Serviços Personalizados

Journal

Artigo

texto em

texto em  Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Acessos

Acessos

Links relacionados

-

Similares em

SciELO

Similares em

SciELO

Compartilhar

Permalink

PermalinkProblemas del desarrollo

versão impressa ISSN 0301-7036

Prob. Des vol.46 no.183 Ciudad de México Out./Dez. 2015

https://doi.org/10.1016/j.rpd.2015.10.004

Articles

External Constraints on Growth in Argentina: The Role of Industrial Manufactured Goods

a Centro de Estudios de la Estructura Económica (CENES), Universidad de Buenos Aires, Argentina

Recent tensions in the current accounts of Argentina have reopened the debate regarding external constraints on growth (ECG). In 2003-2013, export growth was slightly lower than it was during the convertibility era, but a major decline in the income elasticity of import demand mitigated the ECG. However, the effective growth rate was higher than that imposed by the ECG, according to Thirlwall's law, which led to the deterioration of the trade balance and growth. This was due to the trade deficit in manufactured goods of industrial origin (MIO), in light of technology dependence in capital goods and inputs. This paper analyzes the evolution of ECGs in Argentina at both the global and sector level, aiming to determine which MIO sectors had the greatest impact.

Keywords: Argentina; manufacturing industry; external sector; foreign trade; structural change

Las recientes tensiones en la cuenta corriente de Argentina reabrieron el debate sobre la vigencia de la restricción externa al crecimiento (REC). Durante 2003-2013, la expansión de las exportaciones resultó levemente inferior al periodo de la convertibilidad, pero una fuerte merma en la elasticidad-ingreso de importaciones permitió una atenuación de la REC. Sin embargo, la tasa efectiva de crecimiento fue superior a aquella que impone la REC según el criterio de Thirlwall, lo que fue deteriorando el balance comercial y el crecimiento. Esto se debe al déficit comercial en manufacturas de origen industrial (MOI), ante la dependencia tecnológica en bienes de capital e insumos. Este trabajo analiza la evolución de la REC en Argentina a nivel global y sectorial, a fin de detectar las ramas MOI de mayor impacto sobre la misma.

Palabras clave Argentina; industria manufacturera; sector externo; comercio exterior; cambio estructural

Les récentes tensions qu'a souffertes le compte courant de l'Argentine ont rouvert le débat sur l'opportunité de continuer à appliquer la restriction externe à la croissance (REC). Durant la période 2003-2013, l'essor des exportations s'est avéré légèrement inférieur à celui de la période de convertibilité, mais une forte réduction de l'élasticité-revenu d'importations a permis d'atténuer la REC. Cependant, le taux de croissance réel a été supérieur à celui qu'impose la REC selon le critère de Thirlwall, ce qui a détérioré la balance commerciale et freiné la croissance. Cela est dû au déficit commercial dans le domaine des manufactures d'origine industrielle (MOI), confronté à la dépendance technologique quant aux biens d'équipement et fournitures. Ce travail analyse l'évolution de la REC en Argentine aux niveaux global et sectoriel, afin de discerner quelles branches MOI ont le plus d'effet sur celle-ci.

Mots clés Argentine; industrie manufacturière; secteur externe; commerce extérieur; changement structurel

As recentes tensões na conta corrente da Argentina reabriram o debate sobre a vigência da restrição externa ao crescimento (REC). Durante 2003-2013, a expansão das exportações resultou ser levemente inferior ao período da convertibilidade, mas uma forte diminuição na elasticidade-renda das importações permitiu uma atenuação da REC. No entanto, a taxa efetiva de crescimento foi superior àquela que impõe a REC segundo o critério de Thirlwall, o que foi deteriorando a balança comercial e o crescimento. Isto de deve ao déficit comercial em manufaturados de origem industrial (MOI), dada a dependência tecnológica em bens de capital e insumos. Este trabalho analisa a evolução da REC na Argentina a nível global e setorial, a fim de detectar as ramas MOI de maior impacto sobre a mesma.

Palavras-chave Argentina; indústria manufatureira; setor externo; comércio exterior; mudança estrutural

近期阿根廷经常收支的紧张局势再次引发了关于经济增长外部约束(REC)有效性的讨论。2003-2013年间阿根廷出口扩张速度较货币管制阶段略有 下降,进口收入弹性急剧下降,这使得REC有所减缓。然而,经济实 增速 优于强制按照瑟尔沃尔标准实行REC时的速率。后者导致了贸易平衡的日益 恶化及经济增长的日益放缓。究其原因,主要在于工业制成品(MOI)对资 本和货物的技术依赖而造成的贸易赤字。本文分析REC在阿根 全国及部门 范围内的演变,以探究影响最大的工业制成品(MOI)分支。

关键词 阿根廷; 制造业; 对外部门; 外贸; 机构变化

I. INTRODUCTION

Structural imbalances have long ailed the Argentine economy, hitting rock bottom during the decade of convertibility. The economic policy implemented during those years, which was responsible for the destruction of multiple sectoral production chains and job losses, generated a specialization pattern that exacerbated the imbalances of the external sector, causing a recession and the crisis at the end of the 1990s. The destruction of productive chains deepened Argentina's dependence on investment growth in capital goods and imported inputs, which tied economic growth to imports.

On the contrary, in the first years following the end of convertibility between the Argentine peso and the dollar, the country experienced marked growth (and industry played a major role) with an external surplus. However, the tensions that have showed up in the current accounts since 2011, which led the country to implement restrictive foreign exchange policies and to enforce import controls, have brought up new questions regarding the external sector. We might wonder: Did the process that took place between 2003 and 2013 truly manage to mitigate external growth restrictions? Were there transformations in the productive profile that could make high economic growth rates sustainable?

This paper shall seek to answer these questions by analyzing the changes that the industrial structure has undergone and taking into account other components of the current account balance that drive external growth restrictions.

Section II will present some theoretical approaches that link the productive structure, the balance of payments, and the sustainability of growth. Then, in Section III, we will take a look at how the current account of Argentina evolved in the 1990s and 2000s. Section IV will compare (using the Thirlwall method), both overall and for some specific industrial sectors, growth levels and the external sustainability achieved during these years. Finally, we will offer our conclusions.

II. STRUCTURALISM, THE POST-KEYNESIAN SCHOOL, AND THE LINK BETWEEN THE PRODUCTIVE STRUCTURE AND THE BALANCE OF PAYMENTS

There is vast theoretical literature regarding the relationship between the productive structure, growth, and the sustainability of a balanced balance of payments, especially from two schools of thought: the structuralist and post-Keynesian schools.

