Servicios Personalizados

Revista

Articulo

Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por emailIndicadores

Citado por SciELO

Citado por SciELO Links relacionados

Similares en

SciELO

Similares en

SciELO Compartir

Permalink

PermalinkAmérica Latina en la historia económica

versión On-line ISSN 2007-3496versión impresa ISSN 1405-2253

Am. Lat. Hist. Econ vol.19 no.3 México sep./dic. 2012

Artículos

Adoption of Double Entry Bookkeeping in Mexico and Spain

Adopción de la partida doble en México y España

Bernardo Bátiz-Lazo*, J. Julián Hernández Borreguero**, J. Carles Maixé-Altés***, Miriam Núñez Torrado****

* Universidad de Bangor, Gales, Reino Unido, <b.batiz-lazo@bangor.ac.uk>

** Universidad de Sevilla, Sevilla, España, <julianhdez@us.es>

*** Universidad de La Coruña, La Coruña, España, <maixe@udc.es>

**** Universidad de Sevilla, Sevilla, España, <miriam@us.es>

Fecha de recepción: mayo de 2011.

Fecha de aceptación: febrero de 2012.

Abstract

There are conflicting and even contradictory claims as to when exactly double entry bookkeeping arrived to New Spain as well as its diffusion during the colonial era. Although we fail to present evidence from Mexican private enterprise, we address the apparent contradictions while putting forward the idea that the history of "modern" accounting practice in Latin America should be framed by developments in its former colonial power. Our conclusion is that the history of Latin American accounting should be wary of extrapolating everyday practice by interpreting bibliographic material and proceed to pay greater attention to the appropriation of accounting technology through the examination of surviving company documents as well as informal educational practices amongst organizations based in Spain and its colonies.

Key words: digraphic method, accounting systems, knowledge transfer, viceroyalty.

Resumen

Las fuentes y la información disponible son contradictorias respecto al origen y difusión de la partida doble durante la colonización española y tras la independencia. Aunque no ofrecemos evidencia sobre actividades en el ámbito de la empresa privada, este artículo se propone acotar dicho debate y obtener nuevas conclusiones al proponer que la historia de la contabilidad "moderna" en América Latina debería estar enmarcada por los acontecimientos en la metrópoli. Nuestra conclusión es que la historia de la contabilidad en América Latina debe proceder con el examen de fuentes y prácticas de las organizaciones y no llegar a conclusiones únicamente basadas en el examen de libros de texto.

Palabras clave: método digráfico, sistemas contables, transferencia de conocimiento, virreinato.

Introduction

The research in this article aims to enhance understanding of the use and diffusion of "modern" accounting techniques outside of Europe and Anglo-Saxon countries by outlining empirical considerations for the comparison of practices in the American colonies with those in Spain. The issues at hand are the timing and nature of the adoption and diffusion of double entry accounting in Latin America. This article does not provide a definitive answer to these questions. Instead, it offers a new empirical framework for the discussion whilst pointing towards a research agenda for an accounting history of Latin America, through the case of Mexico.

The motivation for this project lies in the handful of contributions which explore accounting practices in former Spanish colonies in Latin America before and after their independence.1 The idea is that developments in Latin America should not be studied in isolation but as an educational process in which the transfer of knowledge is mapped while considering developments in accounting practice and accounting thought within the former colonial power. One potential starting point for this analysis is the so-called "Transfer of Accounting Technology" framework.2 According to this approach, accounting can be transferred from one country to another through a rather complex process that can be described by answering one or more of the following questions: a) what inhibiting factors were there (technical and non-technical)?, b) what were the vehicles of transfer, the networks of access to the originating economy, the information goals of the acquirers, the methods of information collection, the speed of transfer of the technology?, c) what was the rate of adoption, the networks of distribution into the receptor economy, the hindrances faced by the carriers of the new technology?, d) was the incoming technology reshaped by economic conditions, social factors or conditions in the physical environment?, and e) were there any reverse flows of technology?

This approach, however, perceives accounting as a technology that is neutral, unchanging and detached from social actors. Instead, we prefer to follow the lead of Tom Misa and Johann Schott in characterizing the international transfer of technology and knowhow as a process of "appropriation".3 Whereas diffusion is a passive and directionless process driven by random collisions, appropriation suggests an active process in which ownership of a new technology is deliberately and forcefully established by its recipients. In other words, culture and context are relevant in researching accounting history in Latin America. However, during the course of our research and as will be shown below, it became evident that there was a need to reinterpret some of the key studies on accounting history in Spain because these studies often tackled the migration of double entry bookkeeping on the back of evidence emerging from accounting manuals and textbooks. The possibility of appropriation was neglected as these contributions failed to consider accounting as a social and institutional practice that has to be studied in the context in which it operates.4 Without this reassessment, therefore, current and future work documenting the history of accounting in Latin America risks building upon false premises. We will show there was continuity in the use of double entry in Spain and this is the basis for establishing its potential use by public and private enterprise in Latin American colonies. We support this claim through the examination of everyday practices rather than interpreting bibliographic material.

The research focused on developments in Spain and then ascertains the likelihood of its adoption within the viceroyalty of New Spain, a territory whose location, extension and wealth made it a geo-strategic priority for both the Spanish crown and Spanish merchant houses. Most of this territory became a sovereign state after a process of independence that began in 1810. Since 1917 this republic has been formally known as Estados Unidos Mexicanos (henceforward Mexico).5 In light of a dearth of systematic studies on Mexican private enterprise accounting, our chief aim is to establish a framework upon which to assess these developments. In order to do so, we revise and offer new evidence of accounting practices in Spain during the colonial period.

As a starting point, the second section summarizes established views regarding the introduction of accounting techniques within Spain before and in the early colonial era. This is followed by a survey and reinterpretation of contributions published in Mexico dealing with the arrival and diffusion of double entry bookkeeping in public bodies. The third section expands these studies by looking at the context and rationale behind the first attempt to introduce the double entry method in the public management of colonial institutions. It documents in detail the accounting guidelines introduced during Bourbonic reforms in order to identify its influence on colonial and postcolonial accounting practice in the Mexican public sector. This third section also offers indirect evidence that double entry was known within the Mexican private sector.

The fourth section retakes the survey of contributions published in Mexico dealing with the arrival and diffusion of double entry bookkeeping in the Mexican private sector and looks at the possibilities of knowledge transfer amongst private companies across the Atlantic during the colonial era. However, during the course of the research it became evident that there was a need to revisit the consensus about the evolution of "modern" accounting in Spain and specifically the so called "stage of silence and apparent oblivion in accounting doctrine",6 which oscillates between the end of the 17th century and the early 18th century. As its name suggests, it claims that double entry bookkeeping was "abandoned" or at least "overlooked" as far as the production of didactic texts was concerned whilst implying the practice was discontinued in private enterprise. Ascertaining the validity of this claim was important because, if true, it would imply that the actual transfer between Spain and Latin America took place either at the start or the end of the colonial era rather than during a dilated period. Evidence documented in this article emerges from surviving company records. It details the use of double entry bookkeeping in private organizations based in Madrid and Barcelona circa 1690s and 1800s. It suggests double entry was very much alive in the everyday practice of business organizations based in key geographies of economic activity in the Spanish mainland. This clarification is the basis for our empirical framework and thus for future analyses of the nature of appropriation of double entry bookkeeping in the Mexican private sector. Admittedly, we do not resolve the issue but we do provide clarification and a solid basis for future research.

The last section offers a discussion and conclusions. Here it is claimed that the future of the study of accounting history in Latin America will emerge from a synthesis based on contrasting contemporary accounting practices (as reflected in surviving documents of public and private organizations), trade regulation, contemporary manuals and treaties as well as informal education practices (such as apprenticeships and visiting stays).

