Servicios Personalizados

Revista

Articulo

texto en

texto en  Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Accesos

Accesos

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkRevista mexicana de ciencias agrícolas

versión impresa ISSN 2007-0934

Rev. Mex. Cienc. Agríc vol.6 no.8 Texcoco nov./dic. 2015

Articles

Commercial loans, a financing alternative. Case: Padelma Sugar, S. P. R. de R. L.

1Colegio de Postgraduados. Carretera México-Texcoco, km 36.5. C. P. 56230. Tel: 01 (595) 9520200. Ext: 1800. Montecillo, Estado de México. (perez.naty@colpos.mx; jarana@colpos.mx; rcgarcia@colpos.mx; angel01@colpos.mx).

In the rural sector, credit serves as a factor of investment with a further benefit, helping in the production process and therefore the development and its improvement. Resources are not always enough, so the farmers seek alternatives to meet their economic and personal needs. For this reason, this research aims to identify the determining factors in the probability of sugarcane growers that have commercial credit as a financing alternative. As well as making a comparison of results in probit and logit model of the determinants of trade credit. The research was conducted as a case study of sugarcane growers affiliated to Padelma Sugar, S. P. R. de R. L. (Society of Rural Production of Limited Responsibility) located in Paso del Macho, Veracruz. In 2013 a sampling study was conducted by probability to 90 sugarcane growers. Binary probit and logit model was estimated, where commercial credit is the dependent variable. It was concluded that producer age, years of education of the producer and yield cultivation, are factors statistically significant that influence the possibility to access a loan for the sugarcane producers. Finally, in the comparison of both models, the results show consistency with the theoretical and statistically established, as it was concluded that the marginal effects are quite similar and the significant variables that influence the probability of commercial credit in the sugarcane growers are the same.

Keywords: logit; probit; rural sector

En el sector rural el crédito funge como un factor de inversión con un beneficio posterior, mismo que coadyuva en el proceso productivo y por ende al desarrollo y superación del mismo. Los recursos no siempre son suficientes, por lo cual los productores buscan alternativas para satisfacer sus necesidades económicas y personales. Por tal razón, esta investigación tiene como objetivo identificar los factores determinantes que intervienen en la probabilidad de que productores cañeros tengan un crédito comercial como una alternativa más de financiamiento. Así también realizar una comparación de resultados en modelo probit y logit de los factores determinantes del crédito comercial. La investigación se llevó a cabo como un estudio de caso de los productores cañeros afiliados a Padelma Sugar, S. P. R de R. L (Sociedad de Producción Rural de Responsabilidad Limitada) ubicada en Paso del Macho, Veracruz. En 2013 se realizó un estudio por muestreo probabilístico a 90 productores cañeros. Se estimó un modelo binario probit y logit donde el crédito comercial es la variable dependiente. Se concluyó que los factores edad del productor, años de escolaridad del productor y rendimiento de su cultivo, son variables estadísticamente significativas que influyen en la posibilidad de que el productor cañero tenga crédito comercial. Finalmente en la comparación de ambos modelos los resultados muestran consistencia con lo establecido teórica y estadísticamente, ya que se concluyó que efectivamente los efectos marginales son muy similares y las variables significativas que influyen en la probabilidad de crédito comercial en los productores cañeros son las mismas.

Palabras clave: logit; probit; sector rural

Introduction

A society is in the presence of exclusionary practices when only a few of its members have access to financing. In Mexico, 8 out of 10 Mexicans are not served by the conventional financial system and the mechanisms used in the popular credit are insufficient to meet the needs presented by the rest of the population (De la Madrid, 2012).

Different types of financial intermediaries are those that exist in Mexico according to the services they provide. It is the most important credit institutions or banks, as they are generally known (Banxico, 2011).

"Despite the number and diversity of financial institutions in the system of savings and loans in the country, there are few organizations that have ventured into the countryside. Of these, an even smaller number of institutions have been able to provide services in a sustainable manner, without subsidies; ensuring security, convenience, liquidity, confidentiality, access to timely and adequate credit, good service and returns to the rural population" (Becerril, 2010).