From the time of its origins, the structuralist school dealt with analyzing the interaction between the economic structure of a country and its international pattern of insertion. Prebisch (1986) signaled that the deteriorating terms of exchange did not permit the benefits of technical progress in the industrialized center to be distributed to peripheral countries (exporters of primary goods) through the mechanism of international prices, which entailed an obstacle to growth. Other authors, such as Braun and Joy (1968) and Diamond (1972), have parsed the specific impact of primarization on the economic cycle, from which the external restrictions that cause the stop and go cyclical movements are derived. This consists of a growth phase (when investment and the product grow) in which the number of jobs and real wages rise, and the demand for national and imported industrial goods increases (and a portion of the exportable balance), until this forces a nominal devaluation due to the harm derived from the trade balance; and a contractive phase which, beginning with the depression of real wages, generates the conditions for a new cycle of growth.

The post-Keynesian tradition synthesized, in a stylized manner, these considerations through Thirlwall (1979): a sustainable economic growth rate in the long term, such that it would not be limited by external restrictions, formally depends on the ratio between the export growth rate and the income elasticity of imports. To Thirlwall, the differences between sustainable growth rates between countries should be "associated with the characteristics of the goods produced" (1979). In other words, the export growth rate depends on the level of activity of the rest of the world, but also on the sectoral composition of the exports; while the income elasticity of imports is also determined by its sectoral composition, and by the capacity to substitute imports with local production.

If we revisit the case of countries specialized in the primary sector, external growth restrictions are imposed in the long term, because the demand for exportable primary goods is more inelastic with respect to income than the demand to import industrial goods (Prebisch, 1973). However, the low short-term price elasticity of the supply of primary goods, due to the existence of productive factors that cannot be reproduced (such as arable land and oil wells), can push prices up when there is strong surplus demand (Cepal, 2008). This process can generate positive effects for the trading terms of primarized economies in the short term, but the long-term structural capacity is weakened, derived from the fact that the terms of exchange tend to deteriorate.

How then, to engender structural change to achieve a high growth rate compatible with external insertion? In Thirlwall's terms, it would be necessary to change the makeup of both the exports and imports, so as to increase the growth rate of the former and reduce the income elasticity of the latter. In this regard, structuralism has long had a tradition, under the concept of Import Substitution Industrialization, of reducing the income elasticity of imports (Prebisch, 1986), while contemporary authors have rather opted for export diversification (Hausmann and Rodrik, 2003 2

Structural change policies oriented towards sustainable growth cannot be circumscribed to short-term objectives. The mere removal of trade barriers in economies with an abundance of natural resources can destroy sectors that are more integrated in the economic structure and reduce aggregate productivity (McMillan and Rodrik, 2011). As a counterpart to this, merely implementing quantitative restrictions on imports may be an effective short-term policy, but it fails to alter the structural foundation underlying the external growth restrictions.

There are those who would propose, then, the implementation of long-term policies to prevent the allocation of capital from being determined merely by the "correct prices" vector of the free market; favoring the securitization and accumulation of capital towards sectors considered to be "strategic" (Wade, 1989), whose export insertion would transform the pattern of specialization and generate dynamic competitive advantages (French-Davis, 1991). However, this would require an institutional framework that would guarantee that the granting of incentives would bring about benefits in terms of investments, technical change, and exports for the sectors and companies involved (Change, 1993); in other words, a way to prevent rent-seeking behavior.

III. CHANGES IN THE CURRENT ACCOUNT AND THE ROLE OF INDUSTRIAL MANUFACTURES IN THE EXTERNAL SITUATION

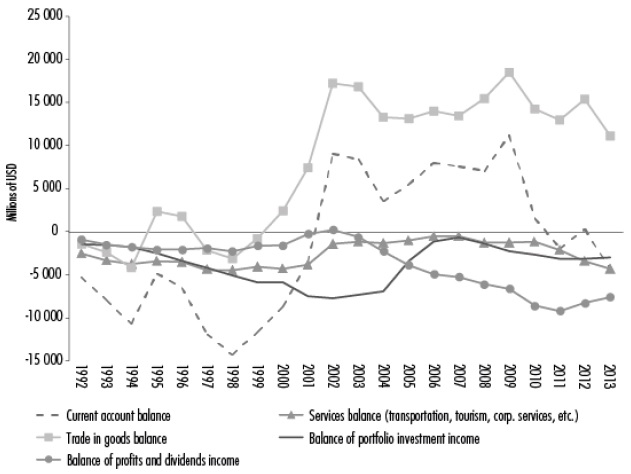

The changes seen in Argentina's current accounts in the post-convertibility era (as compared to the 1990s) are a sign of structural economic change (see Figure 1). The tremendous current account deficit in the 1990s (explained by a sustained negative balance in all of its components, except the balance of trade in goods for 1995-1996), gave way to a significant surplus in 2001-2009 and a subsequently much less pronounced deficit. This relative equilibrium can be explained in large part by the balance of trade in goods, which became strongly positive. However, after the import volume plummeted in 1998-2002, the subsequently marked growth in income generated an import volume that grew to a rate far above that of exports (see Figure A.1 of the Appendix). The improved terms of trade partially closed the gap and propped up much of the trade surplus produced since the end of the crisis. But by 2012, this situation was accompanied by lower growth rates and the implementation of import controls.

Services (transportation, tourism, corporate services, etc.) displayed negative structural behavior, which has escalated in recent years. The component of income balance, also structurally negative, has followed a diverging path in the recent decade: the negative balance of portfolio investment income was reduced (as external debt came down), while the deficit in profits and dividends rose sharply. This can be explained by the massive inflow of FDI into Argentina over the past two decades, which contributed to the foreignization of the economy (Manzanelli and Schorr, 2011). In this way, despite the genuine contribution of foreign currency and the potential exports that were carried out, the strong dependency on capital goods and imported inputs (due to a dearth of linkages with the local productive networks) and the increase in the remission of profits and dividends so characteristic of foreign capital, have led to uncertain outcomes for FDI processes.

Source: Created by the authors based on data from INDEC.

Figure 1 Evolution of the Current Account Balance and Its Components, 1992-2013 (In millions of dollars)

It is also important to remark that the change of macroeconomic regime in early 2000 made the Argentine economy much more open. In 1996-1998, foreign trade in goods and services (adding import and export flows together) accounted for 18.8% of the gross domestic product (GDP), while this percentage rose to 31% by 2011-2013.3 This entrenched the relationship between foreign trade and activity level, especially through the trade in goods balance.