Development of accounting practice

From pre-modern capitalism (circa 1200 to 1500) to the adoption and diffusion of double entry bookkeeping (circa 1500 to 1630)

Gary Carnegie and Lúcia L. Rodrigues7 have noted how academic circles in Spain are one of the handful of non-English speaking spaces characterized by a vibrant research agenda in accounting history. This "maturity" implies that there is a considerable number of systematic studies documenting the overall development of Spanish accounting practices. In particular, Esteban Hernández Esteve and José González Ferrando8 offer comprehensive compilations on the evolution of accounting technology in both the public and private spheres (such as accounting for merchants, local and central treasury).9 Hernández Esteve proposes an interesting scheme to segment developments from the Middle Ages up to the 20th century. Its starting point is the period that immediately precedes the development of double entry bookkeeping (labelled "pre-modern state", circa 1200 to 1500). Accounting documents act chiefly as an aide-memoir, due to the number of operations businessmen had to remember or consider.10

Vlaemminck states that the single entry method replaced memorial and merchant books as it offered greater order, was much more systematic and methodical and incorporated a greater number of books as this method was responsible for introducing dedicated books to record debits and credits. Although interesting, this first stage is of little relevance to the overall purpose of our study given that the Spanish conquerors did not arrive in what was to become Latin America until 1492.

A second stage for Hernández Esteve and González11 regarding the evolution of accounting technology in Spain coincides with Columbus' voyages and the start of the process of constructing modern day Spain. They specifically point to the Reales Pragmáticas de (Royal decrees of) Cigales, 1549, and Madrid, 1552, enacted under Phillip II, which became the first ever-recorded regulation in Spain –and in the world– that the adoption of double entry bookkeeping.12 This regulation called "to have and to register entries in the Spanish language on a handbook (journal) and cash book (ledger) using debits and credits". Interestingly, in the vernacular this method was identified as journal and ledger system (libro de caja con manual) rather than "double entry".13

Early developments in the Spanish metropolis were almost immediately followed in New Spain. For one, Cordero y Bernal14 identifies an initial development taking place in 1519, namely the appointment of the first "accountant" in the Spanish colonies (and specifically in the government of the port of Veracruz) and in 1536 the introduction of an accounting book in the Casa de Moneda (Mexico City's mint), the oldest in the new continent and which carried its entries with Roman numerals (the so called cuenta castellana). In a similar vein, Hernández Esteve15 notes that 150 copies of Bartolomé Salvador de Solorzano's treaty on double entry accounting were taken by Diego Felipe de Aldino and Bartolomé Porras in 1591 to be sold in New Spain. However, this fact has been neglected by Mexican accounting historiography. See table 1, which summarizes contributions by Mexican authors and foreign academics studying Mexican accounting history published in professional and academic forums and dealing with the adoption of double entry bookkeeping in Mexico. Two of these studies date back to the colonial period while most of them date back to the second half of the 20th century. A "bird's eye view" seems to predominate in the latter contributions, that is, studies which offer a broad and rather general overview of the development of accounting methods in capitalist societies (with a bias towards developments in Western Europe and North America). A common thread of these contributions is their didactic nature and textbook roots. Most of these sources progressed using prior research rather than through the systematic study of archival sources. Lack of research based on surviving business and government records thus resulted in the perpetuation of myths, errors, omissions and misunderstandings particularly regarding the arrival, diffusion and actual use of double entry bookkeeping.

The small quantity of systematic studies also reflects a lack of a research program around the history of accounting within Mexican educational institutions.16 Indeed, systematic studies on the diffusion of accounting history as a research agenda have failed to identify any critical mass of activity in Mexico17 while others point to the absence of any substantive effort for the whole of Latin America.18

It is possible that table 1 is not inclusive of all studies in the area. It is also possible (if not probable) that our survey failed to detect dissertations and other published and unpublished contributions that might be of relevance. However, no other study was identified within the digital catalogues of the aforementioned universities. Nevertheless there are citations within the publications in table 1 to other studies (mainly dissertations) but these have either not survived or not been catalogued by these universities. The research thus proceeded under the assumption that table 1 encompassed the totality of empirical studies by authors dealing with the adoption and diffusion of "modern" accounting techniques during the colonial and postcolonial eras.

A recurrent theme within the studies summarized in table 1 is a debate regarding the adoption and first use of double entry bookkeeping in Mexico. On the one hand, within this debate there is some consensus as to developments in public accounting. For instance, Joaquín Maniau19 claims that the first attempt to introduce the "admirable method of double entry" bookkeeping dates to 1785. The aim was to 'standardise different practices within colonial public accounting but it was abandoned given the confusion in its application toppled with the problems to eradicate long standing practices".20 Maniau's view is consistent with that of John TePaske and colleagues21 who state that this innovation was adopted within the caja de México in the colonial capital in 1786 and a year later in the provincial administration. Alvarado22 states that it is 1784 when the introduction of an unspecified piece of regulation institutes the use of the double entry method across the colonial government. But in the same line as Maniau and TePaske, Alvarado and colleagues claim that Spanish authorities lost the "tug of war" with civil servants who opposed the former's attempts" and the regulation was repealed three years later.

To better understand these contributions to Mexican historiography and specifically the first use and derogation of the double entry method in the public accounting of the New Spain one has to consider developments in the Spanish metropolis during the colonial period. The next section will detail how Bourbonic reforms had an impact on accounting regulation and practice.23 During the discussion note how, as has been documented by Núñez Torrado,24 ledgers for the different "monopolies" were all prepared in situ and then posted to metropolitan authorities for auditing, thus opening up the possibility for reverse flows of technology –a possibility that has been neglected by other studies of public accounting in New Spain.25

Double entry in the public Accounting of Spain and New Spain

Early developments and the influence of French Enlightenment

As noted above the double entry system began to be used as part of government records in Spain during the 16th century. For instance the local government of Seville used this method from 1565 onwards, that is, 25 years before the Spanish central Treasury.26 Another early adopter was also found in Seville, namely the treasury office of the Casa de la Contratación (Board of Trade with the Americas).27 In 1592, Phillip ii introduced double entry accounting in the kingdom of Castille but it failed to expand to provincial governments as its use was suspended in 1621.28

Charles ii of Spain, the last of the Habsburgs, died in 1700. This was immediately followed by the coronation of Phillip v, who became the first monarch of the ruling Bourbon dynasty. The establishment of a new dynasty introduced several institutional, economic and administrative changes, many of which took more than one attempt to be successfully implemented. The introduction of innovations in the social, economic and political spheres was inspired by the philosophical tenants of the French Enlightenment. These reforms extended to the Spanish overseas dominions.29

Since early in the 18th century, the newly arrived Bourbon administrators gave the viceroyalty of New Spain priority as a geo-strategic enclave for three main reasons, namely: a) deep water coastal ports on two oceans, which also allowed maritime links with Spanish possession in the Far East (namely, the Philippines);30 b) act as a platform to originate capital investments into Asian and Caribbean possessions, with the side effect that these investments strengthened the raison d'être to remain part of the Spanish crown,31 and c) it regularly made substantial fiscal contributions to the Treasury as well as transferring precious metals (mainly silver) to the peninsular economy.

Bourbonic administrative reforms initially attempted to introduce double entry in the public sector in 1743 at the Giro Real or Cross Border Payments Department. But it was unsuccessful as it found resistance from bureaucrats who were unwilling or unable to adopt the method due to a lack of training as well as doubting its usefulness on "ideological" and "conceptual" grounds (rejection to which bureaucrats failed to provide detailed arguments).32

The pace of the Bourbonic reforms strengthened during the reign of Charles iii (1759-1788). This period of change began with the introduction of major fiscal measures following the arrival of José de Gálvez y Gallardo, Marquis of Sonora as visitador de Hacienda y Justicia e intendente general del ejército (visitor for Treasury and Justice as well as Army Quartermaster general).33 Gálvez's mandate was detailed in a confidential memorandum dated 14th April 1765. In his letter, Charles iii urged Gálvez to look for ways to maximize financial returns to the crown but without creating new taxes or increasing taxable income thresholds.34 The king wanted Gálvez to compile as much information as possible regarding the situation of public finances in New Spain so that, at a later date, this would become the basis for a plan of action to achieve greater efficiency in the use of public funds while also looking to improve the running of public bodies.

