Temporary stabilization: a Fréchet-Weibull extreme value distribution approach

Francisco Venegas-Martínez1, Francisco Ortiz-Arango2, Ambrosio Ortiz-Ramírez3

1 Escuela Superior de Economía, IPN, E-mail: fvenegasini@yahoo.com.mx.

2 Escuela de Ciencias Económicas y Empresariales, Universidad Panamericana, E-mail: fortizar@up.edu.mx.

3 Escuela Superior de Economía, IPN, E-mail: a7ortiz@gmail.com.

]]> Recepción: 16/11/2010.

Abstract

This paper develops, in a small open economy of pure exchange framework, a stochastic model of exchange-rate-based inflation stabilization plan that is expected to be temporary. Agents have expectations of devaluation driven by a mixed diffusion-jump process where the expected size of a possible devaluation is supposed to have an extreme value distribution of the Fréchet-Weibull type. Consumption and wealth equilibrium dynamics are examined when such a stabilization plan is implemented. It is assumed that financial markets are incomplete, that is, there are more risk factors than risky assets. Finally, the effects of exogenous shocks on economic welfare are assessed.

Keywords: inflation stabilization, extreme values.

JEL Classification: F31, F41.

Resumen

Esta investigación desarrolla, en el marco de una economía pequeña y abierta, un modelo estocástico de un plan de estabilización de precios que toma como un ancla nominal al tipo de cambio y en donde se espera que dicho plan sea temporal. Los agentes tienen expectativas de devaluación conducidas por un proceso mixto de difusión con saltos en donde el tamaño esperado de una posible devaluación tiene una distribución de valores extremos del tipo Fréchet-Weibull. Las dinámicas de equilibrio del consumo y la riqueza son examinadas cuando un plan de estabilización es implementado. Se supone que los mercados financieros son incompletos, es decir, hay más factores de riesgo que activos riesgosos. Por último, se evalúan los efectos de choques externos en el bienestar económico.

]]>Introduction

Between 1900 and 2000, emerging economies managing a fixed exchange-rate, a fixed rate of devaluation, an adjustable band or a convertibility plan, like Brazil, Ecuador, Thailand, Korea, Indonesia, Russia, Bosnia, Turkey, among others, had a major financial crisis. These regimes have simply not proved viable over time, especially for countries integrated or integrating into international capital markets. In most cases, the public in these countries anticipated that the stabilization plan was going to be temporary, resulting in a large expansion of consumption of durable goods and an extreme devaluation. Surprisingly, in 2008, as of April 31, according to the IMF, at least 88 of the world countries have one of the above exchange-rate regimes, as it is shown below in Table 1. The lessons, from these episodes, that should be taken into account by policymakers when devising a corrective devaluation, especially if financial markets are incomplete, is that public expectations and consumption dynamics generated by exchange-rate-based stabilization plans may increase imports producing unsustainable deficit in the current account of the balance of payments.

The experience in most of these countries brings the credibility of stabilization programs to our attention. In most cases, the public was skeptical about government's commitment to defend a regime where the exchange rate was taken as a nominal anchor. In many cases, the final outcome was a consumption boom and an extreme devaluation putting an end to an exchange-rate-based stabilization program.4

In Calvo and Reinhart's (2002) paper "Fear of floating", it has emphasized that many countries that claim to have floating exchange rates do not, in practice, allow the rate to float freely, but instead use interest rate and intervention policies to affect its behavior. From this, they draw two conclusions: in first place, that it is incorrect to claim that countries are moving away from adjustable-peg systems. Secondly, that since countries hanker after fixed exchange rates for good reasons, they would be well advised to adopt hard pegs. In their paper, Calvo y Reinhart also investigate whether countries are, indeed, moving as far to the corners as official labels suggest. Since verifying the existence of a hard peg is trivial, their focus is on the other end of the flexibility spectrum. Specifically, they examine whether countries that claim they are floating their currency are, indeed, doing so.

Policymakers now warn against the use of a fixed rate of devaluation or an adjustable band in countries open to capital flows. This belief that intermediate regimes between fixed exchange-rate and free floating are unsustainable is known as the bipolar view (see, for instance, Fischer, 2001). The proportion of IMF members with intermediate arrangements fell during the 1990s, while the use of hard pegs and more flexible arrangements grow. Also, Table 2 shows the evolution of de facto exchange -rate arrangements.