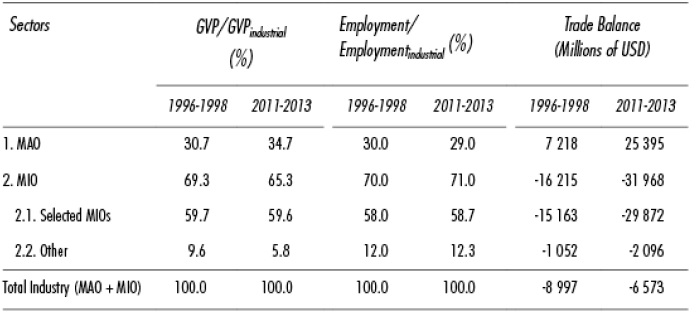

Likewise, it would be useful to clarify that this relationship is a symptom of the productive imbalances present in the industry, which have only deepened since the 1990s. As can be seen in Table 1, manufactures of industrial origin (MIO) generate the majority of the gross value of production (GVP) and industrial jobs, but their trade balance also displays a marked deficit, the majority of which is compensated for by the positive trade performance of manufactures of agricultural/livestock origin (MAO). To this imbalanced structure, which has remained largely unchanged from one decade to the next, we add the fact that the share of MIOs in the GVP is falling. As such, the strong competitiveness of MAOs and a set of MIOs with a major deficit are a sign that local productive networks are significantly dependent on imported capital goods and inputs, as a result of this dual industrial structure (Bekerman and Dulcich, 2013).

Table 1 Composition in Terms of Major Sectors for Employment, Production, and the Trade Balance of the Industrial Sector. Averages 1996-1998 and 2011-2013*

*Note: The line "Selected MIOs" shows all of the data sectors chosen to analyze the subsequent to the study.

Source: Created by the authors based on CEP data.

Finally, despite the fact that macroeconomic policies in the post-convertibility era have differed substantially from the policies implemented in other Latin American countries,4 the industrial policy in Argentina is rather weak (poorly defined and relatively unambitious objectives, certain lack of consistency between objectives and instruments), and the market challenges facing South America in light of China's emergence (in its dual role as a powerful purchaser of commodities exported from underdeveloped countries and a strong competitor for a wide range of industrial products) have prompted the gradual primarization of the productive structure (in which the MAO-MIO fissure is especially important), a situation that is similar to that of other countries in the region (Bekerman et al., 2014).

IV. GROWTH AND EXTERNAL RESTRICTIONS DURING 2003-2013

To identify ways in which the international pattern of specialization was transformed over the past decade and assess the degree of sustainability in light of various growth rates, we must first analyze the country's overall and sectoral export and import track records. To do so, we conduct an analysis drawing on Thirlwall's Law to compare two time periods: 1992-1999 and 2003-2013.

IV.1 General Analysis of Thirlwall's Law

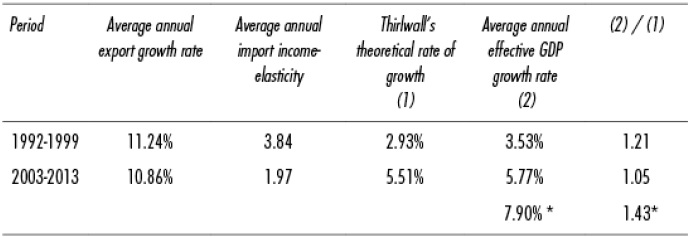

Thirlwall (1979) asserts that if a country incurs a trade deficit as demand is growing (with an abstraction of the other components of the current account), in the medium term, it should restrict its growth processes due to the need for foreign currency to address the deficit, which posits the existence of a theoretical growth rate that expresses the external restriction on growth. In this section, we will look at how Thirlwall's theoretical rate of growth (TRG) in the post-convertibility period evolved with respect to the 1990s, as compared to the effective growth rate (see Table 2).5 To do so, we will examine the time periods 1992-1999 and 2003-2013 (excluding the recession and crisis between the two periods).

Table 2 Comparison Between TRG and the Effective Growth Rate of the Argentine GDP. 1992-1999 and 2003-2013

Note: Values with (*) represent results excluding analysis of the years 2008-2009.

Source: Created by the authors based on IMF and COMTRADE data.

The results shown here display a significant drop in the income elasticity of imports, which proportionately exceeds the decrease in the export growth rate (due to lower export growth, because the terms of exchange were very favorable). This prompts an increase in the TRG during 2003-2013 (with respect to the convertibility era), indicating the potential relaxation of external restrictions. However, the effective growth rate of the GDP during the time period appears as higher than the TRG, which shows that Argentina grew at a rate higher than what would permit the maintenance of a stable balance of payments. It can be demonstrated, moreover, that the situation becomes even more concerning if the years 2008 and 2009 are excluded from the analysis (as these were years in which growth and imports fell sharply due to an external factor, the international crisis), when the effective average annual growth rate of the period was 7.9%, which is 43% higher than the TRG (see Figure A.1).

This situation, along with the negative dynamics observed in other areas of the current account that were analyzed earlier (such as income derived from profits and dividends), helps to explain the downward trend of the current account surplus, as well as the recent implementation of foreign exchange and trade restrictions. In this context, the economic slowdown of recent years is a sign of the imposition of external restrictions, despite the fact that the income elasticity of imports was indeed lowered.

IV.2. Behavior of Thirlwall's Law in MIO Sectors

Although Thirlwall's Law tends to be applied at an overall level, it can also be useful at the sectoral level (Araujo and Lima, 2007; among others). In particular, we will apply it to various industrial sectors to analyze the changes between the time periods considered, both in terms of the export behavior as well as capacity to compete against imported goods.6 This will allow us to determine which sectors are facing the greatest challenges in international insertion.

To do so, 23 MIO sectors were selected based on their importance for imports, exports, and jobs in the overall industry in the time periods considered. These sectors are listed in Table A.1 in the Appendix.

The evolution of these sectors with respect to the two variables considered by Thirlwall between the time periods 1992-1999 and 2003-2013 is found in Figure 2.

More than half of the 23 sectors chosen are located in quadrants 2 and 3, revealing an increase in the income elasticity of imports, which contrasts with the overall decrease of this elasticity. However, many of the sectors are close to the axes, which is a sign of scarce structural change.

Now, there were two sub-sets of the sectors that displayed a tendency towards increasing income elasticity of imports. On the one hand, there were eight sectors whose export rate rose between the two decades, despite the fact that imports also went up (see quadrant 2 of Figure 2): metal surface finishing (289); general-purpose machinery (291) and special-purpose machinery (292); electrical items (31x); textiles and footwear (17x-18x-192); car parts (343); non-ferrous metals (272); and precision instruments. On the other hand, five sectors saw the export rate fall and an increase in import income elasticity (see quadrant 4): fuels and lubricants (232); video and sound players (32x); household appliances (293); iron and steel products (271); and the automotive industry (341).

Note: Due to its negative variation in exports (-35.1%), "Wood and wood products" (20x) could not be displayed on the figure, but it is in quadrant 3. Analogously, the positive variation (28.6%) of "Office and computer machinery" (300) places it in quadrant 1. Source: Created by the authors based on CEP data.