The general disorder of New Spain's treasury was considerable. For instance, the Tribunal de Cuentas de Nueva España (General Accounts Court of New Spain) had a duty to send an income and expense report every six months to the Contaduría General del Consejo de Indias (General Accounts Office of the Council of the Indies). By 1759, when Charles iii ascended to the throne, the Accounts Court had failed to inform the General Accounts Office for many years. In view of the situation, the king immediately ordered a review and audit of all the books and accounts of the viceroyalty between 1703 and 1759. After a meticulous examination, the General Accountant Office's report criticized the lack of method and procedure determining the order of entries in the accounts as well as the absence of any rigor in the process of checking and verification of these books.35 Indeed it was the apparent loss of income to the crown, due to the lack of order and information regarding New Spain's accounts, which led to Gálvez's visit. To highlight its importance, the king issued a Royal Order (11th March 1765). In this order he instructed the General Accounts Court to send detailed accounts of all incomes that belonged to the Royal Treasury.36

In response to the Royal Order, the General Accounts Court issued a decree dated 1st July 1765. This decree basically reinstated the contents of the Royal Order but retroactively, so that the information not yet supplied to the Council of the Indies was forthcoming.37 Meanwhile, when Gálvez arrived in New Spain, he found that most sources of income were leased to private bodies. This arrendamiento or asiento (leasing system) had been typical of the Hapsburg administration, where a person or company gained exclusivity in the exploitation of a specific source of income of the Royal Treasury. In return for allowing the exploitation of a lease, the asentista (contractor) paid the crown a fixed amount in cash and/or made a payment in kind.38 Under the Hapsburgs, therefore, the Royal Treasury effectively outsourced to private contractors unknown income streams emerging from the collection of taxes, import duties, tithes, etc., in exchange for a known fixed payment.

However, the leasing system was detrimental to both taxpayers and the Royal Treasury. On the one hand, contractors profited from the ignorance of crown representatives regarding the potential of individual leases. On the other, in cases where winning bidders were forced to pay a predetermined canon (tax or rent), they would simply pass on these to taxpayers or ultimate consumers.

The introduction and relative success of fiscal reforms in Spain were the basis for eliminating the leasing system while increasing tax income but without changing the tax base in New Spain. To achieve this, Gálvez engaged in a swift process of economic reform while implementing a new collection system. It replaced the leasing system with one where cadres of trained and competent bureaucrats were directly responsible for the collection of all the Royal Treasury's income streams. Furthermore, direct management of the collection system by crown representatives met ideals such as centralization and more effective administration which had been instrumental in fuelling the start of the reforms.

Gálvez's first set of measures were resisted by Tomás Ortíz de Landázuri, contador general del Consejo de Indias (general comptroller of the Council of the Indies) with the support of the Consulado de México (Mexican Consulate). The latter was a body that brought together representatives of the most important merchants and import houses, which in a letter dated 22th December 1767, detailed their complaints about the reforms. To resolve the dispute, the then minister for the Indies, Julián de Arriaga, requested the intervention of Pedro Rodríguez Campomanes, fiscal del Consejo de Castilla (public prosecutor of the Council of Castile). In his long and meticulous report, Rodríguez effectively obliterated the main arguments against the fiscal reform. Rodríguez considered that the new method could "prevent by using fair and recognized means in all cultured Nations, the frauds which annihilated the Exchequer and destroyed legitimate commerce [...] the new rules were clear, easy, fair, destroyed vices, suitable for the public good".39

The reform also faced the challenge of ending the long established custom of interpreting colonial laws and regulations according to personal or local interests. It was common practice in the dominions that regulation from Spain was acknowledged but in fact it was seldom implemented.40

A major challenge that Gálvez had to tackle was ascertaining the fair value of the Royal Treasury's income streams. The income paid by contractors to the Royal Treasury appeared as a debit in the annual accounts of the Royal Public Office of Mexico,41 but as mentioned, the Royal Treasury lacked the means and relevant information.42 It seems the contractors were so secretive that no record of their transactions survived even for their contemporaries.

In summary, Gálvez introduced measures for the centralized and direct administration of the Royal Treasury's income streams during the last quarter of the 18th century. These measures brought about a radical change in the financial management of the Royal Treasury in New Spain, and included an exhaustive control of cash flows and detailed explanations of the concepts related to these cash flows as well as physical inventories related to individual income streams.

Changes in the accounting system of the Royal Treasury in New Spain

A consequence of the new measures for centralizing the administration of the Royal Treasury's income stream in New Spain was the introduction of changes in the accounting system. Initially the new accounting system used the método de cargo y data or partida simple (charge and discharge or single entry method), which envisioned, first, charging all the amounts perceived and, second, crediting all the amounts spent or delivered.43 Gálvez was thus following the prescribed method for public administration accounting in Spain since 1596.

However, according to Donoso,44 there was a first attempt to introduce double entry bookkeeping in all the royal public offices of the Indies in 1784. This included the Real Hacienda de las Indias or the Indies Administration Department in 1785.45 Donoso points to the years 1786 and 1787 as those marking the introduction and subsequent derogation of the double entry method in the management of the viceroyalty of New Spain. Rivarola46 provides additional empirical support by documenting developments in the province of Paraguay (viceroyalty of the River Plate).47 Rivarola's daily journals and ledgers for 1786 show that double entry was used only after 1784 and abandoned circa 1787. He also notes that there was no immediate return to single entry but to a "hybrid" method.48 At the time of writing, Domínguez49 was in the process of documenting similar developments for the general government of the viceroyalty of the River Plate.

Further empirical evidence in support of these authors was found in the General Archive of the Indies for the viceroyalty of New Spain, which enables the mapping of accounting studies in the public sector. The General Archive of the Indies held in reserve monthly cash flow statements of the monopolio or renta de la pólvora de Nueva España (New Spain's gunpowder monopoly).50 Figure 1 illustrates a facsimile of these statements for the 1786-1787 period, where entries appear ordered by debits and credits instead of the single entry or charge and discharge method.

As mentioned above, the differences between double and single entry methods were beyond issues of format and presentation. The financial statements of the double entry accounting system of the gunpowder monopoly included information about accounts receivable, whereas in the single entry that same information would have been added through off-balance sheet documents and specifically through sworn statements.51 Moreover, the double entry system resulted in the delivery of copies of the journal, ledger and cash book from the Council of the Indies to the General Accounting Office.

José de Gálvez returned to Spain in 1772. Upon his return he was appointed both minister of the Indies and president of the Council of the Indies in 1776. He held these offices until his death in June 1787. During his tenure, Francisco Machado, who replaced Tomás Ortiz de Landázuri as general comptroller of the Council of Indies, was the precursor of the establishment of double entry bookkeeping at the royal public offices of the Indies in 1786. The rationale was that with this method, the employees of the General Accounting Office could swiftly detect possible frauds or errors in the accounts.

After Gálvez's death, his successor as minister of the Indies, Antonio Valdes, commissioned in July 1787 several reports regarding the convenience of using double entry bookkeeping for the financial control of Spanish public administration. The people responsible for elaborating these reports were government employees that had not been involved in the process of introducing accounting reforms in the colonial administration.52 The reports were unanimous in asking for a return to the single entry method, using similar arguments to those used by Baron Von Bielfeld in his Institutions politiques of 1762. Valdes disregarded the arguments put forward by Machado and other top government officials in support of the double entry method while, at the same time, taking steps so that the king would fail to learn about alternative views. As a result, the double entry bookkeeping method was abolished from Spanish public accounting on the 25th October 1797.

