nova página do texto(beta)

nova página do texto(beta) Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Similares em

SciELO

Similares em

SciELO

Permalink

PermalinkIntroduction

In recent years, foreign bank entry has increased a great deal in emerging market economies (EMES). Latin America and the transition countries of Central Europe -where in some countries foreign banks have already over fifty percent of total banking assets- have been quickest to permit foreign participation in banking, while in Asia, Africa, the Middle East, and the former Soviet Union, progress has been much more modest. On the one hand, this trend is a consequence of the process of banking internationalisation of some financial firms that result from both financial deregulation and technological changes that have changed deeply the landscape of banking industry all around the world. Financial institutions are seeking to diversify their activities -in terms of products and services, or geographically- and to increase their minimum scale of operations to remain competitive and to enhance their ability to generate profits. On the other hand, foreign bank entry, particularly in EMEs, is the result of the flexibility of the legal rules concerning the treatment related to foreign bank penetration. Its motivation is mainly related to the possible benefits of foreign bank penetration in terms of modernisation and strengthening of the domestic financial system.

The recent expansion of foreign banks in Latin American countries is very impressive in terms of its rhythm. A International Monetary Fund (IMF) study relates that the participation of foreign banks from Spain, United States (US), United Kingdom and the Netherlands in total Latin American banking assets grew quickly, changing deeply the ownership structure of the financial system (Clarke et al., 2001). This development reflects a new banking strategy of international expansion. Banks have not expanded abroad only to serve its home multinational enterprise or to explore opportunities that come from international trade, but also, and increasingly, to dispute domestic markets with local banks in host countries. This transnational rivalry between banks is accompanied by bank functions redefinition. The traditional lending-deposit business that no long ago characterized banking firms was shifted by the universal global bank that combines ancient commercial functions with activities proper of investment banks. The diversification of financial activities is one of the new aspects of banking competition and it has been responsible by the development of securitization and new connections between financial markets and credit markets.

Argentina and Brazil experienced a simultaneous process of foreign bank entry after the 1994-1995 Mexican crisis. The quick pace of growth of foreign banks into the Argentine and Brazilian banking system was seen by the monetary authorities as a solution to face the effects of Mexican crisis over the domestic financial system. According to the literature, with the entrance of foreign banks, emerging countries could (i) have better access to foreign savings, an essential ingredient to finance development; (ii) enhance financial system, increasing its soundness in order to improve the countries’ resistance to shocks; (iii) incorporate new financial technologies, introducing new management methods and new financial products; (iv) improve operational efficiency of banking sector (Levine, 1996; Peek and Rosengren, 2000). It was expected that this set of changes would converge to growing credit facilities and strengthening historically incipient domestic capital markets.

The results of foreign bank entry in Argentina and Brazil, however, did not reach what was expected initially. The evidence shows that financial system efficiency, that is, the financial system capacity to create finance to sustain production and investment, has not improved in Argentina and Brazil. The increased presence of big foreign global banks in Argentine and Brazil, since 1995, has not resulted in a sustainable credit growth; macroeconomic instability has been the hallmark in the two countries.

This paper aims at analyzing the recent experience of foreign bank entry in Argentina and Brazil, focusing on its determinants and effects.1 It is divided in 5 sections plus this introduction. Section 2 examines the concept of efficiency of the financial system, with special emphasis on the effects of foreign bank entry in EMEs. Section 3 analyzes the determinants of foreign bank penetration in Argentina and Brazil, while section 4 examines its effects on the domestic financial system. Finally, section 5 summarizes the main arguments developed in the paper.

Financial system efficiency and foreign banks

The concept of efficiency of financial systems is a measure of their success in reaching macro and microeconomic efficiency. Efficiency has two distinct functions: one concerns the stability of the financial system; another is related to the allocation of the real resources. Macroeconomic efficiency concerns to the stability of the financial system, both as a payment system and as an intermediary of loanable funds, that is how financial system supports financially stable growth. Microeconomic efficiency relates to the ability to provide finance and funding for the investors and other economic agents at the lowest possible cost.2

Microeconomic efficiency means that bank spread must not be greater than necessary to cover the interest paid, administrative costs and credit risk. The literature points out that the increasing presence of foreign banks could bring positive effects to the degree of efficiency of the domestic financial system, as foreign banks are generally more efficient than domestic competitors (Clarke et al., 2001). For example, Focarelli and Pozzolo (2000) argue that foreign banks go to developing countries in order to explore the relative inefficiency of domestic banks. In general, banks that expand abroad are typically the “best of the crop” in the country of origin. They show that foreign banks are more efficient than domestic banks in EMEs, introducing into the host countries better practices of management and new technologies. Thus, one can conclude that the increasing presence of foreign banks must improve microeconomic efficiency, lowering the costs of supply of credit.

Macroeconomic efficiency is obtained when banking system provides loans in sufficient volume to finance investments and other spending in order to achieve full-employment with the possible minimum increase in financial fragility. In globalized open economies, the functioning of the banking system must avoid vulnerability with respect to international rate of interest and exchange rate shocks in order to be considered as efficient.

The empirical literature presents some evidence of positive macroeconomic impacts associated with the increasing presence of foreign banks in EMEs. First, global banks bring to the host country practices consistent with the financial and regulatory reporting requirements of their home country. As financial reports of global banks are supposed to be more detailed and more accountable than developing countries ones, the presence of foreign banks in the domestic financial system is an incentive to local banks to adopt better accounting practices (Peek and Rosengren, 2000, p. 48). This, in practice, reduces the risks associated with financial intermediation and should increase credit supply.

Second, foreign banks are less sensitive to domestic shocks than domestic banks. As their portfolios are better diversified, the impact of a domestic shock, that could seriously affect domestic banks would be more easily absorbed by foreign banks.3 If all this is true, a financial system entirely occupied by domestic banks should be more vulnerable to economic shocks than financial system with the presence of foreign entities. So, the presence of foreign banks reduce the impact of shocks over the financial system, as they are able to reestablish more quickly the financial flows to the real sector and they are less vulnerable to economic shocks.4

Third, the presence of foreign banks in EMEs has another function: in turbulent times, global banks are often an important source of new capital for a devastated banking sector after a crisis. As the recapitalization of banks requires investors that were not fully affected by economic shocks, foreign banks, specially global ones, are the natural candidates to do the job.

Last but not least, Peek and Rosengren (2000, p. 48) point out that the presence of well-capitalized foreign banks may lessen the severity of a domestic shock by mitigating the extension to which the funds of worried domestic savers and investors flee the country when a shock is anticipated: a foreign bank is a safe heaven for depositors who might otherwise choose to remove their funds from the country rather than risk leaving funds in a problematic domestic bank. The safety would be granted if the host country allows deposits denominated in foreign currency, because customers would be more comfortable in placing such deposits in foreign banks that have more ready access to foreign currency during banking crises, with the lender of last resort of the foreign bank being the central bank in the bank’s home country rather than that of the host country.

