nueva página del texto (beta)

nueva página del texto (beta) Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

Permalink1. Introduction

Financial liberalization and globalization -a process of withdrawing government regulations within the domestic financial market to better integrate it with the international financial market via the liberalization of balance of payment capital accounts- has integrated financial markets and capital flows at a global scale. This process has been intensified since the 1970s due to several factors: (i) the collapse of Bretton Woods; (ii) financial deregulation; (iii) the development of the euro-dollar market; (iv) technological processes, especially in the telecommunications and informatics sectors; (v) financial innovations (such as derivatives and securitization) accompanied by active balance sheet management of financial institutions; and (vi) liberalization of the balance of payments’ trade -and mainly capital account- that allows freer transactions among nations.

The seminal work on financial liberalization is by Viner (1947, p. 98), who posited: “[T]he basic argument for international investment of capital is that under normal conditions it results in the movement of capital from countries in which its marginal value productivity is low to countries in which its marginal value productivity is high.” Thus, financial liberalization was understood as the solution for developing countries with low savings and unstable rates of growth, for whom the consequences were low.

The conventional theoretical foundations of financial liberalization include McKinnon (1973), Shaw (1973)1, Balassa (1989), Fischer (1998), and Mishkin (2005), whose main argument is that financial liberalization creates an environment that facilitates economic growth. For instance, Feldstein (1999, p. 2) states, “the most obvious contribution of international capital flows to host countries is to augment the supply of domestic saving in countries with unusually rich investment opportunities.” Nevertheless, other economists criticize financial liberalization, and their criticisms -chiefly those affiliated with post-Keynesian theory - serve as the theoretical foundation of this article.

In a number of emerging economies, including Brazil, financial liberalization occurred at the beginning of the 1990s. In Brazil, it arrived as a result of economic policies and liberal reforms that sought to stabilize inflation and stimulate economic growth, dismissing the leading role that the state had previously held in the country’s development from 1930 to 1980. These neoliberal economic policies were synthesized by Williamson (1990) and became known as the Washington Consensus2.

The purpose of this article is to present, theoretically and empirically, how financial liberalization has been developed in Brazil since the 1990s. To do so, in addition to this introduction, the article has three further sections. Section 2 presents the main criticisms of financial liberalization. Section 3 describes Brazil’s financial liberalization in historical and empirical terms. Section 4 presents the final remarks.

2. Criticisms of financial liberalization

Critiques of financial liberalization have been advanced by different schools of economics, including some scholars affiliated with the mainstream New Keynesian economics, such as Rodrik (1998) and Stiglitz (2000). In heterodox economics, there are at least three main perspectives with extensive criticisms of financial liberalization. For instance, Fine (2010, 2013), Lapavitsas (2013), and Epstein (2005, 2019) offer summaries from a Marxist point of view. Influenced by both post-Keynesians and Marxists, but still developing an original perspective, the Regulationist school also criticizes financial liberalization. Syntheses of their ideas are to be found in Boyer (1999), Boyer and Saillard (2002), Aglietta and Berrebi (2007) and Becker et al. (2010).

Post-Keynesian theory is another perspective critical of financial liberalization. This school of thought has several criticisms, in various dimensions, of financial liberalization, as can be seen in Davidson (2002), Kregel (2004), Arestis (2006), Isenberg (2006), Grabel (2006), Palley (2007, 2009), Blecker (2009), Hein (2012), Paula, Fritz, and Prates (2017), and Kaltenbrunner and Paincera (2018), among others. The post-Keynesian criticism of financial liberalization furnishes the theoretical foundations of the present article.

When criticizing the theoretical hypotheses of financial liberalization3, at least three main points are essential to post-Keynesians. First, the interest rate does not emerge from the “loanable funds theory”. Interest rates are not a real sector phenomenon, they are set in financial markets, where banks and financial institutions are not simply intermediaries between savers and investors. Moreover, savings are not required for investing. As Keynes (2007, pp. 167-168) argues, the interest rate “is the ‘price’ which equilibrates the desire to hold wealth in the form of cash with the available quantity of cash”. Thus, “if this explanation is correct, the quantity of money is the other factor, which, in conjunction with liquidity-preference, determines the actual rate of interest”.