Figure 2 Changes in the Trade Performance of Selected MIO Sectors Between 1992-1999 and 2003-2013

The remaining 10 sectors are located in quadrants 1 and 3, which means that they contributed to the import substitution process. Among others, the sectors in quadrant 1 saw export rates grow simultaneously: office and computing machinery (300); chemical products (242); leather goods (191); non-metal mineral products (269); and trains and aircraft (352-353). By contrast, quadrant 3 contains those where the export growth rate fell: basic chemical substances (241x); pesticides (2412); rubber and plastic products (25x); paper products (2010); and wood (20x), with the particularity that the latter is the only sector of the subset where exports shrunk in absolute terms.

On the other hand, it is interesting to compare the changes observed in each of these sectors with their capacity to supply the domestic market and create jobs, through an analysis of the connection between external sustainability and industrial structure. Figure 3 relates the outcome of the theoretical Thirlwall rate for each of the sectors (TRGi) for 2003-2013, with the level of import penetration.7 In turn, the relative share of each sector in total employment contributed in 2011-2013 for the set of selected sectors is represented by the size of each bubble.

Looking at the trade dynamics of the sectors, we can define two regions in Figure 3 separated by overall TRG, that impacted foreign restrictions on overall trade in 2003-2013. To the left of the overall TRG (5.51% annual average) are the sectors whose dynamics make them "not sustainable in Thirlwall's terms," and which display rates below the TRG. As such, their trade balance shows a trend towards deterioration, even if Argentina grows at a rate that would not harm its overall trade balance. By contrast, to the right of the TRG, we find the sectors whose evolution makes them "sustainable in Thirlwall's terms," given that their TRGi is greater than the TRG.

The horizontal slice of the figure, which indicates the average level of import penetration of the MIO sectors for the time period 2011-2013 (44.1%), will be taken as a reference to assess the degree of import penetration present in the various sectors.

Figure 3 reveals that the greatest external restriction on growth in the Argentine industrial structure is found in the behavior of the MIOs, given that during 2003-2013, only four of the 23 sectors analyzed displayed a sectoral TRGi higher than that of the overall TRG (showing dynamics that are "sustainable in Thirlwell's terms"). The 19 remaining sectors present deteriorating trade balances, even in situations of overall growth not restricted by the external sector. As the foundation for this situation, the surplus generated by primary products (PP), the MAOs, and the few sustainable MIO branches permitted Argentina to grow "at Chinese rates" for a few years; at the same time, the trade deficit of MIOs gradually rose (Bekerman and Dulcich, 2013). Finally, and in conjunction with the aforementioned deterioration of the other components of the current account, the imposition of external restrictions has led to an economic slowdown and the implementation of restrictions on imports.

The evolution of trade performance in the selected sectors can be observed by relating Figures 2 and 3. The few sectors in quadrant 1 of Figure 2, and their location close to the axes, demonstrates that there would not be, in response to a change of macroeconomic regime, a tendential movement to make their sectoral external insertion compatible with the highest GDP growth rates (through the dual path of the decrease in income elasticity of imports and the rise in the export growth rate); so the trend of the MIO sectors did not translate into the mollification of external restrictions in the post-convertibility era. Moreover, there are two sectors with high import penetration levels (computing machinery: 300; and trains and aircraft: 352-353).

Finally, it is worthwhile to point out that the biggest generators of jobs were the sectors that show, initially, an inverse and significant relationship with respect to the degree of import penetration, as we can observe in Figure 3. In effect, sectors with lower import penetration generated the majority of industrial jobs (approximately 43%), in contrast with those that had high degrees of penetration (16%). On the other hand, higher job levels were found, with the exception of chemical products, in the "non-sustainable in Thirlwall's terms" swath of sectors.

Note: The size of the bubbles represents the share of employment from the sector with respect to total employment among the selected sectors. Sectors 191 (leather and saddlery products) and 272 (non-ferrous metals) were outside of the area of the graph, as they had extremely high TRG values.

Source: Created by the authors based on CEP, MTEYSS, and COMTRADE data.

Figure 3 Trade Sustainability, Import Penetration, and Employment Intensity in Selected Sectors, 2003-2013

IV.2.1. Sectors with "Non-Sustainable in Thirlwall's Terms" External Insertion and High Import Penetration

This subset of sectors showed little effect on employment together with high levels of domestic demand (significant trade deficits), so they offer a high potential to implement an import substitution policy. These are innovative sectors worldwide (computing machinery: 300; video and sound players: 32x; medical and precision instruments: 33x; trains and aircraft: 352-353; general-purpose machinery: 291; and special-purpose machinery: 292); complemented by engines and batteries (31x); car parts (343); and basic chemical substances (241).

Although the lack of trade sustainability persists, these sectors did not have the same trade performance as they did in the 1990s. As shown in Figure 2, computing machinery (300) experienced quite favorable dynamics, while video and sound playing devices (32x) worsened notably.