Studies in the literature on temporary stabilization based on a semi fixed exchange-rate that have considered a stochastic setting are, for instance, Drazen and Helpman (1988) examining stabilization with exchange-rate management under uncertainty, Calvo and Drazen (1997) contemplating uncertainty in the permanence of economic reforms,5 and Mendoza and Uribe (1996) and (1998) modeling exogenous and endogenous probabilities of devaluation, respectively. On the other hand, Venegas-Martínez (2000) and (2001), (2006a) has studied exchange-rate-based stabilization with imperfect credibility; Venegas-Martínez (2006b) has examined the impact of fiscal policy exchange-rate-based stabilization with imperfect credibility, and Venegas-Martínez (2010) has valued the real option of waiting when consumption can be delayed in exchange-rate-based inflation stabilization program. It is also important to highlight the work of Uribe (2002) and Uribe and Mendoza (2000) regarding the explanation of the order of magnitude of the unexpected consumption booms and the incorporation of uncertainty in the analysis of temporary stabilization plans. Also, in Mendoza (2001) the benefits of dollarization when the stabilization policy lacks credibility and financial markets are imperfect are examined. Finally, Akgiray and Booth (1988) have made clear that both monetary policy and targets involve different parameters of the exchange-rate distribution, this in the spirit of the Lucas' critique.

While the above literature has provided considerable theoretical advancement, there are some issues on credibility and uncertainty that still need to be explained, as remarked in: Helpman and Razin (1987), Kiguel and Liviatan (1992), Végh (1992), and Rebelo and Végh (1995). First, in the existing models, it is missing a plausible explanation of the lack of credibility. Secondly, most models forget that what makes a stabilization inflation program temporary is uncertainty.

This paper develops, in small open economy setting, a stochastic model of exchange-rate-based stabilization recognizing the role of extreme movements in the dynamics of the expectations of devaluation. It is assumed that the expectations of devaluation follow a mixed diffusion-jump process where a Brownian motion drives the rate of devaluation and a Poisson determines the number of possible devaluations. The expected size of a possible devaluation is supposed to have an extreme value distribution of the Fréchet-Weibull type. It is important to point out that incorporating an extreme value distribution of the Fréchet-Weibull type for the exchange-rate stochastic dynamics extends the work in Venegas-Martínez (2000) and (2006a).

In the framework of partial equilibrium, the proposed model will assume that contingent-claims markets for hedging against devaluation are unavailable. In this context and assuming logarithmic utility, which provides risk-averse agents, we shall examine the equilibrium dynamics of consumption and real wealth when a stabilization program is implemented and the size of devaluation is expected to follow an extreme value Fréchet distribution. We shall also study the effects on economic welfare and consumption of once-and-for-all changes in the parameters determining the expectations. The model is developed under the following two main assumptions: the revenue raised by seignorage is not rebated back to the agents and policy variables are stochastic. Finally, it is important to mention that the proposed model derives tractable closed-forms solutions that make much easier the understanding of the key issues in the analysis of temporary stabilization when the expected size of a possible devaluation is supposed to have an extreme value distribution.

]]> This research is organized as follows. In the next section, we work out a one-good, cash-in-advance, stochastic model where a representative agent has expectations of devaluation driven by a mixed diffusion-jump process where the expected size of a possible devaluation is supposed to have an extreme value distribution. Through section 3, we solve the consumer's decision problem. In section 4, we undertake several policy experiments through comparative statics exercises. In section 5, we examine the impact of exogenous shock on economic welfare. In section 6, we study the dynamic behavior of wealth and consumption, and address a number of exchange-rate policy issues. Finally, in section 7, we present conclusions, acknowledge limitations, and make suggestions for further research.

Structure of the economy

In what follows, we set up the characteristics of the economy under study. The behavior of both the exchange rate and the available assets will be introduced.

Exchange rate dynamics

In order to derive solutions which are analytically tractable, the structure of the economy will be kept as simple as possible. Let us consider a small open economy6 with a single infinitely lived consumer in a world with a single perishable consumption good. We assume that the good is freely traded, and its domestic price level, Pt, the purchasing power parity condition, namely

Where P*t is the foreign-currency price of the good in the rest of world, and et is the nominal exchange rate. Throughout the paper, we will assume, for the sake of simplicity, that P*t is equal to 1. We also assume that the exchange-rate initial value, e0, is known and equal to 1.