The penetration of foreign banks in Argentina and Brazil was seen by their national governments as an important part of the solution of banking system troubles that followed the Mexican crisis, as doubtful banks were acquired by healthy ones. However, the realities of Argentina and Brazil did not allow concluding that foreign bank brought macroeconomic efficiency to the domestic banking sector, despite of the fact that foreign banks may have eventually increased microeconomic efficiency.

As we will see in the next section, there is no reason to suppose that foreign bank entry resulted in a significant improvement in the finance conditions of Argentine and Brazilian economies and also in their financial stability. Indeed, foreign bank entry in Argentina and Brazil did not cause any greater change in banking behavior in terms of portfolio allocation, credit policy, etc. This is explained by the fact that banking behavior has been mainly determined by the macro-institutional environment of both countries, that has resulted in a convergence of behavior of both domestic and foreign banks. In particular, macroeconomic instability prevented the development of financial relations in Argentina and Brazil.

Determinants of foreign bank entry in Argentina and Brazil

Determinants of foreign bank entry in Latin America

Banking crises, deregulation and globalization of financial services have led to a significant increase in the presence of foreign banks in EMEs in the second half of the 1990s. Consolidation has accelerated recently in banking industry in EMEs, changing a traditionally highly protected industry. In this connection, Hawkins and Mihaljek (2001, p. 3) states that “global market and technology developments, macroeconomic pressures and banking crises in the 1990s have forced the banking industry and regulators to change the old way of doing business, and to deregulate the banking industry at the national level and open up financial markets to foreign competition. […] These changes have significantly increased competitive pressures on banks in the emerging economies and have led to deep changes in the structure of the banking industry”.

Although the same forces of changes are determining the process of banking consolidation in mature markets [US, European Union (EU) and Japan] and emerging markets (Asia, Latin American and Central Europe), there are some particular features when one compares both experiences ( IMF, 2001):5

International mergers and acquisitions (M&As) cross-border are an exception in mature economies, but they are the rule in emerging markets. In emerging markets it can be observed an increase in the market share of foreign banks in the domestic banking sector, while this trend is weaker in mature countries. Indeed, in the latter countries banking consolidation emerged as a consequence of financial deregulation implemented during the 1980s and 1990s, as typically is the case of us where the segmentation of the financial system was gradually being eroded. On the other hand, in emerging markets international M&As cross-border, involving foreign banks, in most countries have been the rule.6

Banking consolidation in mature markets has served mainly to increase the efficiency -in the search of scale economies, scope economies and revenue economies- or the market power of the major banks,7 while in EMEs it served mostly to help to face banking crises during the 1990s. Banking crises caused enormous disturbs in emerging countries, in most cases due to the very nature of financial liberalization. Banking crises accelerated, if not determined, the implementation of privatization programs of public-sector banks.

In most cases, banking consolidation in emerging markets was of the type “government-driven”, that is the government conducted directly or indirectly the process of banking consolidation through programs of banking restructuring, privatization of public banks, flexibility in the rules of foreign bank entry, etc., while in mature markets it was mainly “market-driven” style, that is it was the result of the responses of financial institutions to the policies of financial deregulation and privatization during the 1970s and 1980s.

Banking consolidation in Latin America has been the most advanced among the EMEs. The main “forces of change” of this process were the banking crises that resulted from the contagious 1994 Mexican crisis and the consequent foreign banks entry: “Financial crises and the need to (re-)establish functioning banking systems created a one-time set of opportunities to invest in financial institutions and to expand business in EMEs in the second half of the 1990s. A standard response to crises by EME government, encouraged by the international financial institutions, was to accelerate financial liberalization and to recapitalize banks with the help of foreign investors. This was the case in Latin America in the years following the 1994 Mexican crisis”. (CGFS, 2004, p. 6.)

Therefore, there was an active government role in the conduction of banking consolidation in Latin America after the Mexican crisis, although since late-1990s this process has been increasingly market-driven. Note that in Latin America, in contrast with the main countries in Asia and Central Europe, the reduction in the quantity of banking institutions was followed by a remarked increase in banking concentration (except Venezuela), according to Table 1.

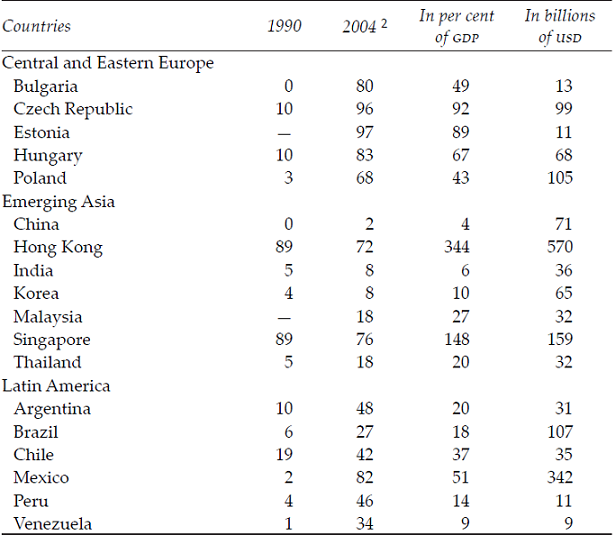

The share of bank assets held by foreign banks in EMEs has increased considerably since 1990. Foreign ownership of the banking sector is substantially higher in Latin America and central and eastern Europe than in Asia (Table 2). While in central and Eastern Europe foreign banks now control more than 60 percent of total banking assets, in the major countries of Latin America, except Brazil, the share of assets owned by foreign banks is more than 30 percent. In Mexico and Argentina the market share of foreign banks (in terms of total assets) was 82 percent and 48 percent in 2004, respectively.

Table 2: Share of bank assets held by foreign banks ¹

Notes: 1/ Percentage share of total bank assets. 2/ Or latest available year.

Source: Domanski (2005, p. 72), based on data from ECB and national central banks.

Following the increase of the market share, the range of foreign bank activity in EMEs has broadened a great deal recently. Historically, foreign banks focused primarily on the provision of financial services to their home-country clients in international transactions. However, since the 1990s, foreign investments have increasingly been driven by more general profit opportunities in local markets. Indeed, the present strategy of global universal banks is aimed at diversifying their activities into some domestic markets through a network of branches and greater integration into the local market, while in the past bank’s strategies were geared mainly to serving their home-country customers and also giving some support to domestic firms to access the international financial market.8

Latin America received one of the biggest influxes of foreign direct investment (FDI) in the banking sector since the middle of the 1990s. However, one cannot understand the wave of bank FDI isolated from the general movement of FDI to Latin America during the 1990s. Indeed, the Latin America and Caribbean region received record levels of FDI in the 1990s, with inflows totaling US$76.7 billion only in 1998, an amount that corresponded to around 41 percent of total FDI flows to developing countries (ECLAC, 2000, p. 35-36). The majority of FDI flows in the financial sector went to Latin America as well. Between 1991 and 2005, transactions targeting banks in the region accounted for US$58 billion or 48 percent of total cross-border M&As targeting banks in EMEs, followed by emerging Asia with US$43 billion (36 percent of total M&As) and central and Eastern Europe with US$20 billion (17 percent of total M&As).9