The absence of formal financial services in rural areas does not mean that its inhabitants do not require the service. Savings in kind, "money-keepers", batches, savings groups, speculators and moneylenders are among the mechanisms used in rural areas to supply extra formal financial services ways (PATMIR-SAGARPA, 2006).

The loan serves an important role in society, as it allows to use resources that are not proper to temporarily advance the consumption and investment decisions, and it can cover emergency expenses, a situation that often seriously affect families with incomes reduced and fluctuating. To obtain credit as the first condition is needed to prove that he has income and the second is to show that there is an acceptable probability that such revenues are sustainable over time (De la Madrid, 2012).

Several authors have identified factors that influence access to credit. As mentioned by Escalante et al. (2013) in his study with data from 832 municipalities in Mexico (study sample) in order to analyse the variables that determine access to credit in the Mexican agricultural sector; for which he applied an econometric probit model where the factors that influence the ability to access the credit market were analysed, such as; the association of producers, surface production units, the level of education, subsidies, social characteristics of the producer and the training received by producers.

The model results showed that, the agricultural area and yield has a positive and statistically significant impact, which confirms that the large agricultural producers have higher access to credit, which can ensure, even with the same property, also yield makes creditworthy and involves a higher level of profitability and capacity for payment. Similarly, the variable rate of agricultural and subsidies schooling producer and behave, as both have a different positive probability, it is argued that the resources of the subsidy may contribute to the payment of credit services, so it is more likely that the producers who have support do have access to credit; higher and more education is the possibility of having access to credit. The index of speakers of indigenous languages has a negative effect on the probability of being creditworthy; municipalities with a higher level of marginalization have a lower likelihood of financial institutions to offer resources for production.

In this regard, De la Madrid (2012), on his report "Discrimination in Mexico - credit", determines the level of education as one of the factors that enables access to financial services in the field of insurance and finance, industry securities, banking and savings and loan sector (SCAP). In his research shows that education is related to the use of financial services. Because users of credit with more schooling are mostly located in the strata of the insurance industry and finance, securities industry and banking sector, according to their level of education. It also determines that less schooling, higher preference for cash management. The more education increases the preference for the use of debit cards or checks.

As we can see, the rural sector is a sector with little access to credit; same situation is presented by Padelma Sugar cane producers, since taking credit even with this organization turned to other financing alternatives to meet their production needs and personal cane, using alternative informal sources and in some cases commercial loans. Whereas the production of sugarcane is a crop with high social impact and historical tradition, the importance in farm families is significant as they depend on it. Production, processing, and marketing are integrated into a production chain in which there are basically three links that are: 1) sugarcane growers; 2) organizations; and 3) agribusiness (sugarcane plots). Therefore this research is plated in order to identify factors involved in determining the likelihood that a worker has for getting a commercial-credit. As well as making a comparison of results in probit and logit model of the determinants of credit. With the objectives established it is possible to determine whether the characteristics associated to the producer and production efficiency are crucial for credit; and if the estimate of the marginal effects from the probit and logit model are similar.

Materials and methods

The research was conducted at the Padelma Sugar S. P. R. de R. L., located in the town of Paso del Macho, State of Veracruz, with coordinates 18° 58' north latitude and 96° 43' west longitude at an elevation of480 meters.

A mixed approach was used in which the systematic integration of quantitative and qualitative methods provide more complete information for the study analysis. However, the method of bibliographic research in this research has provided key elements to begin the development. (Hernández et al., 2003).

The field work consisted of conducting surveys to sugarcane growers and simple random sampling method (MIA) was used with a reliability of 90% and 10% absolute error (Spiegel and Stephens, 2002). It was considered to use a variance p (ratio) p = 0.5 p represents the highest variability between different proportions. This practice is done in studying ratio estimators and is intended to strengthen it, and if the actual ratio is different from this value, the better accuracy (Cochran, 1997).

The sample size was determined with the following equation:

1)

1)Where: N= total study population; n= sample size; p*= proportional estimator: p= (1-q); q=proportional estimator: q= (1-p); B= proportional estimator; D=absolute estimator.

p* and q*= is assumed that the variance of the sampling distribution fulfills the same function as the variance of the estimate of the means, as it measures the dispersion of the sample proportions and shows that the variance of the proportions corresponding to the product p*q (Vivanco, 2005).