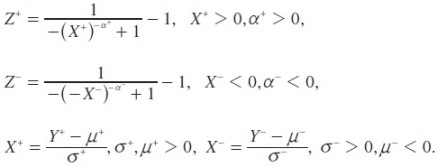

In what follows, we will suppose that the ongoing uncertainty in the dynamics of the expected rate of devaluation, and therefore in the inflation rate, is generated by the following process geometric Brownian motion combined with Poisson jumps of a random sizes driven by extreme value distributions of the Fréchet-Weibull type:

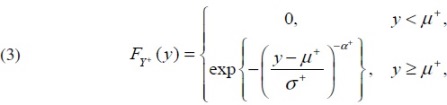

We also suppose that Y+ is an extreme value Fréchet random variable with parameters α+, µ+ and σ+ > 0, that is, Y+ has cumulative distribution function given by

and Y- is an extreme value Weibull random variable with parameters α- and µ- < 0, σ- > 0, that is, Y- has cumulative distribution function defined by

The corresponding densities satisfy

and

Figure 1 shows a Weibull and a Fréchet densities with given parameter values.

Notice now that if σ+ > 2, then

Expressions for E [Y-], E [(Y-)2 ] , and Var [Y-] are similar to that given above. On the other hand, since the number of expected devaluations (i.e., upward jumps in the exchange rate) per unit of time follows a Poisson process dN+t with intensity λ+ , we have that

and

so that

Assets available in the economy

The representative consumer holds two real assets: real cash balances, mt = Mt/Pt, where Mt is the nominal stock of money, and an international bond, bt. The bond pays a constant real interest rate r (i.e., it pays r units of the consumption good per unit of time). Thus, the consumer's real wealth, at, is defined by

where the initial real wealth a0 is exogenously determined. Although this is a limitation of the proposed model, this will be used to think of the decision making process of the representative agent as a stochastic optimal control problem in continuous time. Furthermore, we assume that the rest of the world does not hold domestic currency. Consider a cash-in-advance constraint of the Clower type:

where ct is consumption, and ψ-1 > 0 is the time that money must be held to finance consumption. Condition (6) is critical in linking exchange-rate dynamics with consumption. Observe that

In the sequel, we will assume that the error o(ψ-1) is negligible. In this case, devaluation acts as a stochastic tax on real cash balances.

]]> The stochastic rate of return of holding real cash balances, drm, is simply the percentage change in the price of money in terms of goods. By applying Ito's lemma to the inverse of the price level, with (2) as the equation driven the underlying process (see, for instance, Venegas-Martínez, 2008), we get

Hence, the stochastic rate of return of holding real cash balances, dRm, is given by

The consumer's choice problem

The stochastic consumer's real wealth accumulation in terms of the portfolio shares wt = mt/at, 1 - wt = bt/at, and consumption, ct, is given by

with a0 exogenously determined. Thus,

The von Neumann-Morgenstern utility at time t = 0, V0, of the competitive risk-averse consumer is assumed to have the time-separable form:

where E0 is the conditional expectation on all available information at t = 0. To avoid unnecessary complex dynamics in consumption, we assume that the agent's subjective discount rate has been set equal to the constant real international interest rate, r. We consider the logarithmic utility function in order to derive closed-form solutions and make the analysis tractable.

First order conditions for a an interior solution

The Hamilton-Jacobi-Bellman equation for the stochastic optimal control problem of maximizing utility, with log(ct) = log(Ψatwt), and assuming that Y+ and Y- are stochastically independent of dNt+ and dNt-, respectively, is given by (see, for instance, Venegas-Martínez, 2008).

The first-order condition for an interior solution is:

Given the exponential time discounting in (10), we postulate I (at, t) in a time-separable form as:

]]>

where β0 and β1 are both to be determined from (11). In this case, we obtain

Where

Notice that the arguments in the logarithmic function above are both positive. We compute the first-order conditions by using

In this case, we find that wt Ξ w is time-invariant and

By defining the change of variable

]]>

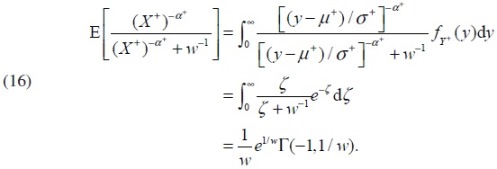

the first expectation can be written as

where

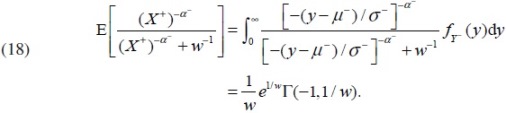

and, for small w , in fact for 0 < w < 1, we have the following approximation:

where Γ ( .,. ) is the upper incomplete Gamma function. Similarly,

Hence, from (16), (17) and (18), the first order condition can be written as

]]>

where λ = λ+ - λ- . Figure 2 shows the graph of the function Γ ( 0,1 / w).

