nueva página del texto (beta)

nueva página del texto (beta) Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

PermalinkIntroduction

This study investigates the role of the firm life cycle stage on the synergy creation after merger and acquisition (M&A) activities. Synergy creation is here regarded as the increase in performance measurements on the remaining company in the years after the event. The process of M&A is inherently linked with the growth of a firm (Penrose, 1959). A merger and/or an acquisition assemble a choice of growing by recombining the old or building a new project/firm. Such a position is a breakdown on the analogy of the firm as a biological body, since a corporation might be formed by other firms, changing (or not) the identity, culture and, mainly, achieving economies of scale (Angwin, 2001).

After four periods of reorganizations, between 1887 and 1980, during the so called “M&A waves”, scholars struggled to develop theoretical models on takeover bidding process (Fishman, 1988; Grossman & Hart, 1980), and on the choice of payment (cash or stock) under asymmetric information (Hansen, 1987). Although, the theories converge on the assumption that the purchase of the target firm will increase the utility function of the acquirer (Stigler, 1950), through an expected value gain. However, the empirical literature does not favor these players. Instead, the evidence of unsuccessful acquisitions signalize that the target shareholders have their value increased in the process (Dargenidou et al., 2016; Renneboog & Vansteenkiste, 2019).

The literature on M&A has been regarded in two different streams: finance, which is related to capital market reaction (Elango et al., 2019; Greenwood & Schor, 2009); and industrial economics, attempting to discuss fundamentalist performance measures, using accounting numbers (Minadeo & Camargos, 2009; Stiebale, 2016; Wu & Chung, 2019). This paper is placed on the former stream, because we shed light on the operational gain resulted from the expected synergy to the acquirer, regardless the capital market reaction.

Prior literature evidence some value-destroyer drivers related CEO hubris (Hayward & Hambrick, 1997), external deal advisors (Chahine & Ismail, 2009; Hayward, 2003; Hunter & Jagtiani, 2003), as well as other firms characteristics that reduce the propensity to engage in M&A (Al-Sabri et al., 2020). Moreover, Bhaumik & Selarka (2012) state that the conflicting relationship between managers and owners is the key reason for M&A failures. Fukuda (2020) documents a negative effect of M&A for domestic deals, but a positive effect for international deals in Japan. Under a governance perspective, recent studies have documented a positive effect on post-event performance related to CEO experience about the target’s industry (Fich & Nguyen, 2019) and CFO influence on the board (Ferris & Sainani, 2021). This enlighten that an opportunity of M&A must be considered under a less uncertain environment, which is more than a specific manager.

In this regard, more than the opportunity growth of the target (Bhattacharya & Li, 2020), the potential acquirer needs to observe its potential of acquiring (or merge with) another firm. This might be understood in terms of firms characteristics that reflect more than a moment, but the operating, investing, and financing arrangement of the firm in each moment (Ames et al., 2020). According to Black (1997), Cantrell & Dickinson (2018), Dickinson, Kassa, & Schaberl (2018) and Jenkins & Kane (2004), this arrangement configures the firm life cycle stages, whereas introducing and declining firms, for instance, present differences in structure and strategies compared to growing and mature firms.

The mature stage is characterized by positive cash flow from operating and negative cash flow from investing and financing activities (Dickinson, 2011). This stage is consistently associated with higher operational returns on assets (Dickinson, 2011), lower asymmetry (Novaes & Almeida, 2020), lower cost of capital (Hasan et al., 2015), greater governance quality (Al-Hadi et al., 2016; Gonçalves et al., 2019; Zhao & Xiao, 2018) higher investment level (Hasan & Habib, 2017b), and higher dividend payouts (Bhattacharya et al., 2020). Besides, mature firms are more likely to engage in an M&A as acquirer (Owen & Yawson, 2010), more expected to enjoy greater cash-slack, which can imply better new growth opportunities (Damodaran, 2005).

In this regard, considering an opportunity of M&A to emerge from both an uncomfortable situation of the target-firm and from the acquirer optimism, we follow Owen & Yawson (2010) as well as the recent results of Ames et al. (2020) to assume the firm life cycle to play a separating equilibrium role on the pursuing of synergy. Then, this paper aims to investigate the role of life cycle stage in the synergy creation after a merger and acquisition process at the Brazilian capital market.

We use the Brazilian scenario because, as an emergent market, member of the BRICs, the country has recently passed through a significant change in economic policies, which has been drawing the attention of both foreign and local investors. Then, the results of this research have the potential to enlighten the conditions where synergy appears to be true (or not) in developing countries.