Substituting values for the calculation of the sample:

The total sample was 90 polls considerable number for analysis thereof. For the implementation of the surveys it was used to the database provided by the enterprise, data used to locate the producers considering all the towns to which they belong. Because of the availability of time by people to interview and considering the willingness of producers to participate in this process, the implementation of surveys was conducted in three phases.

The first phase was held on 17 and 18 June 2013, which through the enterprise cited people to interview in the premises of the company, covering for this stage 40% of the sample.

In the second phase of the survey 30% of the sample was applied (taking place on 18 and 19August 2013), and finally in the third phase, the total sample was covered (by applying them on 20 and 21 October 2013). It is worth mentioning that for these last two phases, the enterprise intervened in the same way quoting interviewees in their facilities; however, in the case of people with closest to the direction of the company were visited in their own home. Total respondents were distributed in 15 villages of the town of Paso del Macho, hinterland of the S. P. R. de R. L. with a minimum of 3 to a maximum of 10 respondents per location. For processing and analysis of information was necessary a statistical method to analyse the research variables of both quantitative and qualitative data, as well as a database in Excel.

With the database we proceeded to generate a regression model with qualitative responses, also known as probabilistic model, aiming to find the probability of an event happening. In the event the investigation is likely to sugarcane growers to have commercial credit and its determinants influencing variables in this event. The analysis was performed through probit models and logit regression; where the hypothesis test for statistical significance in the analysed variables in the model was as follows: Ho: β= 0 vs. Ha= β ≠ 0 with a reliability of 95%; under the decision rule under test, which states that if χ  > χ

> χ  (c= calculated, t= tables), then the null hypothesis is rejected in favour of the alternate (Infante and Zarate, 1990)

(c= calculated, t= tables), then the null hypothesis is rejected in favour of the alternate (Infante and Zarate, 1990)

In the probit model the distribution function used is the standard normal, with which the model is specified through the following expression;

)2

)2

Where: the variable "s2" It is a "mute" variable of integration with zero mean and variance 1.

The probit model for this research is as follows:

)3

)3

y= 1: if the producer has commercial credit; y= 0 if does not have commercial credit; β= parameter vector; X= vector of factors that explain the probability of y;  (β 'x)= Standard normal distribution.

(β 'x)= Standard normal distribution.

The differences between estimates of the models logit and probit results are not great together given the similarity between the curves of the standardized normal and logistics, with these differences in operational, due to the complexity presented calculation normal distribution function versus logistics, since the former can only be calculated in the form of integral (Medina, 2003). For the model logit function used it is the logistics, so the specification of this type of model is:

)8

)8

In general, estimates of the logit model will be between 1.6 and 1.8 times those of probit (Medina, 2003).

These estimates were applied through the statistical procedure Proc, Probit and Proc, Logistic of the Statistical Analysis System (SAS).

The tests of the model probit and logit began with 7 variables (age, education, total area of the producer, area used for sugarcane, yield, ownership and use of irrigation), and due to the non-significance of some variables, we only used for analyzing the variables age, education and yield.

Results and discussion

With the surveys applied to the producers of Padelma Sugar S. P. R. de R. L., township Paso del Macho, Veracruz, surveys that allowed to gather general information and specifies of the sugarcane growers, also a rated classification among those producers that have commercial credit and they do not have that kind of credit.

General information: sugarcane growers have an average age of 46 years, which is within the parameters asking financial institutions of this municipality as one of their requirements to access their services. The data showed that 87% whose main activity is focused on agriculture cane cultivation and the remainder represents other activities with the following characteristics; chemicals used in store, grocery store, selling food and income taxi. In regard to the gender variable; 80% of respondents producers are men and 20% women.

This is reinforced by data from FAO-SAGARPA (2012). Where approximately 15% of rural economic units (EBU) in the Gulf Region correspond to the average marginal strata with high marginality media assets and high assets are held by women. 29.2% of the EBU belonging to the middle layer with low marginal assets is under the responsibility of women. The average schooling is 5.5 years. 22% of the total sample have completed the elementary school, 59% records from 1-5 years of study, 8% have finished high school, 7% did not finished high school, 3% represents producers who do not have studies and the highest level of schooling observed is high school (12 years of study) with 1% participation.