If we assume that 0 < w < 1 and use (17), then we may leave out the error term and write the first order condition as

Once an optimal w is chosen, coefficients β0 and β1 are determined as follows

or

which leads to

Thus,

which is a quadratic homogeneous equation with real solutions

and

Notice that always 0 < ψ + µ + λ and that iff

Policy experiments and comparative statics

In this section, we carry out some comparative statics experiments regarding the optimal share w+. We will see the effects of changes in the mean expected rate of inflation μ, the instantaneous volatility of inflation and the total intensity parameter λ on w+. By differentiating the first order condition, we get

where

We are now in a position to derive our first result: a once-and-for-all increase in the rate of devaluation, which results in an increase in the future opportunity cost of purchasing goods, leads to a permanent decrease in the proportion of wealth devoted to future consumption. To see this, it is enough to use (23) to find that

Notice also that a once-and-for-all increase in the inverse of the variance of the diffusion component will produce a contrary effect to that of ¡ on w+ since

]]>

In other words, the consumer sets aside a larger proportion of wealth to maintain real monetary balances to finance consumption, in order to deal with a higher variance in consumption prices.

Another result is the response of the equilibrium share of real monetary balances, w+ to once-and-for-all changes in the total-intensity parameter, λ. A once-and-for-all increase in the expected number of extreme devaluations per unit of time causes an increase in the future opportunity cost of purchasing goods. This, in turn, permanently decreases the proportion of wealth set aside for future consumption. From (11), we get

Impact on economic welfare

We will now assess the effects of exogenous shocks on economic welfare. As usual, the welfare criterion, W, of the representative individual is the maximized utility starting from the initial real wealth, a0. Therefore, welfare is given by

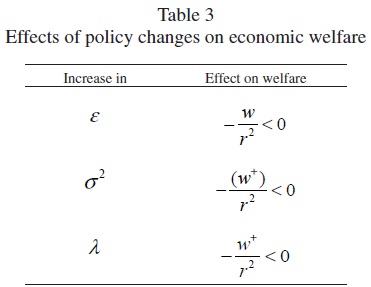

Table 3 shows the impacts on welfare of once-and-for-all changes in the mean expected rate of devaluation, the inverse of volatility, the probability of devaluation, and the expected size from devaluation.

]]>

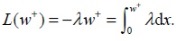

In order to compute economic welfare W, we need to find, explicitly, L(w+). To this end, we use the same change of variable as in (16), so

It is important to point out that (16) can be also obtained by differentiating (28)

Notice also that since there is a differentiation process of L(w+) in the first order condition, we may use now the approximation Γ(0,1 / w+) = we-1/w (1 + O(w)), thus

Wealth, consumption and dynamic implications

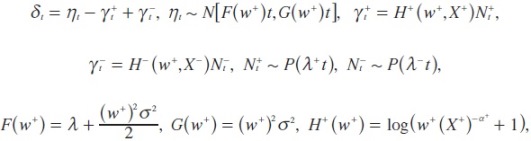

We now derive the stochastic process that generates wealth when the optimal share is applied. After substituting the optimal share w+ into (9), we get

]]>

The solution to the above stochastic differential equation, conditional on a0, is

where

and

Notice that

In virtue of (6), the stochastic process for consumption, in (30), can be written as

]]>

This indicates that, in the absence of contingent-claims markets, the devaluation risk has an effect on wealth via the uncertainty in δt, that is, uncertainty changes the opportunity set faced by the consumer. On the other hand, the devaluation risk also affects the composition of portfolio shares via its effects on w+. Thus, a policy change will be accompanied by both wealth and substitution effects. We cannot determine the level of consumption in our stochastic framework. We can only compute the probability that, at a given time, a certain level of consumption occurs. Notice, however, that by Jensen's inequality, mean consumption satisfies:

In contrast with our stochastic setting, ct+ shows a dynamic behavior, even if the rate of devaluation were expected to remain fixed forever. This is because δt is a time-varying, state-contingent variable. We may conclude that uncertainty is the clue to rationalize richer consumption dynamics that could not be obtained from deterministic models.