Taking into account the existence of “waves of mergers and acquisitions”, Napier (1989, p. 272) claims for “more systematic investigations and better understanding of the impact of mergers”. Likewise, Ghosh & Ghosh (2014, p. 113) sustain that M&As are the “prime vehicles for business engagement across the countries through the foreign direct investment route”. Henceforth, the results of this paper are expected to be useful for financial market analysts and, mainly, managers and investors to improve their decision-making process about the moment of rearranging or purchasing a firm.

We estimate a control group using the PSM procedure by year, size, and industry concentration level. Although the theoretical expectation, we firstly document a decrease in performance measure on average. Moreover, we found no significant result in different performance measures after the M&A for mature firms compared to others. This nonsignificant result is robust for firms in other stages. Therefore, we refute the research hypothesis that as acquirer, mature firms realize greater synergy creation when compared to firms in other stages after a M&A activity.

The remainder of this paper is divided into other 4 parts: section 2 presents the theoretical and hypothesis development; In section 3, we present the operationalization of the sample, variables and econometric issues; section 4 is dedicated to the results, starting from the descriptive analysis of M&A scenario in Brazil, passing by the propensity score matching procedures, until the estimations results; and finally, sections 5, with the concluding remarks and suggestions for future studies.

Theoretical and hypothesis development

Mergers and acquisitions - M&A

A Merger process denotes a strategic deal to form a single economic unit, whilst in an Acquisition, there is a purchase of more than the necessary portion of voting shares from the target-firm to control it. This negotiation involves at least two parts: the acquirer (bidder), who is usually optimist and self-motivated to merge with another firm interested in a potential synergy creation; and the target, who will make the deal if the present value of the expected future benefits (not only financial) is expected to be lower than the negotiation value (and consequent benefits) offered by the bidder.

This takeover process may be friendly (in a private offer) or hostile through a “Tender Offer”, which means an offer directly to the voting shareholders, bypassing the board of directors. There is also a situation when the offer is formally declined by the board of directors, but the potential acquirer decides to keep on the offering (Copeland et al., 2012; Hall, 2002; Matos, 2001; Miller, 2009; Wangerin, 2019).

The incentives towards the decision of merging with (or acquiring) another firm is sometimes based on a horizontal purpose, where the firm seeks the monopoly and then buys its rival, or by a vertical one, when two firms operate in the same value chain in an industry (Grossman & Hart, 1986; Huyghebaert & Luypaert, 2010). In other situation, big companies sometimes diversify risk by forming conglomerates (Hubbard & Palia, 1995; Mueller, 1969, 1977). This economic group diversify its resources and operations to add a new product line, to expand commercial boundaries or due to a pure diversification (Copeland et al., 2012; Hubbard & Palia, 1995; Lewellen, 1971; Matos, 2001; Mueller, 1969), such as Unilever, DuPont, Mitsubishi, Yamaha among other.

The process of M&A may start when a bidder identifies a target firm and evaluates it, considering potential synergies, including nonpublic information related to growth plans among others (Tsao, 2009; Wangerin, 2019). Then, a bid will be offered when the new valuation results in an intrinsic firm value greater than the market current value. Otherwise, a rational bidder abandons the negotiation (Bi & Wang, 2018). However, behind such a comparison of valuation and assumptions for value creation, there are situations concerning the “hubris”, when the investment decision is driven by overconfidence and then it results in gain only for the target shareholders (Hayward & Hambrick, 1997; Morck et al., 1990; Roll, 1986).

Reasonably, when a firm decides to keep the negotiation, facing and beating existing competitors (raiders) on this process, the most expected result, under the financial point of view, is a gain in efficiency, which might be understood as any gain resulted from the reorganization, related to taxes, cost of debt, production scale or even agency costs (Angwin, 2001). In short, this “synergy creation” is expected to minimize the total unit cost of the firm, maximizing the firm value to shareholders, by the classical “one plus one equals three”.

Traditional literature is based on different argument to explain an M&A. Beside the efficiency argument, Healy et al., (1992) summarize that the entrepreneurs are also motivated by: i) information, based on the expectation that the announcement creates a short term effect on stock prices, creating an opportunity to some target investors to assume a short position at higher prices; ii) agency, that is when the shareholders decide not to enhance the managers responsibility over an eventual increase in free-cash flow; iii) market power, that is related to the seeking for monopoly; and last but not least iv) taxes, which implies an idea that some rearrangements are motivated by a tax burden reduction.