Following Keynes, financial markets set the interest rate depending on the liquidity preference of agents which, in turn, relies on the presence of uncertainty. According to Keynesian theory, when high uncertainty and negative expectations prevail, money is demanded as a store of value and is not spent in the form of investment. This is the essence of Keynes’s (2007) liquidity preference theory or interest rate theory.

Second, contrary to the loanable funds theory, Keynes and his followers explain that investment precedes savings, in that financial markets -especially the banking system- play a key role on credit creation. Keynes (2007, p. 183) says, “[s]aving and investment (…) are the twin results of the system’s determinants, namely, the propensity to consume, the schedule of the marginal efficiency of capital and the rate of interest”.

In a monetary theory of production, the finance-investment-savings-funding circuit prevails. This model is an alternative to the neoclassical model of investment financing. In Keynes’s model, when banks grant loans, they create liquidity, as Cardim de Carvalho (2015, p. 92) explains “investment, like consumption, relies on the possibility of paying for the desired goods, so an appropriate rendition of how investment comes into existence requires a proper understanding (including measurement) of how finance is created and allocated”.

The finance-investment-savings-funding circuit is as follows: (i) investment requires that the financial system creates liquidity; (ii) once an investment is made, it creates employment and income; (iii) unconsumed income generates savings that are carried to the financial system, where companies seek short-term debt to fund their investment plans; and (iv) ex-ante investment constitutes ex-post savings; therefore the relationship between savings and investment occurs through income, not through interest rates4.

Third, the canonical financial liberalization model is based on the ergodic axiom, which means that the expected value of an objective probability can always be estimated from observed data that provides reliable information about the conditional probability function governing future outcomes. By contrast, the post-Keynesian theory (Davidson, 2002) rejects the ergodic axiom as an explanation of prone-to-equilibrium financial market behavior.

In an uncertain world, “even ‘fundamentals’ exist today and even if a data set permits one to estimate today’s (presumed to exist) objective conditional probability distribution, such calculations do not form a reliable base for forecasting the future” (Davidson, 2002, p. 187). Thus, it is because of Keynes’s concept of uncertainty that future market valuations are neither predictable nor calculable by probability, implying non-ergodicity; thus, financial markets cannot be presumed to be perfectly efficient.

Furthermore, there are five additional theoretical and empirical arguments to criticize financial liberalization:

i) It is difficult to establish a robust relationship between financial liberalization and economic growth for developed and, and even less evidence has been shown for emerging economies (Eichengreen and Leblang, 2002; Rodrik, 1998). In an empirical work analyzing economic reforms in Latin America and the Caribbean, Stallings and Peres (2000) found that financial liberalization often had negative effects, and that the data correlation level of openness to economic growth is decidedly inconclusive.

ii) Capital flows can be disruptive in emerging markets and may reduce the autonomy of such markets’ macroeconomic policies. They can also create volatility in emerging countries’ exchange rate, as Eichengreen, Tobin, and Wyplosz (1995, p. 164) explain “volatility in exchange rates and interest rates induced by speculation and capital flows could have real economic consequences devastating for particular sectors and whole economies”. Hausmann, Pritchett, and Rodrik (2004) insist that preserving the autonomy of fiscal and monetary policies to focus on assuring growth and development, and on avoiding speculative attacks, requires capital controls and an exchange rate regime that avoids excessive exchange rate fluctuations and minimizes external vulnerability. Palley (2009, p. 16) argues that “countries that have grown fastest (China, the East Asian tigers, Chile, India) have all used [capital] controls”.

iii) According to Demir (2007), financial liberalization stimulates investments in financial assets instead of productive assets -i.e., financialization. International investors favor short-term portfolio investments to the detriment of long-term capital stock. This point is emphasized by Hein (2012), who argues that financialization has, in fact, been used to refer to finance-dominated accumulation regimes.

iv) Financial liberalization increases the need for international exchange reserves, because of the huge, rapid inflows and outflows that accompany deregulated capital accounts. Kregel (2004, p. 8) presents an example of international financial fragility to show the importance of “the provision of temporary liquidity” in avoiding an outcome in which “countries that are hit by external shocks transform their financing profiles from ‘hedge’ to ‘speculative’ (…) [or] into Ponzi financing.”

v) Stiglitz (2000) also criticizes the argument that international financial integration can generate greater macroeconomic stability because risk diversification and market discipline would stimulate the adoption of sound macroeconomic policies. He argues that capital flows are pro-cyclical and, thus, do not soften the economic cycle but rather exacerbate cycles of booms and busts.