Consumption booms

Next, we will analyze a policy of the form:

where T is exogenously determined, and ε1 < ε2, as in Calvo (1986). Notice that in our stochastic setting, there is a lack of credibility even if we do not change the four parameters since agents always assign some probability to the event of currency devaluation. Let us examine the response of consumption to (33). From (32), we may write

where hT (Δ; ε1, ε2) Ξ exp{-δT( ε1 ) - δTΔ ( ε1 ))} tends to 1 as Δ → 0+ a.s. (almost surely). The limit means that although the stationary components of the parameters of ηt and γt are different before and after time T , such a difference becomes negligible when Δ → 0+ . Consequently,

]]>

We also notice that w2+ / w1+ < 1, together with (34), imply  a.s., indicating a jump (boom) in consumption at time T . If ε were to be constant forever, i.e., if εt = ε2 for all t > 0, then we would have

a.s., indicating a jump (boom) in consumption at time T . If ε were to be constant forever, i.e., if εt = ε2 for all t > 0, then we would have

On the right-hand side of (35), the factor ht ( Δ; ε1, ε2 ) → 1 as Δ → 0+ a.s. Hence, consumption would be continuous a.s. for all t. If the plan is expected to be temporary, then a.s., indicating a jump in consumption at T, as we have shown

Conclusions

The "credibility literature" has by now exhausted a class of deterministic models aimed at explaining consumption dynamics. Most of the existing models ignore uncertainty providing a very elaborate economic interpretation of why uncertainty needs to be considered. After all, what produces expected temporariness is uncertainty. We have presented a stochastic model of exchange-rate-based stabilization with imperfect credibility where agents have expectations of devaluation driven by a mixed diffusion-jump process and the expected size of a possible devaluation is supposed to have an extreme value distribution of the Fréchet-Weibull type. An important feature of our formulation is that there is a lack of credibility even if we do not change the parameters determining the expectations of devaluation. By using a logarithmic utility, we have derived closed-form solutions to examine the dynamic implications of uncertainty. These explicit solutions have made much easier the understanding of the key issues of temporary programs.

Our stochastic framework, in which a Poisson process drives the expectations of devaluation and the expected size of a possible devaluation is supposed to have an extreme value distribution of the Fréchet-Weibull type, provides new elements to carry out comparative statics experiments and empirical research on some observed regularities in temporary stabilization that still need to be explained.

The broad message of this paper, although only demonstrated for a particular case of utility index, is that public expectations and consumption dynamics generated by exchange-rate-based stabilization plans are linked through fragile relationships. Therefore, policymakers should consider these elements with great caution when devising a corrective devaluation, especially if contingent-claims markets are absent.

It is worthwhile mentioning that the results obtained strongly depend on the assumption of logarithmic utility, which is a limit case of the family of constant relative risk aversion utility functions. The extension of our stochastic analysis to such a family does not provide closed-form solutions, and results might be only obtained via numerical methods. Needless to say, additional research is required in this direction.

]]> The model can be obviously extended in several ways, for instance, more research should be undertaken in adding both non tradable and durable goods; this, of course, will provide more realistic assumptions. This extension will lead to more complex transitional dynamics, but results will certainly be richer.

References

Akgiray, V. and G. G. Booth (1988). Mixed Difussion-Jump Process Modeling of Exchange Rate Movements, The Review of Economics and Statistics, Vol. 70, No. 4, pp. 631-637. [ Links ]

Calvo, G. A. and C. Reinhart (2002). Fear of Floating, Quarterly Journal of Economics, Vol. 107, No. 2, pp. 379-408. [ Links ]

Calvo, G. A. (1986). Temporary Stabilization: Predetermined Exchange Rates. Journal of Political Economy, Vol. 94, No. 6, pp. 1319-1329. [ Links ]

Calvo, G. A. and A. Drazen (1998). Uncertain Duration of Reform: Dynamic Implications. Macroeconomic Dynamics, Vol. 2, No. December, pp. 443-455. [ Links ]

Calvo, G. A. and C. A. Végh, (1998). Inflation Stabilization and Balance-of-Payments Crises in Developing Countries, in: J. Taylor and M. Woodford, eds., Handbook of Macroeconomics, North Holland. [ Links ]