Bradley & Korn (1984) discuss a methodology to estimate a “true” cost-benefit in an M&A process. The authors point out that sometimes political motive overshadows the traditional “value maximizing approach”. Mueller (1972) argues that big corporation intends to maximize the managerial, not stockholder, welfare. Then, the expected gain in an M&A is less related to profitability or pecuniary reward, since the manager utility is associated with the size and the growth in size, but it depends on the position of the top manager distance to the entrepreneurs.

Napier (1989) states an M&A to be incentivized for gains in technical expertise or knowledge in capital allocation, which refers to human capacity. The author points out that culture, employee reaction and structure are relevant factors to be considered before merging or acquiring a firm. Moreover, the reasons why a firm intends to acquire another company may be related to the life cycle stage of both firms (Ames et al., 2020; Owen & Yawson, 2010).

In 1985, 30% of the M&A resulted in “divestiture”, and more than 50% were “generally unsuccessful” (Napier 1989, p. 271). In UK, examining the deals between 1985 and 2012, Dargenidou et al. (2016) found that, on average, the acquisitions in UK resulted in a decrease in market value. Specifically, two-thirds resulted in value-destruction. Fich & Nguyen (2019) examine deals on the 19972012 period in US, and show that the knowledge of the acquirer CEO (Chief Executive Officer) about the target’s industry is positively related to the synergy creation.. Recently, Ferris & Sainani (2021) document a CFO (Chief Financial Officer) influence effect on deal completion in UK deals. The authors find that more influential CFOs are associated with lower deal premium and greater post-event operating and financial performance. These findings enlighten that an acquisition must be considered under a less uncertain environment, otherwise the expectation of synergy creation will not appear to be true.However, emergent capital markets like the ones from the BRICs are characterized by intensive concentration (Almeida & Dalmácio, 2015; Bhaumik & Selarka, 2012), which modifies the traditional theory of the firm and this may lead to different results compared to developed countries. For example, Camargos & Barbosa (2009) showed the existence of operational synergy after merger and acquisitions in Brazil, analyzing 74 operations between 1996 and 2004. Silva, Kayo, & Nardi (2016) evidenced abnormal stock returns for the acquirer listed at the top tier of corporate governance practices, where 100% of voting share is required to be floating.

In spite that, the Brazilian capital market has evidenced significant opportunities for future negotiations and must be considered differently from other countries. For instance, in a decade, while the developed economies were in crisis during 2007 and 2009, the Brazilian market faced intensive years of economic distress, at least on the short windows between 2008-09 and 2015-16, also concerning political changes. In 2019, the Brazilian stock exchange registered a record in number of new investors and in negotiation volume, responding to an expectation of credit recovery by the local and foreign investors, after significant economic changes (Lourenço, 2019). This uncertainty reduction is also understood as an opportunity for foreign companies to enter the Brazilian market through M&A process with more information.

Then, the decision of reorganize the firm must be carefully conducted. If the assumptions used on the valuation are not based upon a managerial, operational, and financial structure, the attempting to reorganize may fall flat, causing more distress to the acquirer than the status quo situation.

Firm life cycle stages and capital market

Recent studies in financial and accounting literature present a growing contribution of the firm life cycle to understand capital market issues (Al-Hadi, Hasan, & Habib, 2015; Dickinson, 2011; Hasan et al., 2015; Jenkins & Kane, 2004). Hasan et al. (2015, p. 48) state that “the firm life cycle has important implications in management and business strategy”.

The firm theory assumes that, during the life, a company interacts with many others interested agents to reach its goals (Miller & Friesen, 1980). In this sense, Dickinson (2011) concludes that the life of a firm is influenced by internal (strategy choices and financial resources) and external environments (sectorial and macroeconomic factors) and the life cycle of a firm can be segregated into introduction, growth, maturity, shake-out and decline stages.

Mueller (1972) reports the uncertainty to be the most inherent problem of an introducing firm. Then, it is the responsibility of the entrepreneur to make decisions to rapidly move away from this stage (Black, 1998; Jenkins & Kane, 2004). Reaching the growth stage is more important than profitability for a while, and this involves “information, intuition, courage or luck to make correct investment decisions in the face of uncertainty” (Mueller, 1972, p. 200).