In 1991-2005, the majority of FDI in banking sector to Latin America came from European countries: 46.6 percent from Spain, 10.0 percent from United Kingdom, and 6.4 percent from Netherlands10 (Domanski, 2005, p. 75). Some of the main determinants of the expansion of European banks in Latin America can be summarized as follows:

The process of restructuring of the banking sector under European Economic and Monetary Union (EMU). For some European banks expanding abroad is not only a source of earnings diversification, but also a way of strengthening their position in the European banking market considering the increasing market competition in banking in the European Economic Area. The European bank’s strategy for Latin America may be interpreted as a response to this more competitive environment, in which several factors were eroding income from traditional banking business.11 Further, due to political and regulatory constraints, there are some impediments to M&As within EU countries, but incentives to such activity outside the bloc.12 The preference for Latin America, and to a lesser degree Central and Eastern Europe, is partially due to the fact that Southeast Asia during the second-half of 1990s was in crisis, while the Indian and Chinese financial system remained closed to foreign banks, leaving Argentina, Brazil and Mexico as the main big emerging markets open to FDI in bank sector.

In particular, the dynamics of the internationalization of the Spanish banks since they were the main protagonists in the recent wave of foreign banks entering Latin America. These banks pursued growth strategies based on M&As in their natural market before they launched their international growth strategy. So, they already were mature banks when they decided to expand overseas. Indeed, with the implementation of EMU and the perspective of introduction of the euro, the larger Spanish banks -in particular, Banco Bilbao Vizcaya (BBV), Banco Santander and Banco Central Hispanico (BCH)- had to look beyond their natural borders in search of global markets, in order to maintain their competitive position and to defend themselves from the threat of hostile bids by either local or foreign competitors. At the initial stages of this process there was a proliferation of alliances and co-operation agreements with other financial institutions, chiefly within the European Union, while the second phase has involved a fast-paced, aggressive expansion strategy aimed at the main Latin American markets.13

The deregulation process in Latin America, in the broader context of economic and political reforms, since early 1990s, made room for the entry of foreign companies into key economic sectors, such as banking, telecommunications and utilities. Bank privatization programs in general formed part of longer-term public sector reforms, which also involved privatization of major public enterprises with the aim of consolidating the public finances and cutting borrowing requirements (Hawkins and Mihaljek, 2001, p. 13). Further, deepening the role of the market was also a major motive.

The Latin American banking sector offers much better prospects for increasing returns to financial institutions, since the intermediation margins with which banks operate in these countries are considerably higher than in the developed world. While the domestic banks’ average margin on assets (net interest income over total assets) in Latin America was 5.76 percent for the period 1988-1995 (in Brazil it was 6.6 percent and Argentina 9.9 percent), in OECD countries it was 2.80 percent for the same period (Claessens et al., 2001). On the other hand, Latin American banks steadily improved their already high profitability during the 1990s, although net interest revenue has been stable. Their profitability is high both compared to G3’s countries and other EMES.14

The potential gains in efficiency are high in Latin America, since the degree of banking efficiency is in general lower than that in developed countries. The domestic banks’ ratio of operating costs to assets in Latin America was on average 5.5% in 1992-1997, while it was 1.7% in G3’s countries (US, Japan and Germany), 1.6% in East Asia and 4.1% in Central Europe, in the same period (Hawkins and Mihaljek, 2001, p. 6). The high operating cost (as well as high interest rate spreads) of domestic banks in Latin America are in large part the legacy of the high-inflation period of the 1980s and the early 1990s, when inflationary revenues generated easy profits for the banks and, consequently, there was little pressure to cut costs.

Determinants and some features of foreign bank entry in Argentina and Brazil

The recent process of banking consolidation in Argentina is somehow similar to the Brazilian experience in the sense that in both countries the authorities responded to the banking crisis caused by the effects of the contagious of 1994-1995 Mexican crisis with an array of support programs for financial institutions and their borrowers. These programs intended to bolster the health of the financial sector and, at the same time, to open the sector to foreign banks, since the presence of these banks could help to strengthen the banking sector.15 Besides, the entry of foreign banks was used as a policy to weaken the effect of local monopolies that had been established under the previous regulatory structure.

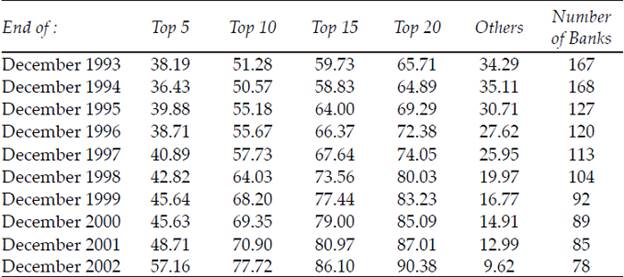

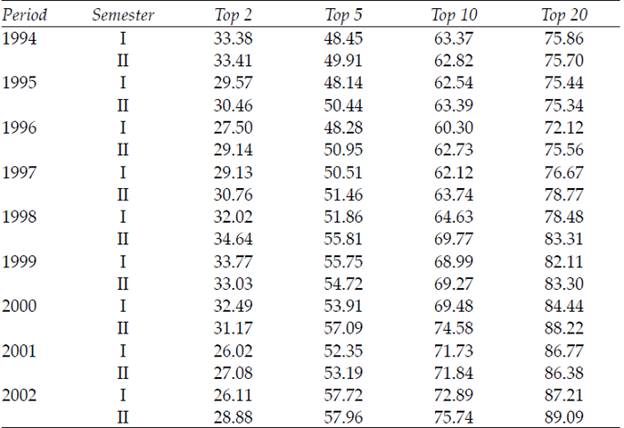

Both countries had important structural changes in their financial systems during the 1990s, evidenced by some decline in the market share of state-owned banks, a decrease in the number of financial institutions, including banks, and an increase in banking concentration. In Argentina the 1980s high inflation period caused shrinkage in the number of banking and non-banking financial institutions probably due to the deep process of economy’s demonetization. More recently, after the 1995 banking crisis, there was a huge decrease in the number of both public (provincial and municipal) and private banks that was followed by a quick increase their share in the banking concentration: the top 10 banks increased from 50.6 percent in December 1994 to 77.7 percent of total assets in December 2002, a significant increase of more than 50 percent in banking concentration in just nine years (see Table 3 and 5). In Brazil, banking consolidation, although less intensive than in Argentina, accelerated a great deal after 1995: The number of banks (multiple and commercial ones) declined from 240 banks in December 1995 to 166 banks in December 2002 (Table 4) while the market share of top 10 banks (as percentage of total assets) increased from 63.4 percent in December 1995 to 75.7 percent in December 2002 (Table 6). These changes in the banking sector in Argentina and Brazil can be attributed to some basic factors, such as banking restructuring policy, programs of banking privatization and the foreign bank entry, following some general trends of banking consolidation in EMEs, as we have seen in the former section.