Drazen, A. and E. Helpman (1988). Stabilization with Exchange Rate Management under Uncertainty, in: E. Helpman, A. Razin, and E. Sadka, eds., Economic Effects of the Government Budget. MIT Press, Cambridge, MA. [ Links ]

Fischer, S. (2001). Exchange Rate Regimes: Is the Bipolar View Correct? Journal of Economic Perspectives, Vol. 15, No. 2, pp. 85-106. [ Links ]

Helpman, E. and A. Razin (1987). Exchange Rate Management: Intertemporal TradeOffs. American Economic Review, Vol. 77, No. 1, pp. 107-123. [ Links ]

Kiguel, M. and N. Liviatan (1992). The Business Cycle Associated with Exchange-Rate-Based Stabilization. The World Bank Economic Review, Vol. 6, No. 2, pp. 279-305. [ Links ]

Mendoza, E. G. (2001). The Benefits of Dollarization when Stabilization Policy Lacks Credibility and Financial Markets are Imperfect. Journal of Money, Credit and Banking, Vol. 33, No. 2, pp. 440-474. [ Links ]

Mendoza, E. G. and M. Uribe (1996). The Syndrome of Exchange-Rate-Based Stabilization and Uncertain Duration of Currency Pegs. International Finance Discussion Paper No. 548, Board of Governors of the Federal Reserve System. [ Links ]

Mendoza, E. G. and M. Uribe (1998). The Business Cycles of Currency Speculations: A Revision of a Mundellian Framework. International Finance Discussion Paper No. 617, Board of Governors of the Federal Reserve System. [ Links ]

Rebelo, S. and C. A. Végh (1995). Real Effects of Exchange Rate Based Stabilization: An Analysis of Competing Theories. Working paper no. 5197 (National Bureau of Economic Research). [ Links ]

Uribe, M. (2002). The Price-Consumption Puzzle of Currency Pegs. Journal of Monetary Economics, Vol. 49. No. 3, pp. 533-569. [ Links ]

Uribe, M. and E. G. Mendoza (2000). Devaluation Risk and the Business-Cycle Implications of Exchange Rate Management. Carnegie-Rochester Conference Series on Public Policy, Vol. 53, No. 1, pp. 239-296. [ Links ]

Végh, C. A. (1992). Stopping High Inflation: An Analytical Overview. International Monetary Fund Staff Papers, Vol. 39, No. 3, pp. 626-695. [ Links ]

Venegas-Martínez, F. (2000). Utilidad, aprendizaje y estabilización. Gaceta de Economía, Año 5, No. 10, pp. 153-169. [ Links ]

Venegas-Martínez, F. (2001). Temporary Stabilization: A Stochastic Analysis. Journal of Economic Dynamics and Control, Vol. 25, No. 9, pp. 1429-1449. [ Links ]

Venegas-Martínez, F. (2006a). Stochastic Temporary Stabilization: Undiversifiable Devaluation and Income Risks. Economic Modelling, Vol. 23, No. 1, pp. 157-173. [ Links ]

Venegas-Martínez, F. (2006b). Fiscal Policy in a Stochastic Temporary Stabilization Model: Undiversifiable Devaluation Risk. Journal of World Economic Review, Vol. 1, No. 1, pp. 13-38. [ Links ]

Venegas-Martínez, F. (2008). Riesgos financieros y económicos. Productos derivados y decisiones económicas bajo incertidumbre. Cengage Learning, 2a. ed., México. [ Links ]

Venegas-Martínez, F (2010). Planes no creíbles de estabilización de precios, riesgo cambiario y opciones reales para posponer consumo: un análisis con volatilidad estocástica. El Trimestre Económico, Vol. 77, No. 4, No. 308, pp. 899-936. [ Links ]

4 The inflation stabilization programs, which took place in Latin America in the 1990's, have been widely documented. We direct the reader to the references contained in Calvo and Végh (1998). In Latin America, the exception was the case of Peru, that left the nominal exchange rate float. Moreover, stabilization in Argentina was not based on an intermediate regime but in a hard peg; a currency board was used.

]]> 5 Though Calvo and Drazen (1998) focus on the duration of economic reforms, their results can be translated into an exchange-rate-based disinflation context. It is also important to point out that while Drazen and Help-man (1988), and Calvo and Drazen (1997) are mainly concerned with studying uncertainty about the timing of stabilization, we are interested in dealing with uncertainty about the exchange rate dynamics.6 We are mainly concern with small and open economies with a regime including a devaluation rate.

]]>