To conclude, two final considerations may be drawn. First, there is no empirical evidence that financial liberalization and large capital mobility produce sustainable growth. On the contrary, more regulated economies, such as China, grew more robustly than deregulated countries, such as Brazil.

Second, following Epstein (2002, p. 3), who asserts that “‘[f]inancialization’ refers to the increasing importance of financial markets, financial motives, financial institutions, and financial elites in the operations of the economy and its governing institutions, both at the national and international levels”, a question arises: How did financialization occur in Brazil?

The next section answers this question. It describes the process of financial liberalization of the Brazilian economy and also shows data attesting to the volatility in selected financial markets that accompanied the deregulation of Brazil’s external capital accounts in the 1990s.

3. Financial liberalization in Brazil

Economic deregulation in Brazil had begun by the end of the 1980s. The economic opening of the country was part of this liberalization process and was initiated with the trade liberalization of the late 1980s. In turn, financial liberalization, Freitas and Prates (2001) argue, began in 1991, when the first step was taken toward the financial opening of Brazil. Foreign investors were allowed entry into the Brazilian stock market -in both its primary and secondary stances. In that same year, external allocations in domestic investment funds were also permitted -although at first only to funds dedicated to investing in privatizations, which were then starting to occur in Brazil. In 1993, foreign investors were granted permission to invest in fixed-income assets. On the other hand, Brazilian financial institutions were granted the authority to issue debt abroad in 1991. These changes marked the beginning of financial liberalization in Brazil.

Notwithstanding having started in the beginning of the 1990s, the process of Brazil’s trade and financial liberalization occurred in earnest with the 1994 Real Plan. The Plan was an economic program that aimed to eliminate the hyperinflation afflicting Brazil. The economic stabilization strategy had three steps: First, the government adjusted its fiscal deficit; second, the Central Bank of Brazil (henceforth, CBB) introduced a price index to stabilize relative prices; finally, a monetary reform was implemented -the real was introduced as legal tender. It was a managed exchange rate, pegged to the US dollar in an underappreciated exchange rate that kept the US dollar cheap in Brazilian real terms. The Real Plan was successful in its main objective, reducing and controlling the country’s inflation rate5.

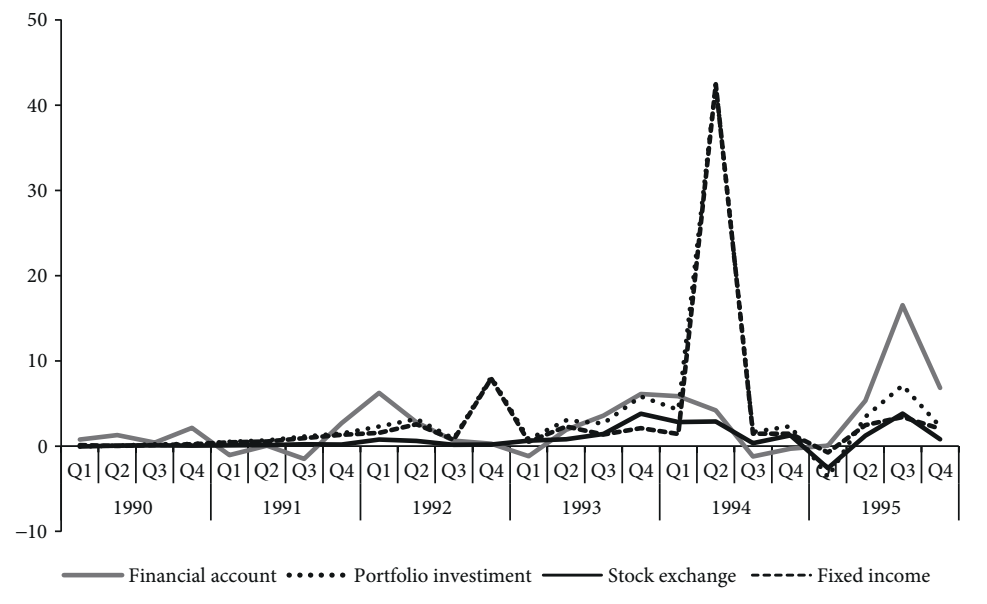

Graph 1 shows the data of Brazil’s balance of payments financial account from 1990 to 1995. The focus is on reporting the data of the first years of financial liberalization in Brazil. The only data available for this period is that of the Balance of Payment Manual 5. Nevertheless, the graph shows the beginning of the financial international inflows to Brazil in 1991, but chiefly from 1993 onwards.