Bender (2013, p. 126) complements that there is a compounded “business risk” associated with introducing firms based on “whether the company will gain an adequate market share to justify its involvement in the industry”. Then, despite the expected potential to growth, resource funding tends to be expensive, due to attracting only investors prepared to accept such risk. Then, this may be worthy under a closer investigation, requiring higher return instead.

Firm life cycle and M&A

Penrose (1959) posits that the M&A is associated with the growth of a firm because it assembles a choice of growing by recombining the old or building a new project/firm. Damodaran (2005) states that in emergent markets, there are relatively greater opportunities to acquiring potential growing firms; however, this negotiation is sensible to cash slack, because the absence of cash by the optimist acquirer would lead to more risk-taking (financial) in addition to the inherent operating risk. Then, mature firms are expected to make better negotiations than firms in other stages, resulting in more share of synergy derived from a presumed stable situation.

Moreover, Napier (1989, p. 273) called attention to the “lack of research linking motives to what happens after the merger, resulting in little information or knowledge about how mergers may, for different reasons, affect the subsequent structure or characteristics of the merged firms in the implementation stage”. This is also aligned with the deterministic theory of Structure-ConductPerformance (Bain, 1959), but the life cycle approach reassemble the reversal arguments of Porter (1980) that the current situation of the firm, including the performance, may conduct to a dynamic reorganization of the firm into the industry.

Recently, Fukuda (2020) finds a positive M&A effect on Tobin’s Q on the second year after the M&A for Japanese firms, but no effect on ROA in domestic deals. In fact, the results indicate a significantly negative effect on the first year after the event. The expected increase in ROA is significant only for international deals. In turn, Al-Sabri et al. (2020) find that size, sales growth, and stock return are positive associated with the likelihood to engage in an M&A in Malaysian firms. On the other hand, leverage, profitability, cash holding, and tangibility are negatively associated with the event.

Specifically, this negative signal of cash holding is contrary to the expectation as well as it casts double on the argument presented in this paper. Both the free-cash flow hypothesis and the cash-slack argument convey the expectation of greater financial situation and consequently less risk to pursue an M&A. Owen & Yawson (2010) find that mature firms are more propensity to engage in a M&A activity as acquirer and less propensity to a tender offer. And at the mature stage, the firms are expected to comparatively generate more cash flow from operating activities (Damodaran, 2005; Dickinson, 2011).

Moreover, Ames et al. (2020) recently examine the effect of firm life cycle stage on acquisitions, and find that acquirers in the declining stage are more likely to pursue diversifying acquisition than acquirers in other stages. However, both studies discuss the relation of M&A and firm life cycle under the market reaction approach, and then the subject remains anecdotal. Then, we expect the mature firms to have better internal structure, with greater ability to restore the industry and then create operating synergy.

Therefore, under the arguments presented, we test the following hypothesis:

H1: As acquirer, mature firms realize greater synergy than firms in other stages after a M&A activity.

Methods and econometric issues

Sample selection

We use data from firms listed at the Brazilian capital market between 2010 and 2017, according to the following procedures:

Table 1 Sample Selection

| Steps | Num. Obs. |

|---|---|

| All firms available on Comdinheiro® database. | 2,692 |

| Excluded: | |

| Firms without information of Cash Flow Statement | -567 |

| Firms without information of Assets | -127 |

| Firms from Financial Industry | -340 |

| Sample | 1,658 |

M&A negotiations data are collected from the ANBIMA (Brazilian Association of Finance and Capital Market Entities)’s database. This entity regulates, informs, and educates the capital market. ANBIMA is also responsible by certifying Qualified Investor Consultants (CPA 20), Hedge Funds and M&A with negotiation value greater than 20 million BRL. Consolidated Financial accounting data are collected on Comdinheiro® database.

Firm Life Cycle Stages

We use the Dickinson (2011)’s model to classify the firm into 5 life cycle stages (introduction, growth, mature, shake-out and decline), using a combination of the Cash Flow Statements signals, as presented by the Panel 1:

Panel 1 Combination of cash flow signals

| Cash Flow | Intro | Growth | Mature | Shake-out | Decline | |||

|---|---|---|---|---|---|---|---|---|

| From Operating Activities | - | + | + | - | + | + | - | - |

| From Investing Activities | - | - | - | - | + | + | + | + |

| From Financing Activities | + | + | - | - | + | - | + | - |

Source: Dickinson (2010, p. 9)

Dickinson (2011) highlights that a benefit of this proxy “is that it uses the entire financial information set contained in operating, investing, and financing cash flows statement rather than a single metric to determine firm life cycle”. The growing use of the metric is observed in international (Bhattacharya et al., 2020; Drake, 2013; Hasan et al., 2015; Hasan & Habib, 2017a) and in national (Brazilian) studies (Almeida & Novaes, 2020; Costa et al., 2014; Novaes et al., 2016; Oliveira & Girão, 2018).