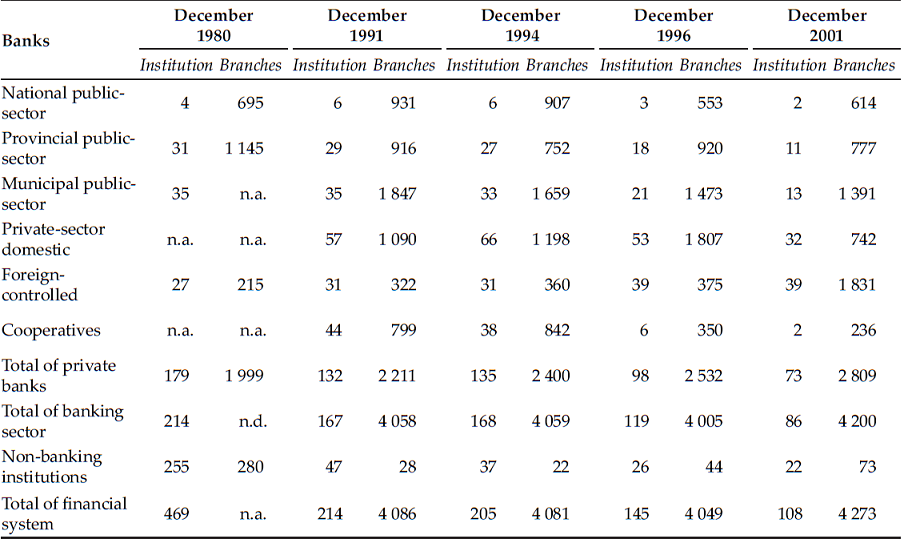

Table 3: Financial institutions and branches in Argentina, 1980-2001

Source: Central Bank of Argentina, in Fanelli (2003, p. 50).

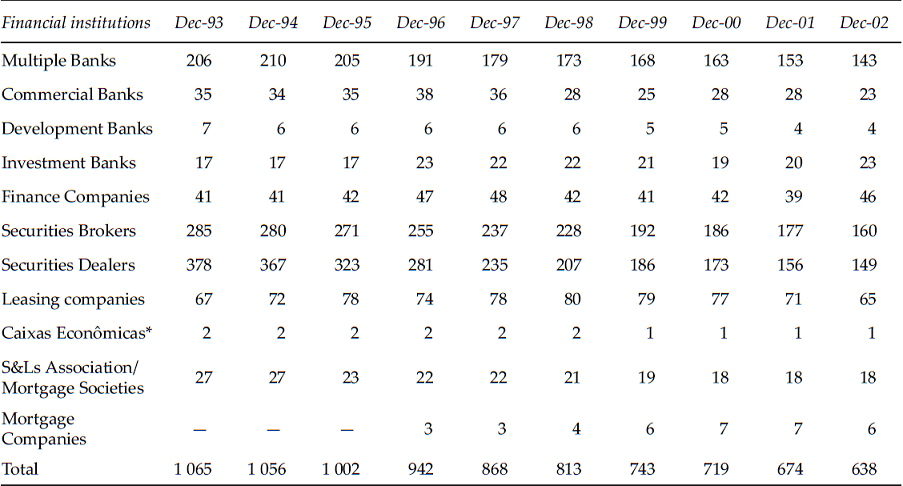

Table 4: Number of financial institutions operating into the Brazilian Financial System

*/ “Caixas Econômicas” are public banks (federal or state ones) that combine commercial activities with activities housing financial.

Source: Central Bank of Brazil, Financial System Organization Department.

Table 5: Banking concentration in Argentina (as percentage of banking assets)

Source: Association of Banks of Argentina (ABA), with data from the Central Bank of Argentina.

Table 6: Banking concentration in Brazil (as percentage of total assets)

Source: Rocha (2001) until 2000; authors’ calculations for 2001-2002, both with data from Central Bank of Brazil.

However, there are some differences and particular features about the recent Argentine and Brazilian experiences related to foreign bank penetration.

Firstly, financial liberalization was more intensive in Argentina than in Brazil. Financial liberalization in Argentina followed the implementation of the Convertibility Plan.16 Actually, the currency board system required financial liberalization as a way to assure a high and stable influx of external capital in order to sustain an adequate level of liquidity in the domestic financial system. Therefore, between 1989 and 1994, almost all the regulatory controls on domestic and external operations in the financial system, that had been replaced during the 1980s due to the high inflation and external constraints, were lifted (Hermann, 2001). Within this new context, foreign banks had full freedom to issue deposits and to extend credit in foreign currency (that is, dollar), to get resources abroad, and to issue subordinated debt in external financial markets. Indeed, prudential regulations stimulated a strong and quick increase in dollarization in Argentina during the 1990s. In Brazil financial liberalization was slower and more restrictive compared to Argentina: during the 1990s only the investments of institutional investors in assets negotiated in Brazil were partially liberalized (Annex IV and V of Central Bank of Brazil), although non-resident accounts in foreign markets (CC5) had been used very often by residents -mainly financial institutions- to send dollars abroad during turbulent periods of speculative attack on the Brazilian currency -the real-.17 After the 1999 Brazilian currency crisis and the adoption of a floating exchange rate regime, economic authorities implemented a lot of norms that resulted in greater flexibility in exchange rate market, including the unification of the exchange rate markets (floating and free ones), simplification of the procedures related to capital remittance to other countries, and extension of maturities for exchange rate coverage related to exports operations.

Secondly, foreign bank opening up was much deeper in Argentina than in Brazil during the 1990s. Indeed, while Menem’s government lifted all the restrictions concerning the presence of foreign banks in the Argentine financial system, in Brazil Cardoso’s government was more selective in terms of foreign bank entry. Legislative Intent no. 311, from 23/08/1995, an act from the Brazilian President, allowed the President exceptionally to authorize, case by case, the entrance of foreign banks in Brazil. On that occasion, Brazilian government announced that foreign banks would not be allowed to open new branches or acquire smaller banks unless they purchased one of the troubled state-owned banks. Although 1988 Brazilian Constitution prohibited the installation, in the country, of new branches of financial institutions domiciled abroad, until a new comprehensive law governing the financial sector could be developed, it also opened a chance to foreign banks entry through authorizations resulting from international agreements, from reciprocity or from interest of the Brazilian government. Within this legal context, foreign banks entry in Brazil was approved on case-by-case basis, mainly to recapitalize troubled banks. The increase of foreign participation in the Argentine banking market was deliberately promoted by a restructuring and concentration policy implemented after the contagion of Mexico’s Tequila crisis, that severely tested the Convertibility system and the financial sector -sparking an outflow of almost 20 percent of system deposits-.18 During the Tequila crisis, efforts were undertaken to reestablish confidence in the banking sector that “included the introduction of deposit insurance, a renewed commitment to privatizing inefficient public sector banks, the liquidation or consolidation of nonviable entities, and the dedication of substantial resources to strengthening supervisory oversight and the regulatory framework. Within this context, foreign banks were permitted to play an important role in recapitalizing the Argentine banking system” (Dages et al., 2000, p. 21).