These results are comparable and reinforced information SAGARPA FAO (2012); where in the Gulf Region is presented in higher percentage producers who have a grade, 63.6%. Similarly the results of the analysis of respondent's producers were obtained. In addition to this; lower strata of assets have the highest proportions of responsible EBU who missed no schooling: 18% in high marginality, marginalization 16.8% on average (which belongs to Paso del Macho) and 12.4% lower margins. For its part, the highest active layers have the following percentages responsible for EBU who completed a university degree: 8.9% in the high marginality, marginalization 10.8% in average and 9.1% in low marginality.

In the production data of respondents predominantly under private ownership in 72%, followed by 21% that represents producers who rent plots and the remaining 7% (private and rented) of mixed regime. These results are in the same direction as the determined nationally, where 60% of landowners including both private owners and to the social sector have less than five hectares, a figure that contrasts with the 178 average hectares per producer observed in the United States of America (De la Madrid, 2009). Likewise, the research results are consistent with the parameters given by FAO-SAGARPA (2012), where the proportion of EBU in this region reported using own land ranges between 88% and 98%. Moreover, between 0.7% and 11.9% of EBU it used a combination of own, borrowed land, middle income or other form of possession.

The average yield for producers in the study sample is 58.51 tons per hectare with an average acreage of 9 hectares per producer; while pointing the SAGARPA (2011) the average cane yield per hectare in Mexico is about 70 tons. Need of financial service. Sugarcane growers borrow respondents to the need of urgent cash. The results showed that 63% of such producers go to a family member or friend to apply for borrowing money in order to meet their need, 26% goes to a microfinance and 11% sell an animal.

Variables established for the probit and logit model:

Credcomercial. Dependent variable, characterized by being a dichotomous variable with values 0 (the producer has commercial credit) and 1 (the producer does not have commercial credit), allowing to know if the producer does not use or commercial credit.

Age= age of the producer; Escol= years of schooling of the producer; and network: yield.

In the probit model with the respective normal distribution, first results were obtained as a classification of sugarcane growers and non-commercial loans; of the total data, 34 producers who have credit with commercial banks and 56 credit producers have obtained commercially. The variables (age, education and yield) as a result have been identified as significant for the model with respect to the statistic presented in T able 1. The estimators obtained in the model were statistically significant at 95% confidence in its entirety showing values of p-value less than the value of α of .05, which allows us to reject the null hypothesis that indicates the lack of significance of the parameters (Table 1).

In Table 1, the age, education and yield variables have a direct and statistically significant effect by increasing the probability that the producer has commercial credit, because if the variable "age" the producer is incremented by one, the probability of commercial credit have increased. So that is suitable to apply for credit to commercial banks as for the specifications and requirements in the age factor for the commercial banks; such as Azteca bank that manages an age range of 20-59 years, Banamex from 21 to 79, and Caja Yanga from 18 to 64 years, with these institutions mentioned by interviewees and located in the town of Paso del Macho, Veracruz.

The model results with respect to the variable "schooling" are comparable with the investigation of Escalante et al. (2013) as a determinant of credit in the Mexican agricultural sector. In the model established for the analysis of commercial credit in Padelma Sugar cane producers, consistent with the aforementioned research and because the results showed a variable positive impact and statistically significant. So, by increasing the average years of schooling unit increases the likelihood that the farmer can have credit with commercial banks. Since a higher level or degree of schooling, will allow the producer to make more informed decisions affecting their personal and economic welfare, and can handle minimum information necessary to manage your credit in a positive way, as well as the decision to access other financial service as it deems it appropriate.

The model results of this research to the variable "yield", shown as a variable direct and statistically significant increase in the probability that it has any commercial credit. This will serve as collateral to access credit from commercial banks; thereby sustained ability to pay. Results that are comparable with those made by Escalante et al. (2013).

Marginal effects. Due to the nature of this research model, in order to determine the magnitude of the effect of each of the variables, it is necessary to obtain the marginal effects, which reflect the variable that has higher effect on the probability that producers of sugarcane for having a commercial credit is the variable "schooling", which shows that the increase in a year the level of education of the producer, the probability of commercial credit increased by 6.2%, the second variable of importance for the model, is the variable "yield" as it shows that the increase in unit yield of cane, the probability of commercial credit increased by 2.2%. The variable "age" has a marginal effect of 0.013, which shows that with a 1% increase in this variable, the probability of commercial credit increased by 1.3% (Table 1).