Source: Authors’ elaboration based on CBB (2021).

Graph 1 Brazil’s balance of payments financial account: Total, portfolio account, stock and fixed-income investments, 1990 to 1995 (Quarterly, USD billion)

The graph also presents two interesting aspects of the financial flows before the 1994 Real Plan. On the one hand, these flows were predominantly fixed income. After such flows were allowed entry into Brazil, a positive response of capital influx can be observed. On the other hand, in the second quarter of 1994 -that is, the very moment when the Real Plan was launching the real as the new currency of Brazil (July 1, 1994)- there was a massive influx to Brazilian fixed-income assets, which accounted for almost the total outcome of the Brazilian financial account. Foreign capital was coming to Brazil to enjoy the sky-high real interest rates in the country just after inflation had subsided, in July-August 1994. Data from CBB (2020a) shows that the nominal Selic rate was 4.17% per month in July 1994, whereas the official consumer price index (IPCA), was 1.86%. In September 1994, the IPCA was 1.53%, whereas the nominal Selic rate was 3.83% per month. Brazil was paying a high yield and the external financial capital took advantage of that.

Economic deregulation played a key part in the overall “mindset” of the Real Plan. In particular, there were two ideas driving external liberalization. First, in terms of trade liberalization, a strong Brazilian real and lower import taxes were the strategy to force external competition upon Brazilian producers, who were perceived as underexposed to external competition, thanks to the commercial protectionism granted to them during Brazil’s 1930-1980 industrialization process. The policy makers of the Real Plan understood that Brazil had a costly and low-productivity manufacturing industry. Thus, trade opening with a weak US dollar in terms of the real was meant to stimulate imports of goods and services in a kind of external commercial shock.

Second, financial opening was needed for two reasons. To administer the managed exchange rate adopted from 1994 to 1999 external savings were required. Giving up capital controls would facilitate the entrance of foreign capital into Brazil and the accumulation of the international reserves needed to administer the exchange rate. Moreover, another idea behind the Real Plan was typically neoclassical. Although Brazil was already one of the ten wealthiest countries in the world in the 1990s, it had a scant capital stock. Thus, for Franco (1998), one of the leading proponents of the Plan, to avail itself of the opportunity presented by financial liquidity, Brazil would need free capital flows.

The outcome of the lowered import taxes and the appreciated real was, of course, a huge trade balance deficit. However, Brazil could not spare the accumulation of international reserves. Moreover, during 1995-1998 external liquidity was reduced among emerging countries due to the crises affecting Mexico (1995), the Asian Tigers (1997), and Russia (1998). The contagion effect of these crises also struck Brazil, another emerging country like those that suffered speculative attacks. Because it was practicing a managed exchange rate, the only possible response that Brazil could give to these crises was to heighten the CBB base rate, Selic. As such, the average Selic rate from July 1994 to January 1999 was equal to 34.1% per year (Ipeadata, 2020).

Brazil’s entrance into financial globalization was strongly dependent on attracting external capital to sustain the framework of the Real Plan; this was the negative side effect of stabilization. With the reductions of capital flux over 1994-1999, Brazil received external direct investment only in 1996 and early 1997, and that was due to the privatization process taking place as a component of the Real Plan. Apart from this short period, short-term financial capital -typical hot money capital- was entering Brazil.

The price stabilization process relied on the managed exchange rate; thus, the fear of inflation arising from the depreciation of the real necessitated a continuation of the pegged exchange rate until January 1999. After the flexibilization of the exchange rate, an inflation-targeting regime was implemented in July 1999, and the openness of the Brazilian economy remained unchanged. Throughout 1999-2020, capital controls were implemented in Brazil only in 2012, and were withdrawn shortly thereafter in accordance with the international liquidity cycles.