Donoso53 claims that the rejection of double entry took place solely on the basis of political considerations. No evidence was found that double entry would cause technical or conceptual problems based upon which it could be deemed a lower quality method or considered an inferior accounting technique; but, at the same time, there was resistance to its adoption amongst civil servants in the colonies.54 For instance, the then viceroy of New Spain, conde de Revillagigedo, sent a letter to the Spanish crown defending the usefulness of "such an interesting development".55 The double entry system was abolished without considering its effects on the management of the royal public offices of the Indies. The latter were ignored simply because financial statements and books of accounts took two to three years to arrive in Spain. The double entry method was abolished before any such statements or books had physically arrived on the Spanish mainland. Thus, the double entry method was abolished irrespective of any difficulties or shortcomings encountered during its introduction in colonial institutions. Moreover, it was abolished whilst disregarding the support for double entry from government employees in the colonies.

Apropriation of double entry method in private enterprise

Las Ordenanzas de Bilbao (The Bilbao Regulations)

The most important regulation for private enterprise of that epoch in Spain and its colonies were the Ordenanzas de Bilbao (Bilbao Regulations).56 They were published in 1737 and effectively became the cornerstone of Spanish commercial law until the 19th century, when Spain unified its patchwork of codes and mercantile regulations.57 In chapter 9 ("Sobre los mercaderes y sus libros" or About Merchants and their Books) the regulator "Casa de Contratación de Bilbao" (Bilbao's Board of Trade) explicitly stated that accounts could be kept by following either the single or double entry method, leaving the ultimate choice to the merchant's own discretion. It is quite clear that both accounting methods were well known to members of the Board of Trade. Otherwise the Board of Trade would have been unable to point to them in such general terms. Yet the Regulations are mute on detailing the superiority of one or other accounting technique in any of the 723 articles. Instead, restoring and guaranteeing commercial good faith were recurrent topics. This suggests the latter were the priority for the Board of Trade in issuing its Regulations.

In principle the Regulations had a standing as supplementary law across the Spanish dominions but it is hard to ascertain the degree to which they were enforced and implemented. Moreover and as noted above, they were lax regarding the specifics of accounting systems. Thus opening opportunities for locals to design fit for purpose systems, that is, for the appropriation of accounting techniques within private accounting systems of colonial enterprises.

Along side opening opportunities for the appropriation of accounting methods, the passing of the Bilbao Regulations is also important as it broadly coincides with the publication of seminal contributions by Luis Luque y Leva58 and that by Sebastán Jócano.59 These books mark a revitalization and renewal in the production of Spanish accounting literature from 1770 onwards which, according to Hernández Esteve,60 together with the Regulations responds to a reinvigoration of economic activity in public and private organizations in the metropolis.

Controversies in Mexican historiography

Evidence is yet to emerge regarding the impact of the Bilbao Regulations over private accounting practices in Latin American at the end of the colonial period. But as far as the historiography of the New Spain is concern there is little consensus and even contradiction (as summarised in table 1). For one, Alvarado and colleagues state that in the decades that followed the birth of the Mexican Republic (after its independence from Spain in 1821): "[accountants in public and private enterprise] continued using standards and accounting practices developed under the colonial administration, with the further difficulty that volatility in the economic environment and political situation originated in confusion in public and private enterprise, losing with it the pressures associated with day to day practice".61

Alvarado62 also points to Manuel Payno's report to his successor as minister of Finance (circa 1850). In this report Payno gives his opinion on the failed attempt to introduce double entry bookkeeping in the Mexican central government during his tenure.63 The interpretation of this evidence by Alvarado and colleagues is to suggest that there was wide acceptance of double entry bookkeeping within private enterprise in the mid-19th century "otherwise [Manuel] Payno would not have complained about the lack of skills within the public sector".64 This view has some merit when considering that Rafael Cancino's translation of Deplanque's65 text was printed in Mexico City in 1844, that is, a year after its original publication in France. Cancino's translation,66 together with that by Bartolomé Salvador de Solórzano,67 are the oldest indigenous accounting textbooks currently on record in electronic libraries in Mexico. Their existence is consistent with contemporary late-19th century writings by Fonseca and Urrutia68 who describe the organization of the Accounting Court (but are mute on its practices). More recently, Rigoberto Cordero y Bernal69 notes that in 1877 core teaching requirements for secondary school education in the state of Puebla included double entry accounting.

A late development of "modern" accounting in private Mexican enterprise is also expressed by Alfredo Chavero e Híjar, Esq., C. P. A.70 who claims that "university lectures" in the 1900s taught single entry bookkeeping and dates widespread use of double entry bookkeeping to the late 19th and early 20th Centuries. Chavero's view coincides with the publication of several "novel books on modern accounting" in Mexico City as identified in the compilation by Rosendo Millán:71 firstly Tratado de teneduría de libros en partida doble (A Treatise on Double Entry Bookkeeping) by Eduardo Jiménez de la Cuesta in 1886; secondly, the Teoría de la partida doble (The Theory of Double Entry Bookkeeping) by Antonio Orozco in 1894, and thirdly, Tratado complejo de teneduría de libros por partida doble (A Complex Treatise on Double Entry Bookkeeping) by Emilio A. Marín in 1903. Both Chavero and Millán date the start of professional accounting in Mexico to two key developments; firstly, the creation of a contador de comercio (business accounting degree) in 1905 and of its first graduate, Fernando Díez Barroso, in 1907. Díez Barroso was instrumental in changing the title of graduates to contador público titulado (certified public accountant). Secondly, the establishment in 1917 of the Asociación de Contadores Titulados (Association of Certified Accountants).72

However, any view on the matter of an early or late adoption of modern accounting in private Mexican enterprise is largely speculative in the absence of systematic studies of surviving company documents. One exception is the use of double entry bookkeeping from an hacienda which was part of the estate of count Pérez Gálvez in Guanajato. The hacienda was a large, autonomous, self-sustaining holding of private land typically associated with agriculture or mining. During the colonial period these grew to be the dominant productive unit and remained so until the 1930s. Some of these engaged in international trade mainly by exporting agricultural products such as natural dyes (e. g. cochineal) or precious metals (e. g. silver). The Pérez Gálvez's hacienda is used by Gallo73 to claim that there was extensive use of double entry bookkeeping in the everyday trading of that hacienda in 1802 and that this should be seen as representative of accounting practice within private businesses of the time. He implicitly claims that double entry arrived some time before but fails to specify when or through which means. García Guidot74 also points to the same Pérez de Gálvez's hacienda in Guanajuato as well as the "thriving Mexican mining sector" as examples of the widespread use of double entry bookkeeping "at the dawn of the 19th century".75 García Guidot is thus in agreement with Gallo that there was widespread use of double entry in Mexico at the start of the 19th century. However, García Guidot76 dates the introduction of double entry bookkeeping to developments in public accounting and specifically the passing and adoption of the Instrucción práctica y provisional (Practice and Provisional Instruction) by the Contaduría General de Indias (General Accounting Office of the Indies) in 1774 and a real orden (Royal Decree) of November 26, 1787 by the Tribunal de Cuentas (Accounting Court).

In summary one is led to believe that at least in the mid to late-19th century there was intense interest in double entry accounting. But it is hard to ascertain if that was the case before or when exactly this accounting technique first arrived in Mexico. Opinions amongst Mexican authors and academic contributions to Mexican accounting history regarding the introduction of double entry are diverse and most if not all disregard developments in the early colonial period. In light of a lack of archival research, the next section discusses developments in Spanish historiography and private accounting in order to ascertain possibilities for early adoption and indeed appropriation by Novo Spanish firms.

The silence of Which LAMB?