Synergy

The literature is not consistent about the best proxy for “synergy” or “value creation” after the M&A. Following Damodaran (1995), we assume the synergy to increase the value to shareholder via both operating and financial perspective. The first one increases the expected future cash flow and second one may reduce the rate of expected return. Then, we firstly use the Return on Investment (ROI), traditionally used for both practitioners and academics, as a proxy for Synergy (𝑆𝑦𝑛):

We use the total asset in end of the fiscal year, to absorb any change on the size during the year. Additionally, we use the net income to ensure the effect of operating results added to results in subsidiaries and financial decision (cost of debt) on the index. Moreover, we use consolidated information, prepared under the International Financial Standards (IFRS). In robustness checks, we switch the ROI for other performance measures.

Then, to test the hypothesis of comparatively greater synergy of acquirer in mature stage, we firstly run a Propensity Score Matching procedure to identify a control group comprising firms that has not passed through an M&A process (on the period), but with other same characteristics (year, size, and industry concentration level), to be compared with those which has engaged in such a reorganization.

Secondly, we run the following regression model:

Where

Beyond the control for size, we also control for year and industry effects. Hence, ceteris paribus, mature acquirers that engage in M&A process are expected to significantly create synergies, by increasing the operational return of the firm.

Results

Descriptive Results

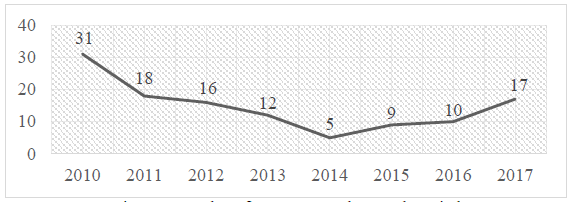

The Figure 1 shows the number of negotiations in which Brazilian listed firms were the acquirer. Despite the evidence, the ANBIMA registered a mean of 150 negotiations per year, totaling 1.197 M&As between 2010 and 2017, but a relevant portion of those information is not published by both parts. Moreover, only 10% of the negotiations are headed by a listed public firm, which limits our analysis.

The conglomerate Hypermarcas (HYPE3) is the firm with the greater number of acquisitions, being 6 in 2010, 3 in 2011 and 2 in 2016. VALE3 follows it with 5 acquisitions in 2011, 1 in 2014 and 2 in 2017. Moreover, BrMalls (BRML3) calls the attention due to the frequency of M&A on the period: the firm has acquired 8 firms, but the acquisitions are distributed on the period of analysis. These scenarios enable a separate analysis, but difficult the main objective of this paper as well, since there is a short period to be considered as “post-M&A”.

Table 2 shows the distribution of M&A across the life cycle stages:

Table 2 Frequency of M&A across life cycle stages

| M&A | Life Cycle Stages | Total | ||||

|---|---|---|---|---|---|---|

| Introduction | Growth | Mature | Shake-Out | Decline | ||

| 0 | 152 | 376 | 617 | 160 | 87 | 1,392 |

| 1 | 8 | 23 | 24 | 5 | 3 | 63 |

| Total | 160 | 399 | 641 | 165 | 90 | 1,455 |

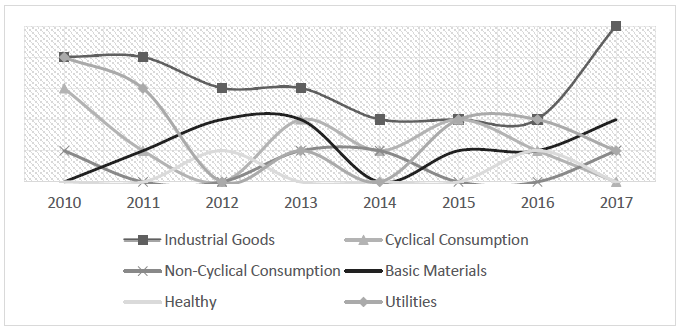

Consistent with the literature, there is a greater number of firms in growth and mature stages, with relative superior incidence of M&A in these stages compared to the others. Figure 2 shows the frequency of M&A across the Brazilian industries in this period:

We observe that industrial goods concentrate the most incidence of M&As, followed by Utilities and Cyclical Consumption. It is also possible to observe that while there is an increase in Industrial Goods from 2010 to 2014, the negotiations in Basic Materials increased until 2013, decreased in years of intensive distress, but increased again in 2017. In the Cyclical Consumption industry, the opportunities are more pronounced between the 2013-2015.