Brazil bears a deregulated capital account, but its price level is strongly subject to the exchange rate. Modenesi and Araújo (2012) estimate that the exchange rate explains one third of the price level in Brazil. Thus, not only does Calvo and Reinhart’s (2000) fear of floating matter to Brazil’s economic policy, but the exchange rate level is also very important, because both directly affect the country’s price level. However, within a deregulated capital account, the main avenues by which the CBB undertakes the exchange rate policy are (i) the use of exchange rate swaps, (ii) international reserves, and (iii) managing the Selic rate.

Following the introduction of the flexible exchange rate in 1999, the Selic rate began falling. Still, a high rate prevailed, namely an average of 14.3% per year from July 1999 to December 2014 (CBB, 2020a). The Brazilian base rate decreased from 2016 onwards only because of the strong recession that hit the country over 2014-2016. However, from January 2015 to July 2020, a period in which several countries went into negative nominal interest rates, the median Selic rate remained high, at 9.4% per year (CBB, 2020a).

This reflects the effort by Brazil to handle the impacts of a deregulated capital account within financial globalization. The country launched a broad financial opening and suffered severely from the external crises in the second half of the 1990s. After that, Brazil was hit twice in the early 2000s -first in 2001 with the Nasdaq collapse and the Argentinian economic crisis, and then again in 2002 with the Brazilian economic crisis, a speculative attack following the presidential elections. In the meantime, the great devaluation of the Brazilian real in 2002 passed through to domestic prices and Brazil registered the highest inflation rate since 1996 -12.53% (CBB, 2020a)- making clear the effect of the exchange rate on the Brazilian IPCA.

Following these setbacks, Brazil started accumulating international reserves to build a buffer against future exchange rate crises. The so-called “Great Moderation” period helped a great deal by increasing the country’s commodities exports. For the first time in history, Brazil had current account surpluses from 2003 to 2007. In this period, based on CBB (2020b), the country accumulated USD 42.0 billion in current account surpluses, whereas the international reserves grew by USD 142.0 billion, mainly in 2006, when they increased by USD 30.5 billion, and 2007, by more USD 87.4 billion. In 2006, the current account surplus was USD 13.0 billion, whereas in 2007 it was merely USD 408.0 million (Ipeadata, 2020). Thus, the international reserves were clearly and mostly mounted on inflows of external savings to the country.

However, the 2007-2008 subprime crisis was a “stress test” of the Brazilian economy: Between the last quarter of 2008 and the first quarter of 2009, the economy was sharply affected by the crisis; Gross Domestic Product (GDP) shrank by 4.5% (Instituto Brasileiro de Geografia e Estatística, IBGE, 2020). Despite the huge impact of the crisis on the Brazilian economy, the economic situation at that time was much better than that of other moments of external turbulence, such as the Brazilian exchange rate crisis in 1998-1999. This was mainly due to the improved macroeconomic fundamentals -that is, the reduction of fiscal and external imbalances6 that, as a consequence, diminished the country’s vulnerability to external shocks.

Moreover, the government responded quickly to the contagion effect of the systemic crisis with a broad variety of countercyclical economic measures, whose objective was to mitigate the effect of the crisis, both on Brazil’s financial system and on its economic activity. Thus, the CBB and the Ministry of Finance implemented stimulus packages that involved various measures related to fiscal, monetary, credit, finance, exchange rate, labor, and sectorial policies.

These measures produced their expected outcomes: In 2010 the Brazilian economy grew by 7.5%. Despite the countercyclical economic policies -particularly the fiscal and monetary ones- Brazil’s macroeconomic fundamentals were under control: The relationship between the net public debt and the GDP increased to only 43% and the international reserves reached nearly USD 239 billion in 2010. The favorable expectations among consumers, entrepreneurs and the financial system not only stimulated economic growth in 2010, but also attracted external capital, predominantly direct investment, and expanded the international reserves, which increased by USD 134 billion from 2009 to 2012 (Ipeadata, 2020).

It is also important to note that from 2009 to 2012, Brazil did not achieve a current account surplus. Once again, the accumulation of international reserves counted on external savings. Although they are a positive buffer to the country, being mostly external savings, they increase vulnerability to international liquidity cycles and to the humors of the hot money strategy. These financial humors change rapidly, as Graph 2 reports.