Hernández Esteve77 was the first to introduce the idea that the 1630s saw the start of a third stage in Spanish accounting history: for the next hundred years or so, there was a general fall in the production of accounting manuals and textbooks in the kingdom of Castille. Donoso78 documents in detail this period, a time when double entry as a method "disappears" from regulation and accounting thought in Spain.

Other empirical studies have failed to clarify the extent to which double entry was indeed "forgotten". For instance, there are reports claiming that contemporary bookkeepers in Spain and elsewhere in Europe were familiar with the intricacies of double entry but these same studies admitted that this method was not evenly distributed amongst bookkeepers.79 Moreover, to date and to the best of our knowledge, the potential effect that the "silence and apparent oblivion" hypothesis might have had over public or private sector accounting in Latin America has not been documented. Hence there is a need to determine the impact of this "deceleration" in the production of analytical developments around double entry accounting in Spain during the 18th century and specifically, in the absence of surviving business records, whether this apparent oblivion helps to explain the contradictions in modern Mexican historiography. Determining the nature and scope of this apparent "silence" requires ascertaining whether there is evidence of a void in terms of analytical developments as well as in terms of everyday practice.

There is evidence to suggest that the dearth of an idiosyncratic production in Spanish accounting thought from the Mediterranean basin from circa 1630 to circa 1730 was substituted by (or remedied through the study of) foreign contributions. Some of these were read in the original whilst others were translated into Spanish. This fact emerges from evidence documented by Capelo and Álvarez-Dardet80 for Andalucian companies active in commerce across the Atlantic, as well as those by Manera81 for Mallorca, Franch82 for Valencia, and Vilar83 and Maixé-Altés84 for Catalonia.

Spanish traders and merchants particularly favoured Genovese authors85 as well as Sicilian writers,86 and other Italian authors.87 There is also evidence of a French influence.88

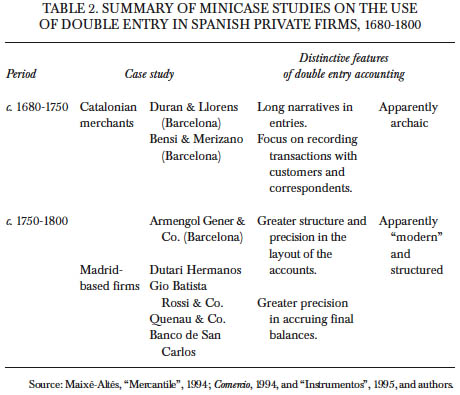

But what of everyday practice? The record is obscure as to whether business organization, especially in the maritime trade activities, had simply an intellectual interest in developments in "modern" accounting or whether these handbooks, guides and treatises actually influenced daily practice. Indeed, accounts of "silence and oblivion" in Spain have failed to pin point the nature of this phenomenon in specific geographical domains and types of business activity. In order to readdress this, the next section provides empirical evidence emerging from companies established in Madrid and Catalonia which effectively challenges the "silence and apparent oblivion" hypothesis. Table 2 summarises the discussion that follows. This is based on surviving records of accounting systems within private businesses whose activities were related to domestic and international commerce as well as some activities related to financial intermediation during the 17th and 18th centuries. Admittedly, Catalonian and Madrid-based firms were unlikely to be fully involved in transatlantic trade.89 However, this evidence documents how double entry became rooted in the accounting system of wholesalers during the course of the second half of the 17th century. This evidence thus helps to support the idea that, during this period, different levels of complexity coexisted. It provides evidence not only of continuity but also of appropriation as accounting systems could be more or less sophisticated according to the users' "needs" and the nature of their business.90 Of course this, in turn, opens up the question as to whether coexistence of accounting systems in Spain was also the case for organizations in New Spain.

Accounting for domestic and international wholesale trade in the Mediterranean

There are noticeable differences in bookkeeping practices within compañías de comercio or casas de comercio (merchant houses) based along the Spanish Mediterranean coastline at the end of the 1690s from the accounting practices these same companies used after the 1750s. These differences are greater in terms of analytical precision than accounting method. Below evidence is provided to support the idea that greater analytical precision resulted from a combination of overall economic growth and business practices of individual firms. Indeed during the 18th century the turnover of Catalonian businesses grew substantially while individual wholesalers aimed to diversify their investments. As the examples that follow suggest, double entry bookkeeping was well established. But it was the need to ascertain the profitability of different investments the element that instigated a more detailed set of accounts and sophisticated bookkeeping system. This suggests that the bookkeepers of 1699 or 1725 were as skilled and knowledgeable as those of the 1750s.91

Surviving records of two merchant houses helped to ascertain continuity in the use of double entry accounting. On the one hand, Duran & Llorens provided an insight into their accounting practices for the last decade of the 17th century and early years of the 18th century. On the other hand, similar records were available for Bensi & Merizano between 1724 and 1750.92 Together they provide a first approximation to the changes in accounting practice between those typical of the first half of the 18th century and those at the end of that century.

The accounting system at Duran & Llorens displayed all the technical characteristics of double entry bookkeeping as they kept the two basic books, libro diario or manual (the daily journal) and libro mayor (the ledger).93 The basic accounts were perfectly defined: for example, the cash account in the assets/debits side and the capital account in the liabilities/ credits side. The principal analytical difficulty of these accounting books related to the lack of definition of what 19th century authors called cuentas transitorias (auxiliary accounts). Here clearly defined accounts were only found for debits and credits relating to the profit and loss account. The use of other accounts, such as general expenses account, is inconsistent, while other "first class accounts" such as those to register cambios marítimos (bottomry contracts),94 bills of exchange and commissions, were nonexistent.95 Hence, this only offered a collection of accounts that lacked any aggregate analytical concepts on debits and credits.

The only accounts that showed a certain degree of "maturity" in that regard were called customer current accounts and current accounts for correspondents. These were representative of accounting practices at that point in time because in their construction bookkeepers indistinctively mixed debits and credits. This particular organization of the accounting plan responded to the interweaving of two idiosyncratic elements of Catalonian accounting in the early 18th century.96 On the one hand, until the middle of the 18th century entries in ledgers by bookkeepers in Catalonian companies followed the entry style of the primary books. This involved a rather descriptive type of entry, which was closer to an explanation in the draft book or the journal than to the rather "analytical" nature of the charge and discharge system of the ledgers. There was thus no basic function, system, key or index to reconcile the whole system of accounts. On the other hand, the rather archaic, disaggregated and unconsolidated nature of Catalonian accounting systems also responded to the diversification of Catalonian investment portfolios. Businessmen opened a dedicated account for every business and even individual investments. The idea was that, at a later date, this approach would facilitate prompt recognition of the profit or loss for each and every transaction. The analytical nature of this approach was evident in the fact that these accounts were consolidated into a balance sheet.97

Strong similarities were also found when comparing the accounting system at Duran & Llorens with that at Bensi & Merizano. A superficial examination of the accounting system at Bensi & Merizano could have branded it as elementary, archaic, and even backward in comparison with that at Duran & Llorens. But closer examination suggested that accounting at Bensi & Merizano offered a large degree of flexibility. The accounting plan opted for a procedure that gave analytical priority to the customer-correspondent. As a result, entries for personal current accounts predominated within the ledger. The ledger as the key source of information for the running of the business focused on two concepts: it informed and provided details of account balances for all the intermediaries of the company and it also provided a summary of profit and loss per account.