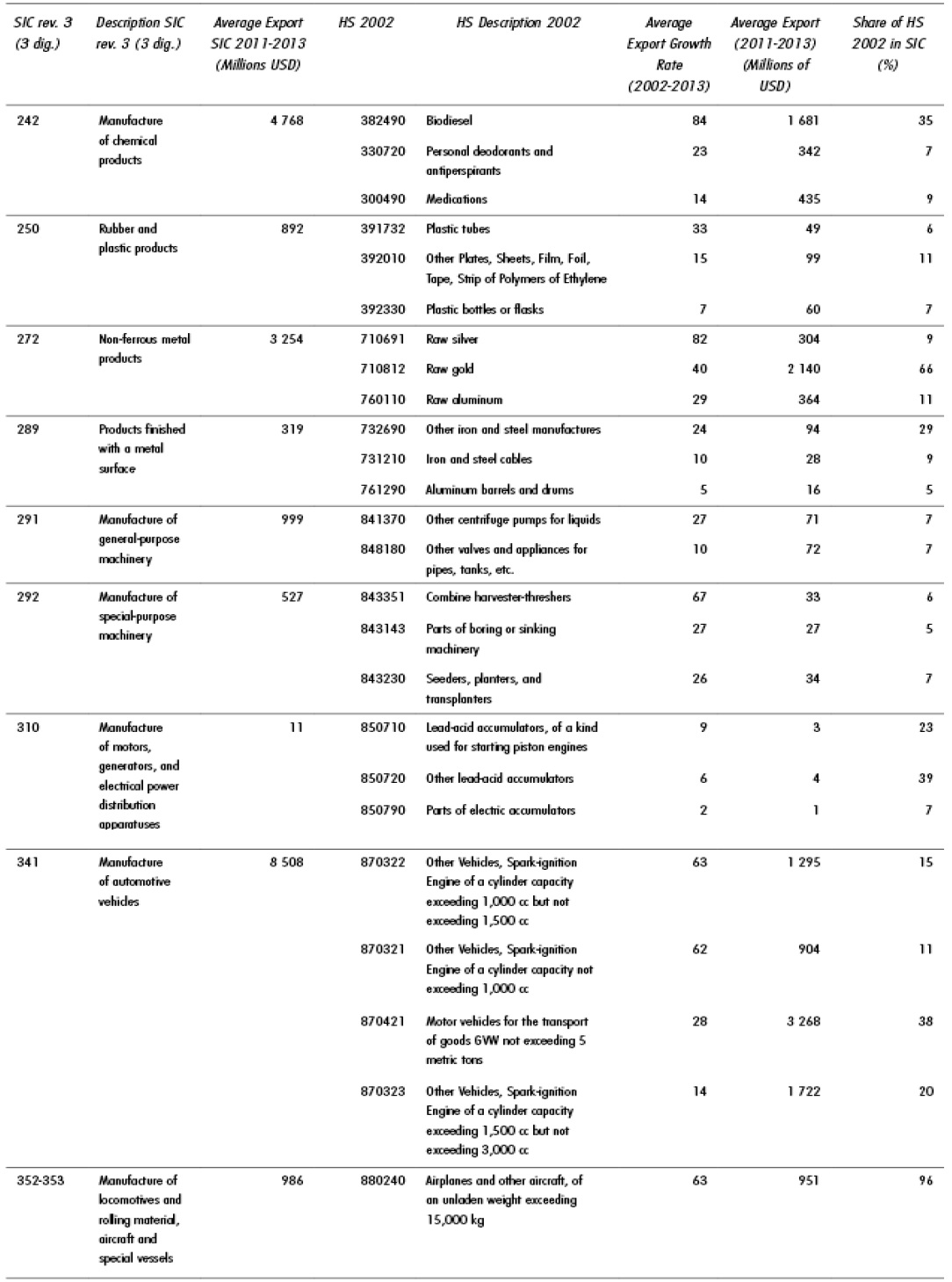

Meanwhile, general-purpose machinery (291) experienced high import penetration and ended the decade with one of the worst trade deficits among the sectors selected (see Table A.1 of the Appendix), persisting with a trend of a lack of trade sustainability. The growth of the export dynamics can be explained by centrifugal pumps for liquids (see Table A.2 of the Appendix), within which there are likewise some specific items that meet the function of car parts. Similar was the situation of special-purpose machinery, whose growing export dynamic, based on the subsector of agricultural machinery (see Table A.2), was not enough to be in the zone of sustainability due to high import penetration. Complementing this analysis of the general- (291) and special-purpose machinery (292), we can see that both experienced import dynamics that can be explained by the significant technology dependence of Argentina, which drives the import growth of machinery and inputs needed to carry out the investment processes in a context of economic growth. This dependency was solidified during the 1990s, in a framework of economic liberalization with the real revalued exchange rate, and was not reversed in the 2000s; although the origin of these imports has shifted to China, to the detriment of the United States and the European Union (Bekerman et al., 2014).

Looking at car parts (343), with a strong impact on industrial employment, this sector opened up to foreign trade as compared to the 1990s: car parts grew both in terms of the export rate and the income elasticity of imports. This productive reconfiguration carried out by multinationals in the sector at the regional level (Bekerman and Dulcich, 2014) entailed an increase in car parts imports, but was also accompanied by an export jump in final vehicles (341), especially in lower-cylinder model cars (see section Sectors with "Sustainable in Thirlwall's Terms" External Insertion).

In the case of engines and batteries (31x), these products display a relatively low impact on exports and jobs, but a strong trade deficit and high import penetration. However, they experienced some growth in the export rate (tied to automobile batteries, where once again we see the effect of the automobile chain in the Argentine industrial complex).

Finally, the good performance of trains and aircraft (352-352), which brings this sector close to the overall TRG, was due mainly to the strong export jump in large-size aircraft (see Table A.2) with no significant changes in terms of imports.

IV.2.2 Sectors with Dynamics that are "Not Sustainable in Thirlwall's Terms" and Low Import Penetration

These sectors also display issues with sustainability with regard to the TRG, but, unlike the others, show low import penetration. This means that, in order to cross the threshold into sustainability, they would need to raise their export growth rates. Within this subset of sectors, of which nearly half show a domestic market orientation (because they are located in quadrant 3 of Figure 2), only three managed to raise the export growth rate with respect to the convertibility era, but failed to reach levels that would mean trade sustainability: textiles and footwear (17x-18x-192), non-metal mineral products (269), and metal surface finishings (289). The principal reason for this is, in the case of the textile and footwear sector, that the increase in exports was concentrated in raw materials and yarn to the detriment of fabric and confections (products with higher added value), in a sector that also suffered from an increase in the income elasticity of imports, according to estimates from the Pro-Tejer Foundation (2012).

The metal surface finishings (289) sector was unable to delve further into import substitution (stable income elasticity) in a context of domestic market growth and displayed a major trade deficit at the end of the period analyzed, despite having experienced export growth. This was concentrated in very specific subsectors (see Table A.2) within "Other iron and steel manufactures," whose exports grew 24% on average annually, and include such dissimilar products as boxes, ladders, bicycle frames, and containers for compressed or liquefied gas.

The wood and wood products (20x) sector experienced some of the highest export growth during the 1990s. However, in 2003-2013, it shifted mainly to supplying the domestic market, with a clear drop in the income elasticity of imports and stagnated exports.

The same was true of fuels (232) in the export realm, but in this case combined with an alarming increase in the income elasticity of imports, which led imports to reach 9.397 billion dollars in 2011, a year in which the energy balance deficit was nearly 3 billion dollars (Barrera, 2012).

Finally, in the iron and steel products (271) sector, despite its good external insertion of seamless pipes for oil extraction, experienced a slight slowdown in export growth.