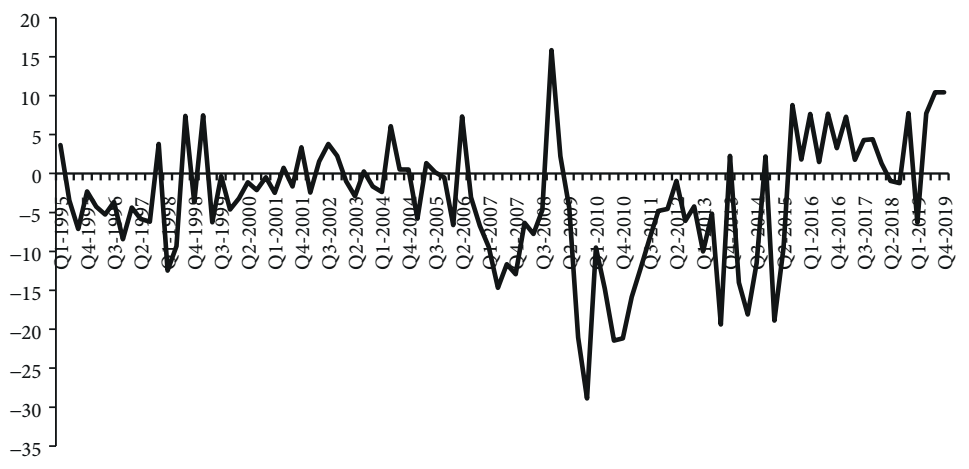

Source: Authors’ elaboration based on Organization for Economic Cooperation and Development (OECD, 2020).

Graph 2 Brazil’s net portfolio investment, 1995 to 2019 (Quarterly, USD billion)

Graph 2 shows that the net portfolio investment in Brazil was extremely volatile over 1995-2019. Such investments helped mounting international reserves, but at the end of the day they withdrew foreign resources from the country, nullifying their net contribution. If they were not responsible for building up Brazil’s international reserves, what was? The answer is direct investment coming into the country, as Graph 3 reports.

Source: Authors’ elaboration based on CBB (2020b).

Graph 3 Direct investment to Brazil, 1995 to 2019 (Annual, USD billion)

At first glance, the inflow of external savings as direct investment into the country would suggest a positive outcome, namely the increase of gross formation of fixed capital to improve Brazil’s rate of investment. However, Graph 4 shows that this was not the case. The quarterly annualized data of the investment rate in Brazil reports a decrease in fixed investments concomitantly with a growing entrance of direct investment into the country. As Graph 4 shows, if the incoming resource is not directed toward building capital stock, it is coming to Brazil merely to take advantage of the high Selic rate. This was Brazil’s financialized integration into financial globalization. Even the direct investment, ostensibly a boon to the enhancement of Brazil’s capital stock, arrived there in pursuit of financial gains.

Note: The IBGE (2020) dataset starts in 1996.

Source: Authors’ elaboration based on the IBGE (2020).

Graph 4 Brazil's gross formation of fixed investment/GDP ratio, 1996 to 2019 (Quarterly annualized data, %)

Moreover, the low entrance of direct investment in the Brazilian economy in the years after the Real Plan has contributed to the poor and unstable economic growth seen from 1995 to 2019. More specifically, based on Ipeadata (2020) data, the Brazilian economy has been characterized by a stop-and-go economic growth during the last 25 years, averaging an annual GDP growth of 2.3%.