In Argentina and Brazil, capital requirements were stricter than those imposed by the Basel Committee: The capital asset rate was set at 11.4 percent in Argentina and 11.0 percent in Brazil during the 1990s as opposed to the 8 percent level recommended by the Basil Committee. In both countries foreign bank entry was justified by the necessity of strengthening the financial system and also to incorporate criteria and international experiences of banking supervision in the domestic financial system. In Argentina, however, one further reason highlighted by monetary authorities was the greater facility to access external capitals by the domestic financial system, since this was considered essential to the modus operandi of convertibility regime. Indeed, foreign banks in Argentina had, ceteris paribus, an important role in maintaining the capital inflow to the country in regular levels and also to provide a contingent credit line to the central bank in the event of a crisis.19

Thirdly, the Argentine financial system was weakened a great deal during the 1980s high inflation period, as a result of both the process of demonetization and financial desintermediation, while the Brazilian financial system strengthened during the high inflation period, due to the development of a broader domestically-denominated indexed money and also the increasing development of a modern clearing system in the banking sector in order to support the clients’ demand for immediate information and the clearing of checks. Consequently, the decreasing in M1 (cash plus deposit deposits) did not result in lost of funds to the Brazilian financial system. In Argentina, in turn, there was a deep process of dollarization that was followed by an enormous decrease in financial deepening. Informal dollarization in Argentina began since the first and not-well succeeded experience of financial liberalization in 1977-1982.20

During the 1994-1995 Mexican crisis, the Brazilian banking sector faced a liquidity crisis that did not result in a systemic crisis, due to the liquidity provision to banking sector by the Central Bank of Brazil and the successful implementation of PROER, the Program to Support the Restructuring and Strengthening of the National Financial System. This program aimed to preserve the solvency of the financial system by removing distressed banks and bolstering those that remained in business.21 In Argentina, due to the lack of adequate mechanisms for provision of liquidity for banking sector, as the Central Bank of Argentina faced constraints to act as lender of last resort, the contagion of the Mexican crisis had a huge impact on the health of the financial system. Consequently, financial liberalization (including foreign bank entry) found domestic banks very bad capitalized, with difficulties to attract deposits and to borrow in both domestic and international financial markets. These structural features of the Argentine and Brazilian financial system explain, at least partly, the much better reaction of Brazilian private domestic banks to foreign bank entry compared to the Argentine ones.

Finally, it is worth noting that while the main acquirers of banks in Argentina during the 1990s were foreigners, private domestic banks commanded the banking M&As wave in Brazil.22 In both countries prevailed European banks as the main players among the foreign banks: in Argentina, the biggest foreign banks are the Spanish Banco Rio de la Plata Santander and Banco Francês BBVA, and the British HSBC Banco Roberts, while in Brazil the major banks are the Spanish Banespa-Santander, the Dutch ABN Amro Real and the British HSBC. In Argentina foreign bank entry occurred mainly via the acquisition of existing operations: Foreign shareholders acquired stakes in private institutions with a national or regional franchise (for instance, privatized provincial and municipal banks). Such acquisitions accelerated a great deal in the beginning of 1996, with foreign banks acquiring control of stakes in a majority of Argentina’s largest private banks. In Brazil, like as in Argentina, foreign bank entry occurred initially via the acquisition of some troubled banks (Bamerindus, for instance). Increasingly, bank take-overs embraced a strong bidder and sometimes a weak, but not yet insolvent, target, such as the acquisition of Noroeste by Santander and Real by ABN Amro. Unlike Argentina, where foreign bank acquisitions included two of the largest three private banks (that is, Banco Rio de la Plata, and Banco Francês), foreign acquisitions in Brazil involved mainly medium-sized banks, such as Excel-Econômico and Banco Geral do Comércio (the exception was the acquisition of Banespa by Santander).

Effects of foreign bank entry in Argentina and Brazil

In this section we compare the effects of foreign bank entry in Argentina and Brazil, highlighting some common features as well as the differences.

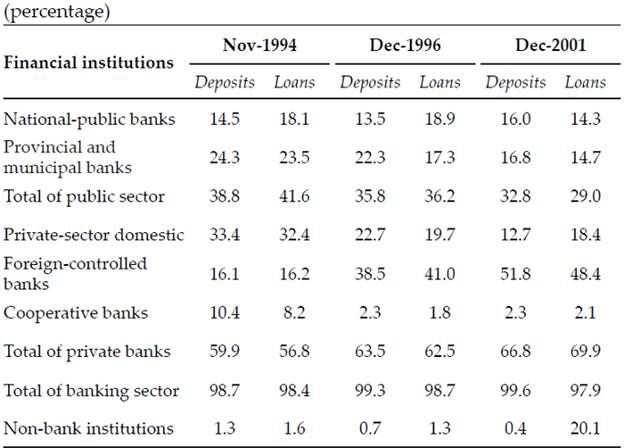

In Argentina and Brazil, as a result of the recent foreign bank penetration, there was a dramatic expansion of foreign control in the domestic banking sector. In Argentina foreign control over deposits and loans increased from 16.1 percent and 16.2 percent, respectively, in November 1994 to 51.8 percent and 48.4 percent, in December 2001, at the cost of the decline of the market share of both provincial-municipal banks, domestic private banks and cooperative banks (Table 7). In Brazil foreign control over deposits and assets increased from 4.4 percent and 9.8 percent, respectively, in December 1996 to 19.8 percent and 27.4 percent in December 2001, at the cost of the decline of the market share of state-public banks and federal-public banks23 (Table 8).

Table 7: Market share in Argentina's banking sector

Source: Central Bank of Argentina, in Fanelli (2003, p. 52)

Table 8: Market share in the Brazilian banking sector

*/ Mainly state-public banks; date excludes the two big federal banks. Caixa Economica Federal and Banco do Brasil

Source: Central Bank of Brazil

Comparing Argentina and Brazil’s experiences, the most obvious feature is that, after the wave of foreign bank penetration of mid-1990s, foreign banks in Argentina dominate the banking sector vis-à-vis domestic private banks, while in Brazil domestic private banks still dominate the banking sector. In Argentina, among the top 10 banks, seven banks were foreign, two banks were public banks -the bank leaders, Banco de la Nación Argentina (federal) and the Banco de la Provincia de Buenos Aires (provincial)- and only one bank was domestic private bank (Banco de Galicia y Buenos Aires), according to data from 2000. In turn, in Brazil (data from 2000), among the top 10 banks, four banks were foreign, four were domestic private, and two were federal ones (the leaders, Banco do Brasil and Caixa Econômica Federal). In terms of total deposits of banking sector, foreign-controlled banks had in Argentina 51.8 percent of total banking sector assets in 2001, while private-sector domestic banks had only 12.7 percent (public-sector banks had 32.8 percent of total assets). Therefore, roughly half of all banking sector deposits in Argentina were under foreign control, with foreign shareholder holding significant minority stakes in a number of other financial institutions. In Brazil, foreign banks had 20.1 percent of total deposits in 2001, while domestic private banks had 35.3 percent and public-sector banks (including Banco do Brasil and Caixa Econômica Federal) had 26.2 percent. Considering only the top 12 private-sector banks, the five major domestic private-sector banks (Bradesco, Itau, Unibanco, Safra and BBA) had 28.8 percentage of total assets of private-sector in 2001, while the seven biggest foreign banks had 21.2 percentage (Paula, 2003, p. 170).