Other information could be obtained by consulting two auxiliary books, namely the invoice book and the libro de tratas (bill of exchange book). The invoice book recorded information regarding the exchange of goods while the second book recorded future payments.98 Several objections could be made to the accounting plan at Bensi & Merizano. However, we must admit that its approach seemed "fit for purpose" when considering other options for a medium-sized company, with a highly diversified business portfolio (that encompassed both mercantile trade and financial services) and a business model geared towards fee income generation. Moreover, building the accounts system around personal current accounts offered the possibility of a prompt and swift calculation of the balance sheet.99

Accounting systems at Duran & Llorens and Bensi & Merizano seemed to be in contrast with the practices and accounting plans of other businesses in Catalonia during the second half of the 18th century. For instance, practices at Armengol Gener & Co. in 1747 have been documented as the first case of a well structured accounting system as well as representative of the "modern" practices pursued by 18th century companies in Barcelona. Firstly, the "basic" accounts were found to be perfectly determined: capital account, profit and loss, cash, overheads, fee income and commissions, bottomry contracts, diners deixats a la part (income derived from the medieval commenda contracts), insurance and barca (the share of ownership of merchant ships). Secondly, accounts to record transactions around bills of exchange followed a mixed system. In 1747 this mixed system was consolidated into a single account (cuenta de sacas y remesas). Later on, however, growth of trading and financial activity resulted in the creation of new accounts.

Thirdly, accounting for merchandise trade and commerce also offered a system geared towards the business model of Armengol Gener. This part of the accounting system was found to offer greater precision and aggregation of the entries than those relating to the bill of exchange account and "basic" accounts, although it should be noted that there was a bias towards creating individual accounts by business sector or type of goods traded. Hence, there was a high degree of personalized entries (reflecting significant personal customers and business correspondents). However, a key element of the accounting system of Armengol Gener was the precision and speed at which they could draft a closing balance sheet. For instance, the ledger systematically recorded initial and final balance statements for every year. These balances clearly specified creditors and debtors as well as the different concepts contributing to overall profitability of the business, providing a snapshot of the financial situation of the company at that point in time.

The accounting practices at other highly diversified businesses, such as the business activities of the Glòria family and merchant house Huguet & Dupré at the end of the 18th century as well as Cristóbal Roig & Co. in the first quarter of the 19th century, bear great similarity to the system pioneered by Armengol Gener (1747-1784).100

This evidence helps to support the claim that by the 1750s the double entry system was used by some family firms and merchant houses in Barcelona with a certain degree of sophistication and structure. Yet at the same time, great variety can be observed in the accounting practices of Catalonian and many other merchant houses established within the Mediterranean basin. But this does not mean that some firms with rather archaic accounting practices developed qualitatively inferior businesses, when compared to other businesses with apparently more structured system of accounts.101 Our evidence suggested that many merchant houses kept their accounting system largely unchanged and ran their organization based on tailor-made approaches to their small volume of trade and high degree specialization in investments and business portfolio.

There could be a temptation to classify the accounting systems at merchants such as Duran & Llorens and Bensi & Merizano from 1690 to 1750 as confusing and archaic when compared to the "technically modern systems" at merchant houses such as that of Armengol Gener from 1747 to 1784. However, the evidence presented above suggests that such a view would be somewhat inappropriate because all of these accounting systems ultimately rely on double entry bookkeeping. Their design and resulting reports were quite different, and given the absence of detailed regulation or generally accepted accounting principles, each followed a number of practices which were largely idiosyncratic to the custom and business model of the merchant or family firm.

A brief comparison of accounting practices in catalonian and Madrid-based firms

Comparing accounting systems Catalonian companies between circa 1675 and 1800 (all of which build on the concept of double entry) with Madrid-based firms in the second half of the 18th century is interesting since the latter offer the opportunity to analyze firms involved in "domestic" trading within the Iberian peninsula as well as being involved in foreign trade and financial services.

Further analysis of the accounting practices at Dutari Hermanos suggests that from 1742 onwards this company developed significant financial service activities by providing credit in the form of discounting bills of exchange and direct loans to businesses involved in the production of Castilian wool. A similar analysis was carried out of the activities of Gio Batista Rossi after 1758, Quenau & Co. after 1759 and Banco de San Carlos after 1782.102 Besides having an important part of their business located in Madrid, they all engaged in financial services, as they all acted as independent clearing houses for bills of exchange and offered bureau de change facilities to customers. Another common characteristic was that they all developed a double entry bookkeeping system with a "classic" structure, that is, using the ledger and journal for the management of their accounting system.

At Dutari Hermanos, for example, discounting bills of exchange was one of the most important income generating activities of the company, so naturally it had a bearing on the account plan. These activities required keeping detailed records and control of the number of days elapsed since an advance was made (whether in the form of a direct loan or discounting a bill of exchange). This tally was the basis for calculating accumulated interest. To record the transaction several auxiliary books were used together with the journal and ledger. These auxiliary books included one for cash, one for discounted bills of exchange and another for outstanding bills of exchange.103 Recording changes in bills of exchange, discounting and other credit operations all the way through from auxiliary books to the journal and ledger is thus evidence that suggests an accounting system based on double entry.

In summary, this section documented evidence from Catalonian firms involved in wholesale international trade and investment together with Madrid-based firms involved in domestic and foreign trade and financial services, suggesting that double entry bookkeeping was common practice in the accounting of private firms in the Spanish mainland at the end of the 17th century and during the 18th century.

A proposal for further research

To the best of our knowledge there is no systematic study that documents links in the use of "sophisticated" accounting technology between Spain and its colonies in Latin America in both public and private enterprise. Research in this article helps to fill this gap by putting forward the idea that future studies of Latin American accounting history should be framed by the evolution of accounting practice in Spain. These studies should offer a synthesis that emerges from different contemporary sources such as textbooks and manuals, surviving company and government records as well as paying attention to educational practices. Furthermore, there is evidence to suggest that different accounting systems coexisted for long periods within Spanish early modern capitalism, sometimes even in the same organization. That is, different organizational forms in Spain are seen as adopting the accounting system that best suited their purpose and business model. In the absence of empirical evidence to the contrary, there is reason to believe that private firms on the west coast of the Atlantic also adopted fit-for-purpose accounting.

The point of departure to illustrate the above is a reinterpretation of indigenous contributions and non-native authors discussing the arrival of double entry bookkeeping in private and public accounting in Mexico. These contributions debate whether there was continuity or discontinuity in Mexican practice immediately after independence from Spain (i. e. the end of the colonial period). The comparison between, on the one hand, Federico Gertz Manero, Luis de la Puente, Alvarado et al., and Rodríguez and Yáñez104 and, on the other hand, García, Gallo and Avella105 suggests that double entry bookkeeping was known in Mexico during the last decades of the 18th century. This view claims that there was some initial success, while the handful of systematic studies by indigenous authors and academics studying Mexico are somewhat biased towards developments in the public sector.106

There seems to be some consistency in the view that this accounting technique diffused at lukewarm pace so that it was "overlooked" as a practice during the first half of the 19th century. Double entry bookkeeping was then reintroduced from 1850 onwards, first in some private firms, as suggested by the publications of Deplanque107 and Salvador.108 This was followed by its adoption in central government thanks to its successful use within the Mexican Army109 and as a remnant of French military intervention.110 Meanwhile, foreign direct investments from the USA, France and Britain during the porfiriato (1876-1910) brought about its widespread use within private enterprise.111

Throughout the above studies, however, there is an implicit assumption that accounting manuals and textbooks are an unbiased reflection of the development of accounting practice and thought. At the time there were some formal education outlets. Mexico City was home to the oldest university in the continent112 and there were some institutions offering business administration and accounting courses,113113 but by and large most of the knowledge transfer during the Spanish American Empire is most likely to have taken place through informal, on-the-job training (such as apprenticeships or visiting stays).

The existence of surviving contemporary manuals and textbooks can be a helpful but not a decisive piece of information in determining everyday accounting practices. Indeed, there is evidence documented for other geographies which points to the development of accounting regardless of an absence of accounting texts and university curricula. For instance, Fleischman and Parker114 point to this conclusion in the context of cost-accounting during the British Industrial Revolution. In an independent study, Edwards and Boyns115 state that despite the lack of any significant industrial accounting literature to guide them, businessmen and key individuals employed or developed accounting techniques in British private enterprise.