Propensity Score Matching (PSM)

The PSM is a technique that enables a fair comparison between groups, by estimating a matched (control) group. By year, we control for size, and by the industry concentration level to estimate the probability of a firm to engage in a M&A operation, using a Probit model. Firstly, Table 3 shows the distribution information for the metric variables to be used in this procedure, segregated into treatment group (dummy of M&A: d_ma=1) and the “overall control group” (d_ma=0):

Table 3 Descriptive Analysis of metric variables of treatment and control group

| Panel A: d_ma = 0 | |||||

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| ROI | 1,389 | -0.0029273 | 0.3 | -8.257 | 4.07308 |

| Size | 1389 | 21.56187 | 1.8 | 11.81 | 27.44652 |

| HHI_RL | 1,389 | 0.2875629 | 0.2 | 0.094 | 1 |

| Panel B: d_ma = 1 | |||||

| ROI | 63 | 0.02208 | 0.1 | -0.343 | 0.1455791 |

| Size | 63 | 23.76403 | 1.7 | 19.81 | 27.52581 |

| HHI_RL | 63 | 0.3146116 | 0.1 | 0.1 | 0.5803794 |

Notes: roi is the total return on investments; size is the natural logarithm of total asset in end of the fiscal year; year is a dummy variable; and hhi_rl is the Hirfindhal-Hirshman Index of concentration, using the Net Revenue.

Caution is needed here once the segregation enables a firm to appear in both groups in different years. Additionally, we observe negative ROI values for both groups (minimum values). We decided not to drop at this step, to further investigate in robustness check. The number of M&A on the sample represents about 4% of the total, and the control group was extracted from these 1,389 observations.

There are different options of extraction, and we used the type “Nearest Neighborhood”, which calculates the probability in blocks. After that, an algorithm finds the same propensity on the control group. Table 4 shows the estimated propensity for the treatment group:

Table 4 Estimated propensity for the treatment group

| Estimated propensity | score | |||

|---|---|---|---|---|

| Percentiles | Smallest | |||

| 1% | 0.004277 | 0.0040711 | ||

| 0.05 | 0.0052987 | 0.0040799 | ||

| 10% | 0.0066788 | 0.0040816 | Obs | 1205 |

| 0.25 | 0.0121376 | 0.0040914 | Sum of Wgt. | 1,20 |

| 50% | 0.029427 | Largest | Mean | 0.0519045 |

| 0.75 | 0.0668132 | 0.5202192 | ||

| 90% | 0.1130422 | 0.5292591 | Variance | 0.0045838 |

| 0.95 | 0.1574435 | 0.5342072 | Skewness | 3.589664 |

| 99% | 0.4002167 | 0.5367422 | Kurtosis | 20.40035 |

The procedure creates a new variable (“pscore") with a distinct distribution. We observe that this variable is asymmetric, with heavy tails. However, this procedure is needed only to find the control group. Table 5 show the propensity estimation according to the variable mentioned before:

Table 5 Probit model estimations

| d_ma | Coef. | Std. Err. | z | P>z |

|---|---|---|---|---|

| size | 0.3431315 | 0.0407243 | 8.43 | 0.000 |

| year | -0.0593529 | 0.0287006 | -2.07 | 0.039 |

| hhi_rl | 0.8061405 | 0.4261924 | 1.89 | 0.059 |

| _cons | 109.8079 | 57.67016 | 1.9 | 0.057 |

According to the p-value of the Z-distribution, it is possible to ensure that the probability of a firm engage in a M&A operation have decreased along the period of analysis. Moreover, the propensity is positively associated with the industry concentration level, and with firm size. Additionally, the algorithm found 6 blocks as necessary to ensure that the mean propensity score is not different for treated and controls in each block. Table 6 shows the inferior bound, the number of treated and the number of controls for each block:

Table 6 Inferior of block of pscore

| Inf.of block of pscore | d_ma | Total | |

|---|---|---|---|

| 0 | 1 | ||

| 0.0040711 | 527 | 7 | 534 |

| 0.025 | 255 | 9 | 264 |

| 0.05 | 232 | 17 | 249 |

| 0.1 | 100 | 18 | 118 |

| 0.2 | 21 | 6 | 27 |

| 0.4 | 7 | 6 | 13 |

| Total | 1,142 | 63 | 1,205 |

Despite the difference in number of observations, the procedure finds a proper control for each block without losing a significant number of observations. It is also observed that the highest probability found for the treatment group is comparable by only 7 firms on the control groups. Therefore, another variable is created (comsup), which means a common support. This dummy variable receives zero if the firm is not comparable. Then, the following procedures include the condition of “comsup” equals to 1, and then the number of observations decreases to 1,205 (control plus treatment group).