One should consider that in Argentina foreign entities already operating in the country had a more solid situation than domestic ones, that had been much weakened due to effects of the Mexican crisis, as foreign banks had better conditions to access funds abroad. Thus, 1990s the financial liberalization found many domestic private banks very few capitalized and with difficulties to attract deposits. Furthermore, as we have already stressed, the Menem government lifted all the restrictions concerning the presence of foreign banks in Argentine financial system, which meant that domestic banks faced foreign banks’ competition in a moment that they were much weakened. In the case of Brazil, domestic private banks reacted positively to foreign bank penetration, improving their efficiency, obtaining revenue economies through cross-selling activities and at the same time expanding their activities organically or by mergers and acquisitions.24 In doing so, they maintained their hegemony in the domestic banking sector. According to Paula (2002, p. 87), “domestic private banks have some advantages over foreign banks which they can exploit, since they are more adapted to the peculiarities of the Brazilian banking market. Their active reaction to foreign bank entry, cultural differences and high level of development and sophistication of the banking sector in Brazil, which resulted from its ability to adapt to the period of high inflation, may explain this behavior”.

In sum, in Brazil there was a banking restructuring that resulted only in a partial denationalization of the banking sector, with no dollarization. The most distinguished feature of the Brazilian experience was the reaction of the domestic private banks to foreign bank entry. In Argentina, financial liberalization resulted in the dominance of foreign banks that was accompanied by an increasing dollarization of the banking sector.

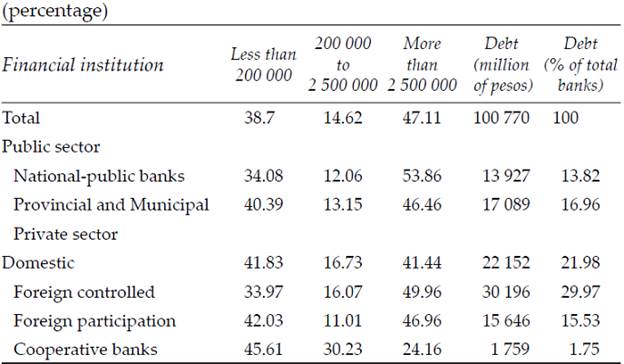

In broader terms, in both countries there was no significant difference in the behavior of foreign banks compared to the domestic private banks, as they tended to adapt the macro-institutional environment in the same way as the latter ones. According to Dages et al. (2000, p. 24), domestic and foreign private banks exhibit in 1994-1999 in Argentina “comparable loan behavior, coexist in the distribution of larger and smaller banks within the top twenty-five banks nationally, and have loan portfolios of similar compositions. The banks respond similarly to market signs, including real GDP (Gross Domestic Product) growth and real interest rates”, although they also “appear to have provided greater loan growth than what was observed among domestic-owned banks, while reducing the volatility of loan growth for the financial system as a whole”. Table 9 shows that the composition of bank portfolio -in terms of loans- in Argentina in 1994-1999 was very similar for domestically owned banks and foreign owned banks. Foreign banks generally engage in the same types of broad lending activities as domestic banks. Furthermore, banks in general have concentrated their loans in big debtors, with the exception of the cooperative banks (Table 10). In particular, banks with foreign control provided only 34 percent of their credit portfolio for loans less than 200 000 pesos (Argentina’s currency) in December 2002, while domestic private banks destined 42 percent for this category of loans. These data show some evidence that foreign bank entry can have resulted in an increase of the credit discrimination for borrowers with lower income.

Table 10: Loans share by credit size. Argentina, december 2002

Source: Central Bank of Argentina, in Fanelli (2003, p. 49).