IV.2.3. Sectors with External Insertion that was "Sustainable in Thirlwall's Terms"

For automobile factories (341), the change of macroeconomic regime prompted a slight increase in the income elasticity of imports, as well as relatively lower export growth (in a sector that experienced strong growth and opening up abroad in the 1990s, due to the beginning of a special trade regime with Brazil). However, the sector continued to have a TRGi value above the overall TRG, due to the fact that the export growth rate in this decade was also very high (31.3% during 2003-2013). As has already been mentioned, these transformations can be explained by the change in strategy of the multinationals coordinating the value chain, in light of the new bilateral regime between Argentina and Brazil.8 The new strategy (which permitted them to exploit the preferential bilateral tariffs) consisted of finishing lower-cylinder models in Argentina to provide to the local and also partially to the regional market, which justified the export jump in these models (see Table A.2); while big cars continued to be provided mainly from Brazil.9

The chemical products sector (242) displayed a slight drop in the income elasticity of imports and a major increase in the export rate. The formidable performance of biodiesel (obtained from soy oil, whose production for exportation began in the mid-2000s) explains the high value of the TRG. The biodiesel export boom was also due to the sliding scale of retentions scheme in the value chain, which generated an effectively high rate of protection (in reality, an income transfer toward the primary links of the transformation of the product), complemented by favorable conditions in the foreign market (Bekerman and Dulcich, 2013), which are currently on hold due to changes made to the European biodiesel import policy. Biodiesel currently accounts for 35% of the exported value of the chemical products sector (see Table A.2), followed by products with strong export insertion, such as deodorant and medication.

On the other hand, looking at non-ferrous metal products (272), more than 85% of the exports consisted of raw metals (gold, silver, and aluminum), erroneously classified as MIO, which show strong export growth due to rising international prices and the growth of the local mining sector. Its formidable trade dynamics are in part obscured by the low generation of employment and linkages with the Argentine industrial complex.

Finally, leather goods (191) are products that have long been exported from Argentina and have historically displayed trade surpluses (see Table A.1). With the change of the macroeconomic regime, import substitution has escalated, with a decrease in income elasticity.

V. CONCLUSIONS

In the post-convertibility era, the Argentine productive structure has opened up markedly, deepening the relationship between the behavior of foreign trade and activity level. In that context, the trade balance was the most dynamic aspect of the current account, and managed to solidify a positive balance that compensated for (and even exceeded) the structural deficit in the income balance. This behavior of the trade balance (the result of an export rate that was slightly lower than during the convertibility era, but with a strongly favorable trend in the terms of exchange, and a reduction in the income elasticity of imports) made it possible for Argentina to experience greater growth during the 2000s, based on the reduction of external restrictions.

However, Argentina grew slightly above the external restriction, gradually deteriorating the trade balance at the beginning of the decade, which, in combination with the deterioration of other components of the current account (especially the balance of profits and dividends), led to the imposition of foreign exchange and trade restrictions and an economic slowdown in recent years.

In spite of the high growth levels recorded during part of the post-convertibility era, the industrial sector did not undergo structural change, which generated growing trade deficits for the majority of MIO sectors. In that context, the surplus generated by PPs, MAOs, and the few sustainable MIOs permitted Argentina to grow at high rates for some years, but with the trade deficit of MIOS gradually on the rise, in light of dependence on the import of inputs and capital goods. This behavior of the industrial sector underpinned the external restrictions on trade and is a sign of the deteriorating trade balance of fuels during the 2000s, which has aggravated the structural problem, especially for MIOs.

This imbalance in the foreign trade performance of MAO and MIO sectors is inversely related to jobs. In effect, the MAO sectors, which displayed strongly positive trade balances, generated only 30% of industrial jobs, while the rest of the employment came from MIOs, which displayed a negative trade balance.

In this context, only a small set of MIO sectors (consisting of products with generally low added value) could achieve high "trade sustainability in Thirlwall's terms": chemical products (especially biodiesel), leather products, some raw metals, and automobile factories. The rest of the MIO sectors (19 of the 23 sectors analyzed in this paper, and those sectors that had the highest-technology industrial goods) displayed a clear trend towards a lack of trade sustainability and do not show signs of a positive change in the future. Only a few specific sub-branches displayed commendable export dynamics (such as agricultural machinery, non-metal minerals, and aircraft).

As such, the manufacturing performance in the post-convertibility era did not manage to reverse the Argentine industry's historical legacy of technology, which explains a good portion of the trade deficit of MIOs. Although a diversified productive system has been solidified in Argentina, it is facing challenges to achieve a sustainable growth trajectory.

Complementarily, the momentum of technology development is constantly redefining the most dynamic sectors worldwide. Global progress in biotechnology, nanotechnology, and communication and information technology is paving the way to add value to industrial commodities and foods that could help absorb qualified labor, create new dynamic companies, and potentially produce international suppliers of technology in specific niches. The growth of the agricultural machinery branch in Argentina, as well as other less-developed branches, but with strong potential (such as space technology and software production) are possible sectors whose progress derived from increased investment (in research and development, brand strengthening, etc.) could drive higher penetration for these products (and their associated technologies) in the global market. In that context, it will be necessary to complement macroeconomic policies focused on the aggregate demand with long-term policies that seek to modify the industrial structure, to prompt changes in international insertion that would solidify a process of high and sustainable growth.

REFERENCES

Arestis et al., 2008 Arestis, Philip, Luiz Fernando de Paula y Fernando Ferrari-Filho (2008), "Inflation targeting in Brazil", The Levy Economics Institute, Working Papers, núm. 544, Bard College. [ Links ]

Arza Valeria, 2011 Arza Valeria (2011), "El Mercosur como plataforma de exportación para la industria automotriz", Revista de la Cepal, núm. 103, abril, Santiago de Chile, pp. 139-164. [ Links ]

Azevedo Araujo et al., 2007 Azevedo Araujo, Ricardo y Gilberto Tadeu Lima (2007), "A Structural Economic Dynamics Approach to Balance-of-Payments-Constrained Growth", Cambridge Journal of Economics, vol. 31, Issue 5, Oxford University Press, pp. 755-774. [ Links ]

Barrera Mariano, 2012 Barrera Mariano (2012), "Subexploración y sobreexplotación: la lógica de acumulación del sector hidrocarburífero en Argentina", Revista Digital Apuntes para el Cambio, núm. 2, marzo-abril, Buenos Aires, pp. 19-35. [ Links ]

Bekerman et al., 2013 Bekerman, Marta y Federico Dulcich (2013), "La inserción internacional de la Argentina. ¿Hacia un proceso de diversificación exportadora?", Revista de la Cepal, núm. 110, agosto, Santiago de Chile, pp. 157-182. [ Links ]

Braun et al., 1968 Braun, Oscar y Leonard Joy (1968), "A Model of Economic Stagnation- A Case Study of the Argentine Economy", The Economic Journal, vol. 78, núm. 312, diciembre, Blackwell. [ Links ]

Cepal, 2008 Cepal (2008), "Las relaciones económicas y comerciales entre América Latina y Asia-Pacífico: el vínculo con China", Segunda Cumbre Empresarial China-América Latina, Harbin, China, octubre (consultado en marzo de 2012), disponible en <http://www.cepal.org/publicaciones/xml/3/34233/relaciones_economicas_america_latina_asia_pacifico.pdf >. [ Links ]

Chang Ha-Joon, 1993 Chang Ha-Joon (1993), "The Political Economy of Industrial Policy in Korea", Cambridge Journal of Economics, vol. 17, Issue 2, Oxford University Press, pp. 131-57. [ Links ]