Linear Regression Estimations Results

To estimate the differences-in-differences model, we test the possible approaches for panel data. The results are presented in Table 7:

Table 7 Tests for Panel Data

| Tests | |||

|---|---|---|---|

| Chow | Breusch-Pagan | Hausman | |

| H0: | Pooled | Pooled | RE |

| Ha: | FE | RE | FE |

| Stat | F (183, 1017) = 1.24 | chibar2 (01) = 3.50 | chi2(4) = 1.52 |

| p-value | 0.0262 | 0.0307 | 0.8226 |

In short, assuming an alfa of 1% we did not reject the null hypothesis of nonsignificant specific error term (ci) in Chow test. In turn, Breusch-Pagan test shows a p-value (0.0307) lower than the alfa of 1%, which signalize a constant variance of these specific residuals. Presumably, the Hausman test (0.8226) did not reject the null, indicating the Random effects would be superior, compared to the Fixed Effects. However, we select the estimator relied on the Chow test results. Therefore, we follow the traditional OLS model (pooled) and the results are shown in Table 8.

Table 8 Regression Results

|

| ||||

| Variables | (1) OLS |

(2) White |

(3) Ctrl 1 |

(4) Ctrl 2 |

| Post_M&A | -0.0429* | -0.0429** | -0.0451** | -0.0422** |

| (-1.650) | (-2.367) | (-2.417) | (-2.139) | |

| Mature | -0.000409 | -0.000409 | -0.000746 | -0.0146 |

| (-0.00592) | (-0.0233) | (-0.0332) | (-0.771) | |

| Post_M&A*Mature | 0.0300 | 0.0300 | 0.0323 | 0.0462 |

| (0.343) | (1.068) | (1.019) | (1.533) | |

| Size | 0.00716* | 0.00716*** | 0.00693*** | 0.00873*** |

| (1.903) | (2.981) | (2.670) | (3.143) | |

| Constant | -0.136 | -0.136** | -0.124** | -0.132** |

| (-1.636) | (-2.455) | (-2.093) | (-2.172) | |

| Num of Observation | 1,205 | 1,205 | 1,205 | 1,205 |

| R2 | 0.40% | 0.40% | 1.40% | 2.30% |

| Adjusted R2 | 0.11% | 0.11% | 0.34% | 0.65% |

| F-test | 1.335 | 2.999** | 2.763*** | 3.733*** |

| Industry Control | No | No | Yes | Yes |

| Year Control | No | No | No | Yes |

Notes: t-statistics in parentheses; *** p<0.01, ** p<0.05, * p<0.1.

We anticipate that after estimation of the OLS model, we i) observed a VIF mean of 2.15, that indicates low level of multicollinearity; ii) tested - and did not rejected - the null hypothesis of correct model specification (Ramsey test: 0.3044); iii) though, we rejected the null hypothesis of constant variance of errors (prob>chi2: 0.0003). Therefore, we focus the analysis on the model with White’s estimator of robust standard-errors to treatment of heteroscedasticity (Column 2), also controlling for industry (Column 3) and both industry and year (Column 4). Column 1 is presented only for comparison.

In short, the results are qualitatively the same among the estimators 2, 3 and 4. Post_M&A is a time dummy variable the captures the years after the M&A operation. The coefficient is negatively significant at 5%, which means that, on average, the total Return on Investment decreases after the M&A. Additionally, Mature is the dummy variable that receives one if the firm (the object) is classified at mature stage in each year. Such coefficient is not significant, indicating that, ceteris paribus, on average, there are no differences in terms of total return on investments between mature firms and firms in other life cycle stages.