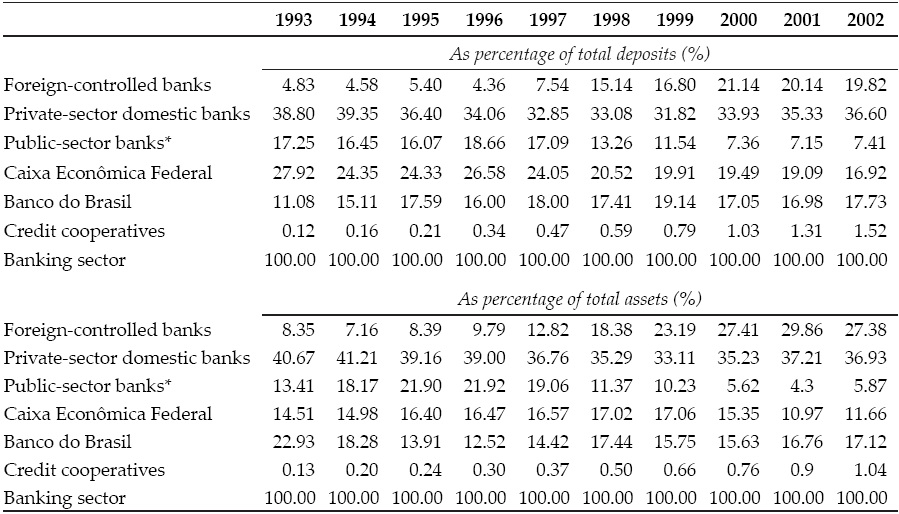

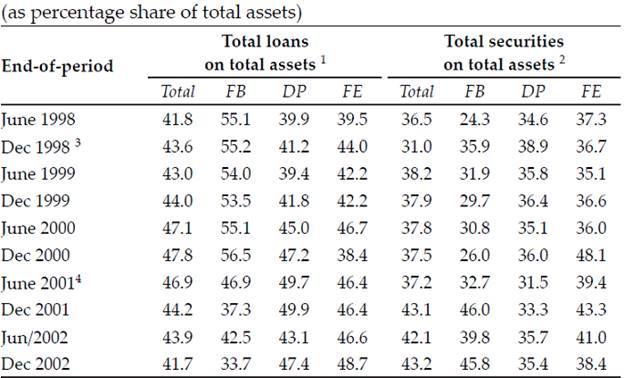

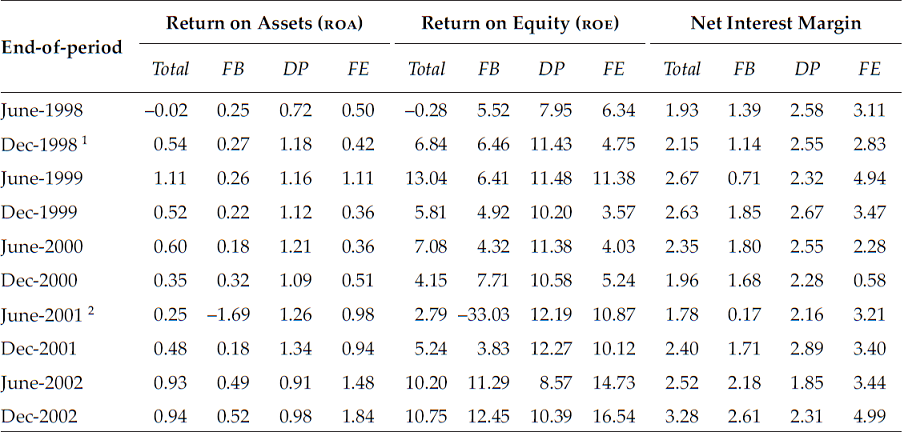

Similar behavior of foreign banks has been observed in Brazil, where recent studies have shown that operational characteristics of domestic and foreign banks are similar, as well as the balance sheet structures, dominated by interfinancial operations and by investment in securities, mainly public bonds (Carvalho et al., 2002; Carvalho, 2002). Foreign bank behavior has been even more conservative than domestic private ones in recent period (1998-2002): Total loans as percentage share of total assets has been in general higher in domestic private banks when compared to foreign banks (Table 11). Furthermore, the expected credit expansion due to the foreign bank entry did not occurred in Brazil, probably because this entry coincided with the external shocks that the Brazilian economy suffered in the last years. Finally, some studies (Guimarães, 2002; Paula, 2002) also show evidence that, contrary to the international literature that states that foreign banks are more efficient than domestic banks in EMEs (Levine, 1996; Demirguç-Kunt and Huizinga, 1998), there is no clear evidence that foreign banks in Brazil have been more efficient than domestic ones both in terms of operational cost and profitability. Domestic private banks profitability, determined mainly by the evolution of the profitability of the four major domestic private banks (Bradesco, Itaú, Unibanco and Safra), proved greater and more stable than foreign banks profitability during 1998-2002, while foreign banks’ net interest margins have proved larger than those of the domestic private ones (Table 12). Therefore, increased competition due to the recent entry of foreign banks has thus not brought about, at least in the recent years, the decline in the net interest margin which one might have expected according to the literature (Claessens et al., 2001).

Table 11: Banks portfolio in Brazil

Notes: 1/ Includes other loans besides normal loans. 2/ Includes also interfinancial operations. 3/ Excludes ABN Amro because of the incorporation of Banco Real. 4/ Excludes Santander because of the incorporation of Banespa.

DP: 4 major domestic private banks (Bradesco, Itaú, Unibanco and Safra); FE: 6 major foreign banks (Santander, ABN Amro, BankBoston, HSBC, Citibank and Sudameris); FB: 2 major federal state-owned banks (Banco do Brasil and CEF); Total: includes all financial conglomerates, public and private ones.

Source: Authors’ elaboration with data extracted from financial conglomerations in <www.bcb.gov.br>.

Table 12: Banks Profitability and Net Interest Margin, 1998-2002

Notes: 1/ Data excludes ABN-Amro because of the incorporation of Banco Real.

2/ Data excludes Santander because of the incorporation of Banespa.

DP: 4 major domestic private banks(Bradesco, Itaú, Unibanco and Safra); FE: 6 major foreign banks (Santander, ABN-Amro, BankBoston, HSBC, Citibank and Sudameris); FB: 2 major federal state-owned banks (Banco do Brasil and CEF);

Total: includes all financial conglomerates, public and private ones.

Source: Authors’ elaboration with data extracted from the financial conglomerations in Central Bank of Brazil.

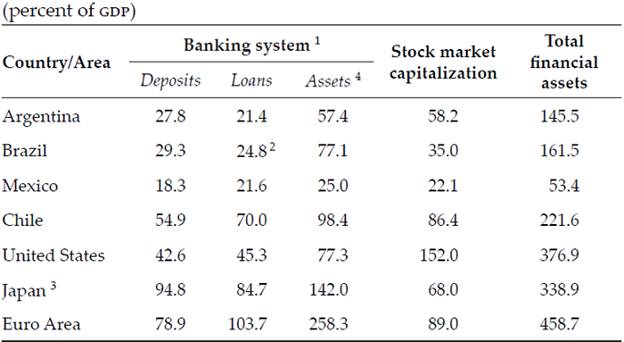

In both countries, unstable macroeconomic environment during the 1980s and 1990s impeded the development of credit relationships in the domestic economy, at the same time that this environment determined the behavior of the banks, including the foreign ones (Fanelli, 2003; Paula and Alves Jr., 2003). The Brazilian financial sector is large and bank-dominated, but the extent of intermediation -the ratio of intermediate financial flows resulting from the collection of deposits to the amount of credit actually extended- is small. The Brazilian banking sector seems very large when compared to those in other advanced Latin American economies (Mexico and Argentina), at the same time as it provides about the same proportion of loans as banks in these countries. On the other hand, in terms of asset size to GDP, the Brazilian banking sector compares to the US banking sector, but provides only half the loans in proportion to GDP (Table 13). Although Brazil has one of the most sophisticated banking sectors of the world in terms of technology and clearing system, the ratio total credit-to-GDP was only 24.8 percent in 2000, which is very low compared to developed countries. Furthermore, the Brazilian bond and equity markets are still in their infancy compared with those in more advanced countries: At end-2000, equity finance through stock market issues represented 35 percent of GDP in Brazil, about one-quarter the level in the US. In turn, the Argentine financial sector is only partially bank-dominated. Its bond and equity markets are larger than Brazilian ones -equity finance through stock market issues represented 58.2 percent of GDP in Argentina- but still very small when compared to advanced countries. The ratio of total credit-to-GDP in Argentina was very low, that is only 21.4 percent in 2000. On the other hand, in terms of asset size of financial system to GDP, Argentina and Brazil have less than half of US ones. In sum, financial deepening of Argentina and Brazil is still very underdeveloped, even after the 1990s years of succesful price stabilization.

Table 13: Financial system in some selected countries, 2000

Notes: 1/ Only deposit-taking, universal banks are considered.

2/ Data include commercial leasing.

3/ Bank data for Japan are as of March 2001.

4/ Data include total assets in banks’ balance sheet.

Source: Belaisch (2003, p.4), with data from Central Bank of Brazil, Federal Reserve Bank, ECB, BIS, and Federación Iberoamericana de Bolsas de Valores.