Diamand Marcelo, 1972 Diamand Marcelo (1972), "La estructura productiva desequilibrada argentina y el tipo de cambio", Desarrollo Económico, vol. 12, núm. 45, IDES, Buenos Aires. [ Links ]

Ffrench Davis Ricardo, 1991 Ffrench Davis Ricardo (1991), "Ventajas comparativas dinámicas: un planteo neoestructuralista", Cuadernos de la Cepal, núm. 63, Santiago de Chile. [ Links ]

Frenkel, 2007 Frenkel, Roberto y Martín Rapetti (2007), Argentina's Monetary and Exchange Rate Policies after the Convertibility Regime Collapse, Center for Economic and Policy Research, Washington/Political Economic Research Institute/University of Massachusetts. [ Links ]

Fundación Pro-Tejer, 2012 Fundación Pro-Tejer (2012), "Boletín Económico Anual 2011" (consultado en octubre de 2013), disponible en <http://www.fundacionprotejer.com/boletines>. [ Links ]

Gómez Zaldivar et al., 2009 Gómez Zaldivar, Manuel, Oscar Manjarrez y Daniel Ventosa-Santaulària (2009), "Regresión espuria en especificaciones dinámicas", Ensayos, vol. 28, núm. 1, mayo, México. [ Links ]

Hausmann et al., 2003 Hausmann, Ricardo y Dani Rodrik (2003), "Economic Development as Self-Discovery", Journal of Development Economics, vol. 72, núm. 2, diciembre, Elsevier, Amsterdam. [ Links ]

Manzanelli et al., 2011 Manzanelli, Pablo y Martín Schorr (2011), "La extranjerización en la posconvertibilidad y su impacto sobre el poder económico local: un balance preliminar", Industrializar Argentina, núm. 14, mayo, Buenos Aires. [ Links ]

McMillan et al., 2011 McMillan, Margaret y Dani Rodrik (2011), "Globalization, Structural Change and Productivity Growth", Working Paper 17143, National Bureau of Economic Research, Cambridge. [ Links ]

Prebisch Raúl, 1973 Prebisch Raúl (1973), "Problemas teóricos y prácticos del crecimiento económico", Serie conmemorativa del XXV aniversario de la Cepal, Santiago de Chile, febrero. [ Links ]

Rodrik Dani, 2005 Rodrik Dani (2005), "Políticas de diversificación económica", Revista de la Cepal, núm. 87 (LC/G. 2287-P), diciembre, Santiago de Chile. [ Links ]

Thirlwall Anthony, 1979 Thirlwall Anthony (1979), "The Balance of Payments Constraint as an Explanation of International Growth Rate Differences", BNL Quarterly Review, vol. 32, núm. 128, pp. 45-53. [ Links ]

Wade Robert, 1989 Wade Robert (1989), "What can Economics Learn from East Asian Success?", Annals of the American Academy of Political and Social Science, vol. 505, The Pacific Region: Challenges to Policy and Theory, septiembre, pp. 68-79. [ Links ]

REFERENCES

Banco Mundial, 2014 Banco Mundial (2014), "World Development Indicators Database" (consultado el 25 de noviembre de 2014), disponible en <http://data.worldbank.org/data-catalog/world-development-indicators>. [ Links ]

Bekerman, Marta, 2014a Bekerman, Marta y Federico Dulcich (2014), "Dependencia comercial y patrones de especialización en un proceso de integración regional: el caso de Argentina y Brasil", Desarrollo Económico, núm. 211, vol. 53, IDES, Buenos Aires. [ Links ]

Bekerman, Marta, 2014b Bekerman, Marta, Federico Dulcich y Nicolás Moncaut (2014), "La emergencia de China y su impacto en las relaciones comerciales entre Argentina y Brasil", Problemas del Desarrollo, núm. 176, vol. 45, IIEC-UNAM, México. [ Links ]

Centro de Estudios para la Producción, 2014 Centro de Estudios para la Producción (CEP) (2014), "Fichas sectoriales 2013" (consultado el 10 de diciembre de 2014), disponible en <http://www.industria.gob.ar/cep/>. [ Links ]

Prebisch Raúl, 1986 Prebisch Raúl (1986), "El desarrollo económico de la América Latina y algunos de sus principales problemas", Desarrollo Económico, vol. 26, núm. 103, octubre-diciembre, IDES, Buenos Aires. [ Links ]

2 According to these authors, export diversification entails productive diversification that permits local agents to "discover" the unexplored comparative advantages of their economies, where pioneering exporters show the way to those who later take up the mantle (Hausmann and Rodrik, 2003). Countries that export more sophisticated goods experience a greater change than countries that do not (Rodrik, 2005). This allows them to raise the export growth rate and relax external restrictions.

4 In the entire region, interest rate control and currency appreciation prevailed, as the result of the implementation of inflation targeting regimes (ITR) (in Brazil, Mexico, etc.), which drive the inflow of speculative foreign capital (Arestis et al., 2008). However, Argentina did not adhere to this regime, and actually had in place a managed floating exchange rate system for many years, with more flexible growth targets and guidelines for monetary issuance (Frenkel and Rapetti, 2007).

5 The advantages of the Thirlwall approach for this analysis are manifold. Firstly, it permits the evaluation of the dynamic aspects of the relationship between international trade and the economic growth of a country more effectively than by comparing specific values of variables. Complementarily, and precisely due to its dynamic nature, it manages to clearly show the evolution of a structural problem, which is manifest in the indicators that make up the index (export growth and income elasticity of imports), especially when disaggregating these indicators by sector, like in this study. For more details about calculating the overall TRG and the estimation method, see the Methodological Appendix.

6 For the sectoral analysis, changes were made to the calculation of the TRG, with respect to its classic calculation method, which was used for the overall analysis. For more details about the methodology used, see the Methodological Appendix.

7 Import penetration was calculated as the average of the ratio between imports and apparent consumption in the sector for the period 2011-2013.

8 After the 28th Additional Protocol to the Economic Complementation Agreement Nº 14 signed between Argentina and Brazil in 1994, which permitted the significant liberalization of bilateral trade in the automotive chain (Arza, 2011); by 2000, the 31st Additional Protocol to this agreement had been signed, which standardized the common foreign tariff (with differences varying between auto parts, automobiles, trucks, etc.) and consolidated a tariff preference of 100% for bilateral trade, subject to a coefficient (called flex) that related bilateral imports and exports between Argentina and Brazil. This coefficient increased gradually until reaching 2.6 in 2005, and the expectation was that this restriction in bilateral trade would be liberalized by 2006. However, the 35th Additional Protocol to the agreement, signed in June 2006, reincorporated the flex condition for the regional tariff preference, but with a more restrictive coefficient of 1.95, which lasted (with negotiations in the interim) until mid-2013.