Moreover, the above citations from Mexican authors and non-natives studying Mexican accounting practice fail to make a clear distinction as to whether the double entry method was established in the public sector or in the haciendas (and more precisely, whether any of these were involved in international trade with merchant houses in Spain). This blurring of economic activity is as much a concern as the assumptions regarding the speed of diffusion of "modern" accounting in Mexico.

In summary, all authors identified above have made implicit or explicit claims regarding how the continuity of accounting practice in New Spain was subject to vicissitudes in its colonial ruler, while disregarding possibilities for the appropriation of accounting techniques. It is indeed fair to assume that the introduction of double entry bookkeeping in Mexico was influenced by practices and institutions in Spain during the colonial period. As mentioned above, Hernández Esteve116 notes that 150 copies of Bartolomé Salvador de Solorzano's treaty on double entry accounting were taken by Diego Felipe de Aldino and Bartolomé Porras in 1591 to be sold in New Spain. But when exactly Mexicans adopted double entry bookkeeping, and to what extent there were differences and similarities between private and public enterprise, remain primary unresolved issues.

The path of adoption and diffusion of this accounting technology in Spain provides a framework to begin ascertaining the likelihood of adoption given the handful of sources that survive from pre-independence Mexico. A brief summary of the historiography of double entry in Spain noted that some Spanish authors have pointed to an apparent crisis in Spanish history of double entry while pointing to a desertion in the use of this method between the 17th and 18th Centuries. However, through the analysis of surviving company records, evidence documented in this article shows how the technique had a much wider use in private companies than is otherwise claimed. This is very much the case for firms involved in large volume business or diversified investments. This result was in line with developments documented elsewhere and in particular around Anglo-American accounting.

That evidence also led us to believe that, first, the apparent desertion (at least as far as the production of Spanish bibliographic material is concerned) must be understood in the context of the predicaments and general chaos that characterized the end of the Hapsburg dynasty. This period had a significant impact on accounting regulation and doctrinal production in Spain. The Hapsburg's economic mismanagement was also instrumental in decimating the number of skilled practitioners by reducing opportunities for training new cadres of competent bookkeepers. At the same time, large numbers of bankruptcies and business failures with the consequent reduction of surviving records significantly lowered possibilities of studying this epoch systematically. Hence one must be careful not to equate a "slow down" in the diffusion of the double entry method in Spain with total desertion or even neglect of this accounting technology.

Second, this article presents evidence which suggests that the use of double entry method had taken a hold in firms established in the more industrious geographies of Spain by the 1690s. There is no reason to believe that firms outside of the colonial powerhouse and particularly those based in New Spain and involved in foreign trade or investments in Asia and the Caribbean, were excluded from learning about the double entry method. However, it is likely that Novo Spanish firms adopted European accounting technologies with some delay and chiefly through interaction with peers in business and commerce as well as migration of skilled employees and entrepreneurs. This is because "on-the-job training" rather than formal education was the chief method for knowledge transfer. But as noted above, the crisis at the end of the Hapsburg Empire could have disrupted opportunities for knowledge transfer to the colonies. One is thus led to believe that this accounting technique was first adopted in New Spain as early as the 17th century. This claim would position its adoption considerably earlier than that suggested in most Mexican contributions. But since were unable to provide evidence in this regard, the validity of our claim remains hypothetical and subject to future empirical research.

Third, with regards to the public sector, it could be said that public accounting systems may have had a lesser degree of complexity when compared with the requirements of private accounting systems, but in fact the accounting systems of public and private bodies were very different during the early modern capitalist era. It would be erroneous to think they are equivalent mainly because the analytical criteria of each type of corporate body were very different. For instance, evidence has been provided of accounting systems in private firms which specifically associated with a large number of accounts and accounting books whereas in others there was no variety and they followed more traditional practices. Key concepts for private firms include capital, profits and the role of partners, whereas these same concepts are non-existent for public administration.

Nonetheless, our interest in highlighting the comparison of public and private bodies is that public accounting systems introduced criteria that went beyond the charge and discharge method much earlier than anticipated by Mexican historiography. Admittedly this effort seemed more successful in Spain than in its colony. Indeed, the numerous forms of Spanish institutions and administrations (municipalities, colonial, etc.) first introduced the double entry method during the second half of the 16th century. At the beginning of the 17th century the Spanish Treasury and other public administrative bodies developed double entry accounting systems, while it was in the middle of the 18th century that the Bourbon introduced double entry bookkeeping to colonial public administration (although these efforts were not always successful). Specifically, top officials of the viceroyalty of New Spain (namely administrators at the Accounting Court and General Accounting Office of the Indies) were keener to adopt double entry bookkeeping than top officials in colonial administrative bodies. However, it seems that the progressive deterioration of political and economic control of the dominions at the end of the 18th century together with non-standardized rules (i. e. no concept of generally accepted accounting principles) and the processes leading to independence, generated a break up in New Spanish-Mexican accounting practices which indigenous firms most have found difficult to solve in the short term.

The lack of clarity regarding accounting practice at the end of the colonial period and during the early independent Mexico, probably resulted in an informal setting where some individuals employed double entry bookkeeping while others in similar organizations stuck to the charge and discharge method. This view helps to explain why our survey of Mexican sources apparently found contradicting claims based on surviving records of several haciendas and mines at the beginning of the 19th century. The volatile economic and political climate that followed included mass outward migration of Spanish businessmen and capital, and the separation of Central American states as well as armed conflict with France and the USA, the latter resulting in the loss of over half the territory at independence from Spain. Moreover, industrialization in Europe meant a loss of many traditional export markets for natural dyes. All this had a profound effect on any attempt by the former colony to regain continuity in accounting practice. In fact and as above mentioned, it was not until the second half of the 19th century when a more stable economic and political environment and a reintroduction of European investments and some migration, when the modernization of the economic system entailed the gradual introduction of double entry bookkeeping in Mexico. The introduction and adoption of double entry bookkeeping in Mexico was thus a consequence of knowledge transfer from its former colonial ruler as much as a consequence of institutional "normalization".

Lastly, some caveats. First, our research documented evidence from Madrid-based firms involved in domestic and foreign trade and financial services, together with Catalonian firms involved in wholesale international trade and investment, suggesting that double entry bookkeeping was common practice in the accounting of private firms in the Spanish mainland at the end of the 17th century and during the 18th century. This evidence contests the current framework for the historical analysis of accounting technology in Spain and in particular, the soundness of the so called "stage of silence and apparent oblivion" hypothesis.117 It must be acknowledged that Madrid-based and even more so Catalonian merchant houses were, in general, excluded from trade with the American colonies in the early colonial period. However, there is enough evidence to suggest the possibility of an early adoption of this technique in Latin America and that this could have happened much earlier than anticipated by Mexican historiography.

Second, this article is not making the claim that there was generalized use of double entry in Spain during the 17th and 18th centuries. The absence of widely accepted accounting principles together with the slowdown in intellectual and economic environments at the end of the Habsburg Monarchy in Spain118 resulted in many bookkeepers devising accounting systems that best fitted the purpose of their organization. The accounting practices in firms of different sizes and degrees of diversification discussed above, suggest that the nature of the accounting system and the prevalence of rudimentary methods was strongly influenced by the business model and the level of complexity in their operations, complexity that arose from a combination of the type of market they were involved with and the volume of their trade. Our evidence thus suggests that double entry bookkeeping was most likely to be found amongst large or diversified organizations. These were the types of firms that usually engaged in trade with others elsewhere in Europe and the American dominions, thus opening up the possibility for technological transfer to private firms established in the colonies. Of course, the use (even if widespread) of this accounting technique in Spain is not in itself sufficient to make a similar claim for its colony. There is a possibility for other accounting techniques to have had been more suitable in New Spain. As a result, this article offers a robust, empirically-based, new framework to assess future evidence regarding accounting practice in Mexico and elsewhere in Latin America during the Spanish colonial era.