In both Argentina and Brazil financial intermediation has been short-termist, although short-termism in Argentina was followed by a high degree of dollarization in the portfolio of financial institutions and in financial contracts. This phenomenon had already begun in 1975 crisis, but it increased a great deal during the 1990s. The maturity of financial contracts in Argentina had been affected by changes in inflation, macroeconomic volatility and also in the macroeconomic policy regime. The length of the contracts, was slow, and it was often followed by an increase in dollarization, as the credit operations illustrate. Thus, the preference for flexibility prevailed in the portfolio decisions of financial institutions as well as in the use of short-run an a instrument to reduce banking risks. Within this context, financial institutions had a big flexibility to change their portfolio investments vis-à-vis financial and macroeconomic shocks. In Argentina during the 1990s there was a mismatching of currencies in the balance sheet of banks, due to the predominance of dollarized liabilities while the assets were partly denominated in domestic currency (peso), mainly during the turbulent times when firms sought to change their long-term debts denominated in dollars by short-term debts denominated in pesos. This situation put the banks in a very vulnerable position in case of a sudden increase in the costs to getting dollars and of an eventual exchange rate devaluation, which would result in the end of the Convertibility system. Argentine banks, expressing their liquidity preference during the recession that began in 1999, increased their investments in public bonds, as well as their liquidity requirements, and reduced the more risky assets in their portfolio, thus becoming increasingly submitted to government risk (Fanelli, 2003, p. 41). Due to the high degree of dollarization, an eventual break in the convertibility between peso and dollar would have -as it did have- chaotic and deep effects for the Argentine economy and its financial system. Indeed, the default on government debt in December 2001, followed by the devaluation of the peso in January 2002, had devastating consequences for the banking system as a sizable portion of bank assets (21 percent in October 2001) was in government liabilities.25 After the 2001 crisis, Argentine banks could not only give back the deposits to their clients, but also they could not pay their own debts.26

In Brazil, as in Argentina, financial intermediation has been short-termist, that is, in both preponderate the preference for flexibility of financial institutions. However, the supply of indexed and/or short term-domestic assets has satisfied the demand for flexibility of the economic agents (firms and households) without the necessity of dollarizing assets and contracts. Exchange rate hedge and interest rate hedge were offered by the government via the issuance of domestic public bonds, indexed to the dollar or to the overnight rate. These conditions allowed Brazilian banks to face the external shocks in 1997-2002 with a matched and protected balance sheet, they allowed them to combine banking soundness with high profitability.27

Finally, there is no evidence in Argentina and Brazil that in the long run foreign bank entry has contributed, by itself, to strengthen the financial system and to avoid balance of payments crises. In Brazil banking soundness has been obtained by the government offer of exchange rate -and interest rate- hedge to the banking sector, as we have already stressed. Besides, the greater flexibility in economic policy has allowed the economy to face the external shocks without a systemic crisis, although at the costs of the huge and quick increase in the public debt.28 Indeed, public debt as a percentage of GDP in Brazil increased from 34.1 percent in December 1997 to 57.4 percent in December 2002.29

In Argentina, due to the rigidity of the convertibility system, the survival of this system depended partly of the combination of foreign bank entry and a broader financial regulation framework. However, the effect of this combination was contradictory: although it resulted in an apparent increase in the financial system soundness, as the 1997-1999 external crises showed,30 it finally contributed to the rupture of the convertibility system due to the incentives for the dollarization of the economy. That is, the country depended on the desire and interest of foreign banks to get external funds and offer resources to the Central Bank of Argentina, through a contingent credit line (PCP). As the crisis unraveled, some of the supposed benefits of the international banks -such as the enhancement of the stability of the domestic banking system- did not quite materialize as expected.

As we have already stressed in section 3, prudential regulatory framework in Argentina stimulated the increase of dollarization, as it admitted the constitution of deposits and loans in foreign currency and it facilitated the access of financial institutions to the international financial markets. As a result, as financial regulations increased the degree of Argentina’s economy dollarization, they increased the exchange rate risk of the banks. Indeed, monetary authorities did not ask that banks constitute provisions for reserves or higher capitalization rates to face the exchange rate risk. Consequently, Argentine banks had no incentive to hedge their positions in foreign currencies (Fanelli, 2003, p. 35-36).

Summing up, the Argentinean case illustrates that it is very difficult to maintain a sound banking sector with only prudential policies when economic problems are due to serious macroeconomic unbalances. It also shows that the presence of international banks can not be enough to prevent local banking crises and sizable losses for depositors.

Conclusion

We can now summarize the main conclusions of this paper:

In both Argentina and Brazil the combination between financial liberalization and the framework of the macroeconomic policy (that allowed bigger or shorter flexibility in terms of country’s responses to external shocks), plus the degree of development of financial system inherited from high inflation periods, was essential to understand the degree of internationalization of financial system and the reaction of the domestic private banks in each country. Financial liberalization, that followed the Convertibility system, was more intensive in Argentina than in Brazil, and it was followed by the acceleration of dollarization of the Argentine economy. This is probably one of the reasons why currency-financial crisis was much more destructive -in economic-social terms- in Argentina than in Brazil.

There is no evidence that in the long run foreign bank entry has contributed, by itself, to strengthen significantly the financial system and to avoid balance of payments crises in Argentina and Brazil. Indeed, the greater stability due to the foreign bank presence would be derived by the fact that the branches and subsidiaries of large international banks can draw on their parent for addition funding and capital when needed. In Brazil banking soundness has been obtained by the government offer of exchange rate -and interest rate- hedges to the banking sector at the cost of the weakening of public finance conditions. In Argentina, it was expected that the presence of foreign banks in the domestic banking system would enhance the financial system as occurred after the 1995 banking crisis due to Mexican contagion. As the 2001-2002 crisis unraveled, some of the supposed benefits of the international banks -such as the enhancement of the stability of the domestic banking system- did not quite materialize as expected.

The experience of foreign bank entry in Argentina and Brazil has evidenced that the penetration of foreign banks in these countries did not contribute effectively to the improvement of the macroeconomic efficiency of the financial system.31 The reality of these countries shows that the unstable macroeconomic environment is one of the main factors responsible for the weak level of financial development -as measured by the ratio of total credit-to-GDP and total financial assets-to-GDP- in their domestic financial systems.

The expected results of the foreign bank entry -more diversified portfolio with predominance of credit operations, greater efficiency and enhancement of the soundness of the financial system- did not materialize in Argentina and Brazil. In both countries foreign banks behavior was similar to domestic private banks, in terms of portfolio allocation, credit policy, etc., although in Argentina there are some evidences that in tranquil times foreign bank entry contributed to the enhancement of the financial system. These results in Argentina should be expected as foreign entities in Argentina had a more solid situation than domestic ones, that had been very weakened due to effects of the Mexican crisis. Although the World Bank and some economists argued that one of the main benefits of the presence of foreign banks in Argentina (and Latin America) was the overall decline in systemic risk, during the Argentina’s 2001 crisis foreign banks behavior did not contribute to enhance financial stability of the banking sector. In the case of Brazil, domestic private banks reacted positively to foreign bank penetration, improving their efficiency, obtaining revenue economies through cross-selling activities and at the same time expanding their activities organically or by mergers and acquisitions, as they have some advantages over foreign banks which they can exploit, since they are more adapted to the peculiarities of the Brazilian banking market and accumulated capabilities to survive in an environment of macroeconomic instability. Furthermore, they were less affected by the 1994-1995 crisis than domestic banks in Argentina.

Changes in banking behavior and improvement in the soundness of the financial system in Argentina and Brazil -in order to reach the desirable macroeconomic efficiency of the financial system- depend crucially on improvements in the macroeconomic environment. Furthermore, as the recent Argentine experience suggests, EMEs must be very careful in adopting a quick and intensive financial liberalization in their economies in order to avoid disruptive process of financial speculation in their financial markets that results in deep real negative effects in the domestic economy.