9 Two possible factors to support this argument can be found in Arza (2011). First, automotive bilateral trade is very sensitive to Argentine growth. The elasticity of bilateral exports from Argentina with respect to the country's growth is positive and higher than the unit, which demonstrates that the growth process reshapes some links of the chain at the regional level (especially factories), to supplant the domestic market in growth, but from that point forward, began to supplant part of the regional market. Complementarily, this process took place only in some models, with greater insertion in the Argentine market, and therefore on a smaller scale. By 2006, for example, Brazil was producing 43 models of light vehicles, and 15 of them on the scale higher than 35,000 units, considered efficient for the industry, while Argentina was only producing 17 models, and only two on this efficient scale. This difference is grounded not only in the fact that the two domestic markets operate on a different scale, but also because Brazil is a much more significant export platform to third-party markets than Argentina is. By 2005, Brazil was exporting automobiles to 135 destinations, while Argentina only did so to 64.

10 The subscripts i and t indicate that the variable in question applies to a certain sector and moment in time, respectively.

11 The following nomenclature was used: Mt= Total argentine imports for the period t (millions of current USD, FOB), Mit = Argentine imports for sector i in time period t (millions of USD, FOB), Yt = Argentine GDP for the period t (millions of USD, FOB), π = overall income elasticity of imports; πi = Income elasticity of imports for sector i; α and α i = constants. The sources used were INDEC and CEP.

12 The non-significant p-values were: fuels (1992-199) and household appliances (1992-1999). The significant p-values but with an R2 less than 0.7 were: pesticides, iron and steel products, special-purpose machinery, sound and video players, trains and aircraft (all for 1992-1999).

13 There is vast literature that addresses the issue of spurious regressions (see Gómez Zaldívar et al., 2009). Essentially, these regressions come about from the presence of a senseless statistical relationship, which results from estimating a regression using non-stationary series independent from one another.

METHODOLOGICAL APPENDIX

1. Presentation of the Adaptation of Thirlwall's Law Used in the Sectoral Analysis in this Paper

The conclusion of the original theoretical model developed by Thirlwall (1979) can be summarized in the following equation, which expresses the theoretical growth rate that determines the external restriction:

Where: TRG = theoretical GDP growth rate formulated by Thirlwall,  = export growth rate and π = elasticity - income of imports.

= export growth rate and π = elasticity - income of imports.

We get to this result assuming, one, the equilibrium of the trade balance (Xt = Mt, where Xt is the value of exports at time t and Mt is the value of imports at time t), two, the dynamic stability of this balance (  , where

, where  is the import growth rate), and three, that there are no significant variations in relative prices.

is the import growth rate), and three, that there are no significant variations in relative prices.

To apply this at the sectoral level, a version of the model was developed10 with a major change from the original. We begin with the dynamic equation for the trade balance, ignoring whether or not this balance is in static equilibrium:

Where:  and

and  represent the variations in the value of the trade balance, exports, and imports, respectively.

represent the variations in the value of the trade balance, exports, and imports, respectively.

In contrast with the classic Thirlwall analysis, which separated these into prices and quantities, we will analyze the flows in terms of value, without differentiating the effect of the terms of exchange, which are less significant at the sectoral level. We use the dynamic equation for the trade balance:

Once this equation is obtained, which relates the trade balance of the sector with the sectoral export and import growth rates, and with the relative level of the trade balance of the sector (X,it / M,it), we assume the stability of the trade balance (, =0) and redefine the sectoral import growth rates:

=0) and redefine the sectoral import growth rates:

Where:  is the growth rate of national income;

is the growth rate of national income;  and TTTi are the theoretical growth rate of the national GDP compatible with the stability of the trade balance for sector i (or Thirlwall's theoretical sectoral rate).

and TTTi are the theoretical growth rate of the national GDP compatible with the stability of the trade balance for sector i (or Thirlwall's theoretical sectoral rate).

As such, we reach Thirlwall's theoretical rate of growth, which, through the ratio Xi,t / M i,t, ends up being higher for the sectors that already displayed a surplus and lower for those that presented a deficit. In this regard, the choice was made to use for the values of Xi,t and Mi,t the averages of the period in question, which avoids the possibility of making evaluations tied to the specific context of a particular year.

The modified version reveals that in the analysis of the overall Thirlwall rate, the assumption of the trade equilibrium implies that the ratio of exports and imports in the sector would be equal to the unit (Xi,t =Mi,t) (and therefore Xi,t / M i,t = 1). In this way, the overall imbalances do not impact the growth restriction in the long term, driven by export growth and the income elasticity of imports. This could be due to economic forces that pressure the long-term equilibrium of the trade balance (in reality, the current account), through Hume's law and price adjustments (depending on the currency exchange regime), which tend to balance the supply and demand for foreign currency. However, in the sectoral case, there are no intrinsic forces in the trade balance: in fact, taking into account the criteria of the international division of labor and international specialization, it is not to be expected or desired that all of the sectors tend towards equilibrium.

2. Model Used for the Econometric Estimates of the Annual Income Elasticity of Imports in Argentina, Both Overall and at the Sectoral Level

Originally, the model to estimate was structured in the following manner:11

Global case (quarterly series):

Selected sectors (annual series):

For the conventional estimate of the Ordinary Least Squares, both at the overall and sectoral level, the variables were significant and displayed a high R2, except for a few cases where the p-value was above 0.05 and the R2 was less than 0.7.12 For the overall case, analyzed with quarterly series, the variables explained presented a significant self-regressing component on the order of 1, which was incorporated into the structure of the model. Likewise the variables (inter-annual growth rates) were stationary in levels pursuant to the Augmented Dickey-Fuller text for the periods under study, to avoid analyzing "spurious regressions."13 Although it would be relevant to analyze the cointegration of the variables for the sectoral case, so as to guarantee a statistically significant relationship in the long term between the variables considered, the annual data series used (because it was impossible to access public information regarding quarterly trade flows at the sectoral level) consist of very few data entries, which makes a hypothetical analysis of cointegration rather unfeasible.

STATISTICAL APPENDIX

Table A.1 Share in the Industrial GVP and Trade Balance of Selected MIO Sectors. Averages: 1996-1998 and 2011-2013

Source: Created by the authors based on CEP.

Table A.2 Breakdown of the Most Dynamic Exports into Selected Sectors for the Period 2003-2013

Source: Created by the authors based on COMTRADE.

Received: February 03, 2015; Accepted: April 29, 2015

This is an open-access article distributed under the terms of the Creative Commons Attribution License

This is an open-access article distributed under the terms of the Creative Commons Attribution License