Sources consulted

Archives

AGI Archivo General de Indias, Sevilla, Seville, Spain.

AHBE Archivo Histórico del Banco de España, Madrid, Spain. Secretaría: Dutari Hermanos, libros 18560, 18637, 18638, 18616; Gio Batista Rossi, libros 18558, 18559, 278P, 235P, 272; Rossi, Gosse & Co., libro 322; Casa Quenau, libros 272, 423, 453; Banco de San Carlos, libros, 240, 246, 251.

AHPB Arxiu Històric de Protocols de Barcelona, Barcelona, Spain.

AHMB Archivo Histórico de la Ciudad de Barcelona, Cataluña, Spain.

ACM Archivo y Biblioteca de Can Mayans, Vilassar de Dalt, Barcelona, Spain. Private records of the landed estate of the Bensi-Olmera's family.

AD Archivio Storico dei Durazzo, marchesi di Gabiano, Genoa, Italy. Private archive.

Hemerography

El Universal, Mexico City. [ Links ]

Bibliography

Alberts, Gerard, "Appropriating America: Americanization in the History of European Computing", Annals of the History of Computing, Institute of Electrical and Electronics Engineers, vol. 32, num. 2, April-June, 2010, pp. 4-7. [ Links ]

Alvarado Martínez y Escobar, Lourdes et al., La contaduría pública: estudio de su génesis y de su evolución hasta nuestros días, México, Universidad Nacional Autónoma de México, 1983. [ Links ]

Amato ed Urso, Giuseppe Carlo, Il microscopio de computisti, Palermo, A. Felicella, 1740. [ Links ]

Anes, Gonzalo, Historia de España, Miguel Artola (ed.), vol. 4, Madrid, Alianza Editorial, 1994. [ Links ]

Anonymous, Reflexiones sobre el acuerdo del Senado, relativo a la adopción del sistema de partida doble, para las cuentas del erario público, México, Imprenta de José Mariano Lara, 1850. [ Links ]

Arcila Farías, Eduardo, El siglo ilustrado en América: reformas económicas del siglo XVIII en Nueva España, Caracas, Ediciones del Ministerio de Educación, 1995. [ Links ]

Avella Alaminos, Isabel, "La experiencia de la partida doble en la Real Hacienda en la Nueva España (1784-1789)" in Ernest Sánchez Santiró, Luis Jáuregui and Antonio Ibarra (eds.), Finanzas y política en el mundo iberoamericano: del antiguo régimen a las naciones independientes, 1754-1850, México, Universidad Nacional Autónoma de México, 2001, pp. 115-138. [ Links ]

Baños Sánchez-Matamoros et al., "Govern (mentality) and Accounting: the Influence of Different Enlightenment Discourses in Two Spanish Cases (1761-1777)", Abacus. A Journal of Accounting, Finance and Business Studies, University of Sidney, vol. 41, num. 2, June, 2005, pp. 181-210. [ Links ]

Bátiz-Lazo, Bernardo, "Business Elite and the Diffusion of US-Style Business Education in Mexico (1955-2005)", Research Papers in Economics, 2008, Leicester, <http://ideas.repec.org/p/pra/mprapa/7473.html>. [Accessed: 26 Nov., 2011. [ Links ]]

Bici, Antonella, "Modelli di contabilità nella seconda metà del Seicento" in Simonetta Cavaciocchi (a cura di), L'impresa industria commercio banca (secc. XIII-XVIII), Firenze, Le Monnier, 1991, pp. 393-397 (Serie ii, Atti della Settimane di Studio e Altri Convegni, 22). [ Links ]

Capelo Bernal, María Dolores and Concepción Álvarez-Dardet Espejo, "La reputación de los gestores y su elección contable: el caso del almacén central de Agüera (1822-1830)", Revista Española de Financiación y Contabilidad, Asociación Española de Contabilidad y Administración de Empresas, vol. XXXIII, num. 121, April-June, 2004, pp. 281-312. [ Links ]

Carmona, Salvador, "Accounting History Research and its Diffusion in an International Context", Accounting History, Accounting History Special Interest Group of the Accounting and Finance Association of Australia and New Zealand, vol. 9, num. 3, November, 2004, pp. 7-23. [ Links ]

Carnegie, Gary D. and Lúcia L. Rodrigues, "Exploring the Dimensions of the International Accounting History Community", Accounting History, Accounting History Special Interest Group of the Accounting and Finance Association of Australia and New Zealand, vol. 12, num. 4, November, 2007, pp. 441-464. [ Links ]

Carnegie, Gary D. and Robert H. Parker, "The Transfer of Accounting Technology to the Southern Hemisphere: The Case of William Butler Yaldwyn", Accounting, Business and Financial History, Routledge, vol. 6, num. 1, 1996, pp. 23-49. [ Links ]

Casaregis, Josephus Laurentius Maria de, Discursus legales de commercio, Venecia, ex Typographia Balleoniana, 1740, 3 vols. [ Links ]

Cordero y Bernal, Rigoberto, Historia de la contaduría en Puebla, Puebla, Centro de Estudios Históricos de Puebla, 1997. [ Links ]

Deplanque, Luis, La tenue des livres en partie simple et en partie double..., Paris, Dutertre, 1843. [ Links ]

----------, La teneduría de libros en partida simple y doble, puesta al alcance de todas las inteligencias para ser aprendida sin maestro, trad. Rafael Cancino, México, Imprenta de Vicente García Torres, 1844. [ Links ]

Domínguez, Manuela, "El sistema de intendencias y su influencia en la estructura organizativa y recaudación de la hacienda: el caso del virreinato del Río de la Plata (1776-1782)", XIII Jornadas Hispano Lusas de Gestión Científica, Baeza, 2009. [ Links ]

Donoso, Alberto, "La contabilidad virreinal americana, análisis de una experiencia: la aplicación del método de la partida doble en las Reales Cajas de Indias (1784-1787)", doctoral dissertation, Seville, Universidad de Sevilla, 1996. [ Links ]

----------, "Estudio histórico de un intento de reforma en la contabilidad pública: la aplicación del método de la partida doble en las Cajas Reales de Indias (1784-1787)", Revista Española de Financiación y Contabilidad, Asociación Española de Contabilidad y Administración de Empresas, vol. XXVII, num. 93, October-December, 1997, pp. 1045-1089. [ Links ]

----------, "Nuevo método de cuenta y razón para la Real Hacienda en las Indias. La instrucción práctica y provisional en forma de advertencias comentada (27 de abril de 1784)", Revista Española de Financiación y Contabilidad, Asociación Española de Contabilidad y Administración de Empresas, vol. XXVIII, num. 101, July-September, 1999, pp. 817-862. [ Links ]

----------, "El virrey de Lima, caballero de Croix, defensor de la partida doble en el siglo XVIII", Revista Española de Financiación y Contabilidad, Asociación Española de Contabilidad y Administración de Empresas, vol. XXX, num. 107, October-December, 2001, pp. 165-206. [ Links ]

Donoso, Rafael, Una contribución a la historia de la contabilidad: análisis de las prácticas contables desarrolladas por la tesorería de la Casa de la Contratación de las Indias de Sevilla (1503-1717), Seville, Universidad de Sevilla, 1996. [ Links ]

Edwards, John R. and Trevor Boyns, "The Construction of Cost Accounting Systems in Britain to 1900: the Case of the Coal, Iron, and Steel Industries", Business History, Routledge, vol. 39, num. 3, July, 1997, pp. 1-29. [ Links ]

----------, "The Development of Cost and Management Accounting in Britain" in Christopher S. Chapman, Anthony G. Hopwood and Michael D. Shield (eds.), Handbook of Management Accounting Research, vol. 2, Amsterdam & London, Elsevier Science, 2007, pp. 969-1034. [ Links ]