Finally, the variable Post_M&A*Mature (the diff-in-diff coefficient) captures the effect of both variations (object and time), but the coefficient is not statistically significant for none of the 4 estimators. The only significant variable is Size , signaling that the greater the firm, the greater the total return, regardless the merger and acquisition. This is consistent with the economy of scale (Silberston, 1972), once the greater structure might represent higher fixed cost, which comparatively reduces the total unit cost, by means of the operating leverage (França & Lustosa, 2011; Mandelker & Rhee, 1984).

Robustness Checks

We have first considered M&A operation in any year, then the periods after received value 1. Afterwards, we controlled for windows of short (1 year), medium (3 years) and long terms (5 years) after the M&A, but the results are qualitatively the same. We tested alternative proxies for synergy, dropping negative values of ROI, winsorizing it at 2.5% in each tail. We also used the random effect estimators, but the results did not change.

Alternatively, we switched the Net Income for EBIT (Earnings Before Interest and Taxes), but nothing was found to be significant. In addition, we used the first and second lagged return on investment as independent variable, but the result for the diff-in-diff coefficient is qualitatively the same.

We also included a dummy variable to capture periods of financial distress on the economy, proxied by the negative variation on the GDP (Opler & Titman, 1993). Then, a dummy received the value 1 if year equals 2015 or 2016 for economic crisis in Brazil. This variable was tested alternatively on the Probit model and the regression model, but the results remain identical.

In further investigations, we also considered the possibility of life cycle stage transition after the M&A and then we tested the effect only for those firms, and not for the stage. However, the decrease of observations restricts the analysis. Afterall, we also investigated it by each life cycle stages and nothing different was found.

Concluding Remarks

We investigated the role of life cycle stage in the synergy creation after a merger and acquisitions in the Brazilian setting between 2008 and 2017. The literature advocates that an opportunity of M&A emerges from an optimistic view from the bidder in purchasing firms to create value to investors, among other motives, by reducing the total unit cost, which enhances the total return. We argue that mature firms are more prepared in terms of cash slack, environment, and are expected to present a stable structure and business model (Damodaran, 2005; Mueller, 1972).

We then assume the firm life cycle to play a separating equilibrium role on the pursuing of synergy and hypothesized that after the M&A, mature firms would increase the total return on investment. Nevertheless, using the PSM to estimate a control group by year, size, and the industry concentration level, we found no significant result for the comparison between mature firms and firms from other stages. Therefore, we refute the research hypothesis that, as acquirer, mature firms realize greater synergy than firms in other stages after a Merger & Acquisition activity. At least in Brazil in the period of analysis, it could not be confirmed according to the results in this research. Instead, we observe an overall decrease in term of return on investment after M&As.

The national literature is weak in presenting results derived from M&As. Studies such as Camargos & Barbosa (2009) and Oliveira (2016) find significant operating synergy. However, we understand that the synergy of a group concerns the operational income plus the results in subsidiaries. Neither of them has isolated potential effects of other phenomena by creating a matched group, which can disturb the analysis. Then, this research innovates in presenting evidence about this global return, through a comparative instrument of analysis.

Taking into account the several robustness check, the insignificant effect of our interesting variable might be explained by the arguments of Bradley & Korn (1984), Napier (1989) and Roll (1986), that non-financial factors can negatively influence the realization of the synergy (i.e. hubris, employee’s motivation, management turnover and other agency conflicts). Teece & Pisano (1994) advocates that “the properties of internal organization cannot be replicated by a portfolio of business units amalgamated through formal contracts as the distinctive elements of internal organization simply cannot be replicated in the market”. Additionally, they agree with the role of the organizational structure and managerial process, which refers to certain items eventually out of the balance sheet to generate productivity and efficiency.

Under the perspective of hubris, Morck et al. (1990) argue that good performing firms are most likely to be affected by such a overconfidence. This may incur in a value-destruction once more financial resources are paid at the shareholders expenses. In addition, Rezende & Macedo (2020) recently find that slack has weak influence on organizational growth at the Brazilian setting.

Hence, this paper shed light on this stream of work, incentivizing more instrumentalized studies to both enhance the quality of the literature and to provide relevant micro and macro factors to be studied by potential investors and other stakeholders, such as financial market analysts and underwriters, before embarking on a M&A activity. Subsequent studies can further investigate such situation by controlling for cross-border acquisition (Fukuda, 2020; Ghosh & Ghosh, 2014; Vennet, 1996) institutional investors participation (Andriosopoulos & Yang, 2015; Faelten et al., 2015; Ghaly et al., 2020), financial deal advisors (Chahine & Ismail, 2009; Hayward, 2003).