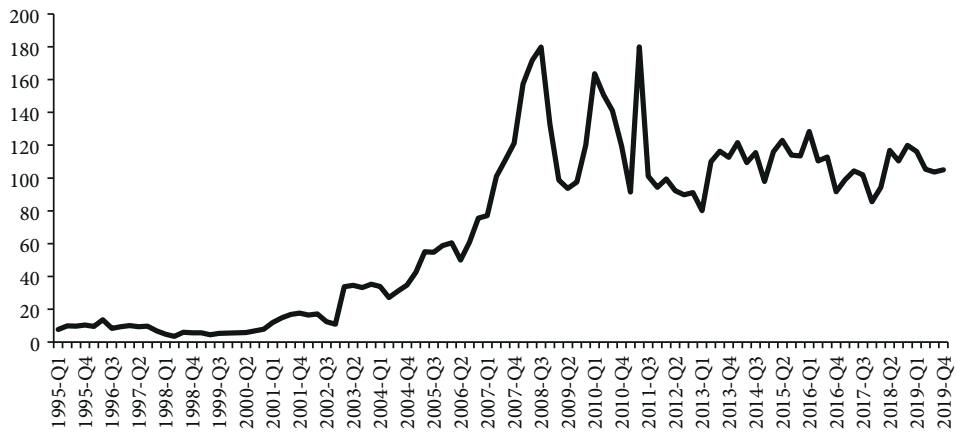

Because of the continuously high Selic rate -and after 2003 due to the accumulation of international reserves as well, which lowers the risk of investing in the country- Brazil has become a hotspot for another type of speculative transaction: Forex derivatives (Rossi, 2016). Graph 5 displays the notional volume of derivatives transacted in Brazil from 1995 to 2019. The volume of exchange rate derivatives grew in step with the increase of Brazil’s international reserves. High interest rates and the accumulation of foreign reserves have made Brazil a harbor for investors looking to hedge their financial investments, even if Brazil is not their ultimate destination.

Source: Authors’ elaboration based on Bank for International Settlements (BIS, 2020).

Graph 5 Exchange rate derivatives transacted in Brazil - Q1 1995 to Q4 2019 (notional values, quarterly, USD billion)

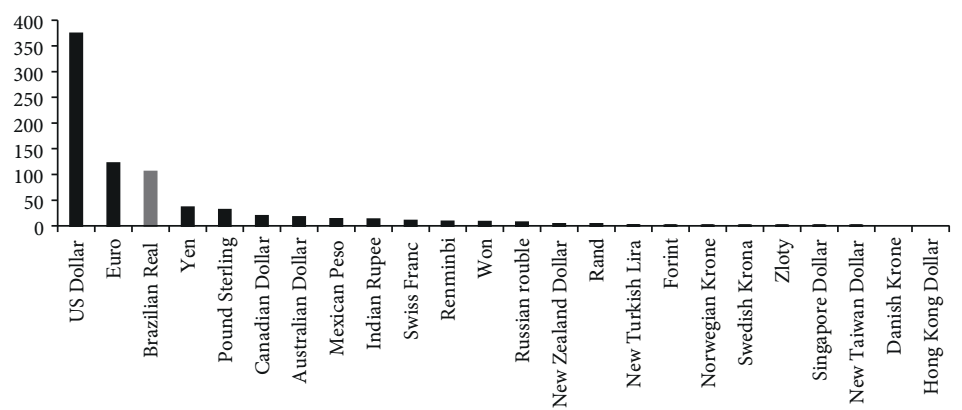

To make it clear how Brazil became the place to hedge financial transactions, Graph 6 compares the respective notional values of futures and options derivatives contracts in Brazil in the last quarter of 2019. In terms of global rankings, Brazil is third in the volume of notional value of derivatives (futures and options) contracts. However, the Brazilian real is not even a top-ten currency in the hierarchy of the global monetary and financial international system.

Source: Authors’ elaboration based on BIS (2020).

Graph 6 Notional value of futures and options derivatives exchange rate contracts in 2019 (USD billion)

The reason behind the position that Brazil occupies in terms of derivatives contracts concerns (i) the openness of the capital account, which makes it easy for money to enter and leave the country -a feature highly valued by speculative capital flows; (ii) the premium paid by the high base rate of the country and consequently by other financial assets- chiefly government bonds; and (iii) the volume of Brazil’s international reserves, which reduces the exchange rate risk faced by external investors when they use Brazil for their global transactions.

