard errors of the Fractional parameter are presented in ( ) .

Table 11 CVAR vs FCVAR. (Monthly)

| LR | P-value: | |

|---|---|---|

| Full Sample | 3.037 | 0.181 |

| Pre-GFC | 216.485 | 0.000 |

| Post-GFC | 152.191 | 0.000 |

Note: under the null hypothesis, the LR test restricts the fractional parameter to 1. A failure to reject the null implies the acceptance of the CVAR, whilst the opposite favors the FCVAR.

Conclusions

This study sets out to achieve two key objectives. First, to examine the behavior of the nominal exchange rates persistence in Nigeria, during the Pre-GFC and Post-GFC periods, in addition to the full sample. Second, to ascertain whether or not, the nominal exchange rates are fractionally integrated. Consequently, for the main analysis, we adopt the traditional, fractionally integrated, and the fractionally cointegrated VAR models to analyze, the weekly frequency of the USD-Naira, Euro-Naira, Yen-Naira, Pound-Naira, Rupee-Naira, and Yuan-Naira nominal exchange rate variables.

We find, using both the traditional and fractionally integrated approaches, that the Post-GFC consistently maintains higher magnitudes of persistence for all exchange rates, than the Pre-GFC period. Both results suggest that the response of the nominal exchange rates to shocks were slower during the post-GFC than the Pre-GFC period. The result indicates the need for better coordination between the fiscal and monetary authorities, for the effective and efficient management of the exchange rates in the post-GFC era. Also, our results depict the nominal exchange rates, are fractionally cointegrated. The results, further reveal the FCVAR to be better in forming cointegrating relationships than the conventional CVAR for the Pre and Post-GFC periods. However, the reverse is the case, for the full sample results. The insight into this study is to aid policy innovation on exchange rates.

What are the most important takeaways from our findings? To begin, it is obvious that substantial policy actions must be adopted in the case of a shock in order to return the series to their original patterns. Second, for the series to respond more quickly, a proactive foreign exchange policy attitude is essential. Finally, this study may be expanded in numerous ways. Nonlinear structures may be considered in the context of fractional integration; moreover, the structural break technique used in this study can be expanded to allow for more flexible specifications, such as regime-switching models or time varying models.