Logit model. Since the logit and probit models would produce qualitatively similar results can be obtained coefficients from logit from the probit coefficients and vice versa; based on the above by Enchautegui (2003) and through the software package Statistical Analysis System (SAS) The following results were obtained. Through statistical procedure PROC LOGIT in the same 90 observations that were analysed for the probit model, the classification of 34 producers was obtained, who have credit with commercial banks and 56 producers who have no commercial credit.

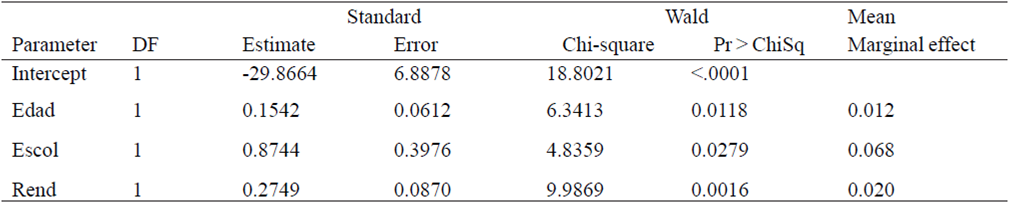

The information cited by Medina (2003), which states that the results estimated by probit and logit models do not differ much from each other, is reaffirmed with obtaining results obtained in this investigation of sugarcane growers. Since comparing the estimation of both models confirms the parameter that the same author mentioned (logit model estimation will be between 1.6 and 1.8 times the Probit), where the coefficient probit to be multiplied by approximately 1.8 coefficient is obtained logit, in the same way with the 1.6 factor can also get the approximate value of the logit coefficient. Estimated by the logit model results are shown in Table 2, where the estimated value of the intercept logit model (-29.86) is 1.6 to 1.8 times the value of the intercept in the probit model (-17.67; Table 1). Estimating the value of the significant variables age, education and yield as shown below. The estimated value for the significant variable "age" in the logit model (estimated value = 0.15) is 1.6 to 1.8 times the value of the same variable in the probit model (0.09; Table 1).

Table 2 Analysis of the estimator of parameter in the logit model.

Fuente: elaboración propia con SAS.

With regard to the significant variable "education" for the logit model estimation it has a value of 0.87 which is about 1.6 to 1.8 times the value of the same variable in the probit model (0.45; Table 1). Finally, the same approach is found in the variable "yield" as the logit model that variable reflects an estimated value of0.27 is approximately 1.6 to 1.8 times its value in the probit model (0.16; Table 1).

Also in Table 2, it can be seen that in logit and the probit model, the variables age, education and yield vary with signs expected positive and statistically significant at the 95% confidence level, where their values are less than a .05 (age= 0.011,=0.027 schooling, yield= 0.001). Likewise such results allow to reject the null hypothesis indicating the lack of significance of the parameters.

Marginal effects. In the logit model, the variable "age" is 1.2%, which represents an increase of probability that sugar producers have commercial credits, this percentage increased to the same variable. Which is similar to the effect obtained in the probit model (1.3%; Table 1).

For the variable "schooling" in its marginal effect, the logit model shows that as it increases by one the year of schooling of the producer, the probability that the sugarcane producer has commercial credit is 6.8%. What is pretty much the same to that obtained in the probit model (6.2%; Table 1). The same situation occurs in the variable "yield" as that obtained in the logit model (increase of 2% chance that sugar producer has commercial credit to a percentage increase per unit in the variable yield) is similar affection obtained in the probit model with 2.2% probability that producer credit (Table 1).

Therefore, the results of the marginal effects obtained in the logit model probes that the similarity with effects obtained and analysed in probit; since the only difference is marked by decimal directly as shown in Table 3. Where producer schooling variable is more important in both models, being 0.6% higher in the logit model. Minor variable in both models is old producer, with 0.1% the biggest difference in the probit model. The variable yield, ranks second in importance for both models, with a difference of 0.2% higher in the probit model.