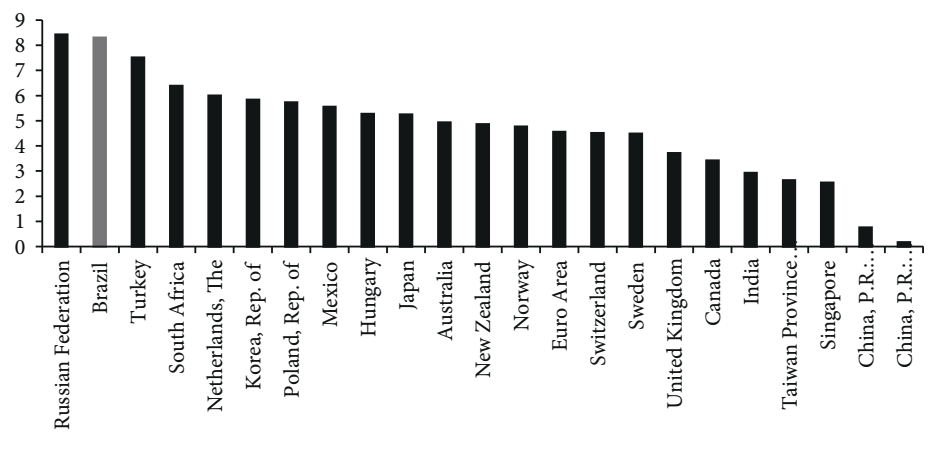

The consequence of Brazil’s status as a global hotspot for financial transactions was the outstanding volatility of the country’s exchange rate. As per the International Monetary Fund (IMF, 2020) and as illustrated in Graph 7 , Brazil had the second-highest exchange rate volatility index in the world in 2020, just behind Russia. This is the fallout from which Brazil has become in the financially globalized world an arena for all manner of financial speculation. Whether a financial speculator is seeking easy gains or looking to hedge their financial portfolio, Brazil can serve both roles.

Source: Authors’ elaboration based on IMF (2020).

Graph 7 Exchange rate volatility, 1995 to 2019 (Average of the mean of each year)

To sum up, Brazil first engaged in financial globalization as a payer of high interest rates in order to manage the exchange rate during the process of disinflation. However, even after the flexibilization of the exchange rate, the country in essence remained trapped in the exchange rate-domestic prices link. One third of Brazil’s price level relies on the exchange rate, so even after abandoning the managed exchange rate, the fear of significant pass-through from the exchange rate to domestic prices drove the CBB to continue administering the Selic rate at high levels. Thus, as of the mid-1990s, the country is a place of secure and reasonable financial gains regardless of the exchange rate policy.

In the 2000s, the CBB chose to accumulate foreign reserves to equip the tools available for policing the exchange rate. However, Brazil has also become a place where speculative investors hedge when speculating elsewhere. The great financial openness of the country, the tendency toward high interest rates, and the reduced exchange rate risk because of the great stock of external reserves have made Brazil a perfect place for investors aiming to hedge their portfolio.

Therefore, bearing this position in the financial globalization, Brazil’s place in the globalized world did not bring with it economic development. The main outcome, so far, has been great volatility in the exchange rate, which changes with the shifting humors of global liquidity. Due to the link between the exchange rate and domestic prices, Brazil is threatened by changes on the level of the exchange rate. Consequently, the Selic rate is continuously fluctuating according to the deregulated capital flows into and out of the country. The CBB Selic rate thereby maintains a level unfavorable to productive investments. Thus, the financial liberalization of the Brazilian economy diverted the country’s growth path and made Brazil a hotspot for speculative capitals.

4. Final remarks

Those who criticize financial liberalization continuously invoke Keynes (2007) to advocate for the speculative nature that financial investments can bear. Of course, these speculative investments do not circumscribe themselves to the borders of a country; that is why these speculative investments asked for and built financial globalization.

During the 1994 Real Plan, Brazilian economic authorities took for granted that a broad and rapid opening of the economy would necessarily entail economic development. However, such development did not materialize, and the degree of openness of Brazil’s capital account remained unchanged. Nevertheless, the match between a high interest rate that had always prevailed in the country and the lower exchange rate risk that emerged with the greater international reserves of Brazil have turned the country into a hotspot for financial gains and hedge within the international monetary and financial system.

The outcomes of this pathway have been detrimental to the Brazilian economy. On the one hand, even the direct investment that comes to the country arrives in pursuit of financial yields. On the other hand, Brazil’s exchange rate derivatives market has taken on outsized proportions compared to the country’s economy and its importance in the international monetary and financial system. The outcome is clear: The country has had the second-greatest exchange rate volatility in the world economy since 1995, and volatility, as the post-Keynesian theory extensively argues, brings only instability and disturbance to economic activity.