Conclusions

In the study it is found that the variables age, education and yield are factors that influence the possibility of the sugarcane producer to have a commercial credit. Thus, the characteristics associated to the producer and production efficiency are crucial for access to commercial credit to those producers.

With the comparison of logit and probit models, the results show consistency with the established theoretical and statistically; likewise it meets the objective and the hypothesis established for this investigation, and the results show that the regression coefficients are different between the two models because they were estimated based on different probability functions; and regarding the marginal effects are quite similar and significant variables that influence the probability of commercial credit in the sugarcane growers are the same. Where the schooling variable is the most important in the probit model and the logit model, making a difference of 0.6% higher in the logit model, thus reflecting the importance of a degree of schooling, this will facilitate making decisions best suited to the producer at the time of the possibility of access to credit, as well as a higher willingness to request information about the financial service, which will allow the producer easier access to credit. Yield has second level of important in both models reflecting in producer payment guarantee to access credit, being 0.2% higher in the probit model.

Finally, the variable age is 0.1% higher in the probit model, being the minor variable for both model; however, it is part of the requirements to apply for credit, representing more responsibility and ability to pay.

Literatura citada

BANXICO (Banco de México). 2011. Sistema financiero. http://www.banxico.org.mx/divulgacion/sistema-financiero/sistema-financiero.html. [ Links ]

Becerril, T. A. 2010. Servicios financieros en el medio rural caso Xalacapan, Zacapoaxtla, Puebla, México. Tesis de Maestria. Colegio de Postgraduados. Montecillo Texcoco, México. 169 p. [ Links ]

Cochran, G. W. y Snedecor, W. G. 1997. Métodos estadisticos. Compañía Editorial Continental, S. A. México. 703 p. [ Links ]

De la Madrid, E. 2009. ¿El campo puede crecer? El Universal. http://www.eluniversal.com.mx/notas/587020.html. [ Links ]

De la Madrid, R. R. 2012. Reporte sobre la discriminación en México 2012 - 06: crédito. Ed. Conapred. México. 82 p. [ Links ]

Enchautegui, M. E. 2003. Módulo de estudio sobre modelos probit y logit. Departamento de Economía, Universidad de Puerto Rico. Recinto de Rio Piedras. 16 p. [ Links ]

Escalante, R.; Catalán, H. y Basurto, S. 2013. Determinantes del crédito en el sector agropecuario mexicano: un análisis mediante un modelo Probit. Cuadernos de Desarrollo Rural. 10(71):101-124 p. [ Links ]

FAO-SAGARPA (Food and Agriculture Organization of the United Nations-Secretaria de Agricultura Ganaria, Desarrollo Rural Pesca y Alimentación). 2012. Diagnóstico del sector rural y pesquero: identificación de la problemática del sector agropecuario y pesquero de México. Capitulo I, II, y III. [ Links ]

Hernández, R.; Fernández, C. y Baptista, P. 2003. Metodología de la investigación. 4a. Edición. México, D. F. McGraw Hill. 627 p. [ Links ]

Infante, G. S. y Zárate, de L. G. P. 1990. Métodos estadísticos: un enfoque interdisciplinario. Trillas. México. 643 p. [ Links ]

Medina, M. E. 2003. Modelos de elección binaria. 26 p. http://www.eva.medinaam.es (consultado febrero, 2014). [ Links ]

PATMIR-SAGARPA (Proyecto Regional de Asistencia Técnica al Microfinanciamiento Rural y Secretaria de Agricultura, Ganadería, Desarrollo Rural, Pesca y Alimentación). 2006. Promoviendo el desarrollo y la consolidación de un sistema financiero al servicio del sector rural marginado en México. México. 19 p. [ Links ]

SAGRAPA (Secretaria de Agricultura Ganaría, Desarrollo Rural Pesca y Alimentación). 2011. Producción a partir de caña de azúcar. 321 p. [ Links ]

Spiegel, M. R. y Stephens, L. J. 2002. Estadística. Serie Shaum. Tercera Edición. McGraw Hill. México. 541 p. [ Links ]

Vivanco, M. 2005. Muestreo estadístico: diseño y aplicaciones. Edit. Universitaria. México. 209 p. [ Links ]

Received: June 2015; Accepted: October 2015

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons